Hi friends I would love to explain the concept of refinance and I would love even more for a simple numerical example, thanks…

I have a dream - USA Real Estate Forum version: I am happy to join you today, in what will be recorded in the words of the times as the greatest demonstrations for freedom in the history of our nation. A year and a half ago, a great American (former Israeli), in whose shadow we live today, signed the sparrow's speech. This word is a beacon of light of hope for millions of dwarfs, economic slaves who were burned by a healing ulcer of...

Happy New Year and Happy holidays to us all ???? Highly appreciate that we have a job, especially during such periods. ???????? Participates in some of the projects we are working on: First photo - Rental…

The BRRRR Method Imagine yourself attending a real estate investment networking event, and you hear someone say “BRRRRR”. Chances are your colleague is not responding to room temperature…

Today, at Nadlan Capital Group, we work with 96 lenders who compete to provide the best terms for your loan, constantly working on signing agreements with...

Very nice. So I'm very happy that it fell to me to be an entrepreneur this week in the forum. In the first post I will give some of my story, when later this week I will try to give from my angle…

Good week and Happy Freedom Day All parents asked me to update on the shaft of the elevator so please. Video of the beginning and end of the concrete casting of the shaft, the basement floor.

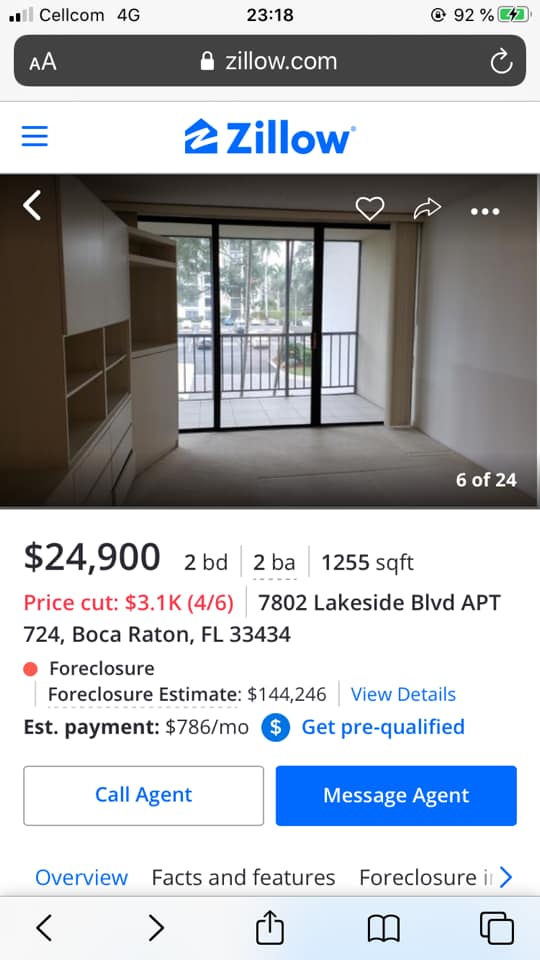

I would appreciate a brief explanation of what you see in the picture. Thanks in advance to the helpers Link to the original post on Facebook - works on a desktop computer (to view the post you must be a member approved for the forum)

What's going on an expensive group? So this week I'm getting into the big shoes of "Entrepreneurs of the Week," thanking Lior on stage. So in a few words about me and us, I am a co-owner of SafetyTint, having been operating for the past eight years in Orlando, Florida as a real estate agency for local and distant investors. This week I will start with a post slightly different from my regular content, the topic is dealing with pressures and changes…

Happy to tell about a project I have been working on in recent months: We bought for a dollar (not kidding) a 4-story building, which had 6 apartments above a commercial floor before…

there is Connect to the system To post a comment.

Please confirm you want to block this member.

You will no longer be able to:

Please note: This action will also remove this member from your connections and send a report to the site admin. Please allow a few minutes for this process to complete.

In the United States it is sometimes called cash-out.

After a period in which you hold a property that you bought in cash (for example) you can;

1. Mortgage the property

2. Get some or all of the cash you put in the house

3. Pay monthly mortgage payments to the bank

4. Make a higher return, and have more cash on hand to continue making trades.

For example:

You bought a property for $ 50,000

Renovated for $ 30,000

Total investment $ 80,000

And the introduction of a tenant,

Rent $ 1,000.

Now you come to the bank and tell him - I want to mortgage the property.

The bank makes appraisals and is willing to give you 70% of the value of the property.

According to the appraisals, the value of the property is $ 100,000 and therefore, you will receive *** cash *** of $ 70,000 from the bank and pay monthly payments on them, with the guarantee for the money being the property.

In this case, you are "invested" in the property for only $ 10,000, and along with the returns you are probably making a very nice return, in addition to the rent "buying" the house back. (Returns the fund)

In some cases, it is possible to "withdraw" the entire initial investment amount and sometimes even a higher amount than the initial investment.

In the context of a mortgage, in this country it is called a mortgage cycle

Thanks so much for the answers ??

Moshe Orange

Taking out a mortgage (financing an existing property) is not in favor of buying.

Copies here part of a post I wrote about calculating a return on a real estate transaction in the US, including a numerical example of refinance and its benefits:

For example, let's say we buy a new property in the United States for $ 200,000 (including transaction expenses), with the rent we are expected to receive at $ 1,800 per month.

We manage the property remotely so we will have to pay the management company. In addition there are other expenses that apply to us such as local tax (the American equivalent of property tax), insurance, small repairs and turnover of tenants - short periods in which the property is not rented and payment to the management company for finding a new tenant or extending the contract with the existing tenant. Since this is a new property, these expenses will be relatively small - about $ 7,200 per year (about a third of the rent, if it was an old property, we would take into account larger expenses - 45% -50% of the rent).

Our return will then be:

(1,800 × 12-7200) / 200,000 = 7.2% before tax.

I have previously published a detailed post on taxation in real estate investments abroad. The calculations below are based on the information in this post.

Due to the relatively low level of expenses, it was chosen to pay a reduced tax on the property. The annual tax will amount to $ 2440. Thus the net return will be:

(1,800×12-7200-2440)/200,000 = 5.98%

In practice, in this situation, tax will also be paid in the United States, so that in practice the fruitful yield (rent) will be about 5.5%.

Now suppose we purchase the property with a local mortgage. Suppose we take out a 30-year mortgage at 60% of the value of the property at an interest rate of 5.95% (high interest since we usually do not have a local credit history). The mortgage repayment will be $ 716 per month. Consider our return on equity in this case:

(1,800 × 12-716 × 12-7200) / 80,000 = 7.26% before tax.

We received a similar return on the equity in the case without the financing (compared to Israel, since here we usually receive a lower current return). However, there are several advantages to financing. First, the mortgage interest is a recognized expense and therefore in this case we will pay tax in the marginal tax track and if we assume that our marginal tax is 35%, the tax we will pay will be $688. Thus, the net yield from renting while repaying the mortgage will be:

(1800×12-716×12-7200-688)/80000 = 6.4%

I have not considered here the tax to be paid in the United States, since in the marginal tax route, this tax is deducted from the tax payment in the country.

"Wait, what about the increase in value?"

We strive to purchase properties in areas of demand, where housing prices are on the rise. Therefore we calculate our total return after 6 years on the assumption (quite solid) that the price of the property increases on average by 5% per year. The total increase amounts to 34%, which means that the value of the property after 6 years is $ 268,000.

Suppose we want to sell the property at this point in time. Selling expenses will be:

Brokerage fee - $ 17,420

Selling expenses - $ 5,000

Capital gains tax (in Israel) - $ 17,000

Total - $ 28,580

If we purchased without financing, our capital return will be:

(68,000 - 28580) / 200,000 = 19.71%. That is 3.04% per year.

Total return (capital + fruitful): 5.5% + 3.04% = 8.54%

If we purchased the property with financing, we will get back $ 118,985 after offsetting the expenses and the mortgage balance. Thus our capital return will stand at:

(118,985-80,000) / 80,000 = 48.73%. I.e. 6.84%.

Total return (capital + fruitful): 6.4% + 6.84% = 13.24%.

Now let's assume another case. Instead of selling the property, we will refinance taking into account the increase in value. We will ask the bank for a new loan of 60% of the new value of the property, ie $ 160,800. To offset our existing debt, this is a sum of $ 51,000, which we can spend without a tax event.

Our return as a result of the refinancing process will be:

51,000 / 80,000 = 63.75%, i.e. 8.57% per annum

And the total return (fruitful + refinancing) will be: 6.4% + 8.57% = 14.97% on average per year. In this case the property remains in our possession and continues to work and bring us a handsome return.

*** Due Diligence - I am accompanied by financial growth and financial independence. I do not market investments or assets but help my clients choose the right investments for their business plan.

In short: it is a process of exchanging the terms of an existing credit agreement, usually when it comes to a loan or mortgage. When a business or individual decides to refinance a credit obligation, they are in fact seeking to make favorable changes in the interest rate, payment schedule and / or other terms specified in their contract. If approved, the borrower will receive a new contract that takes the place of the original agreement on better terms.