The Federal Reserve is set to make a pivotal decision this week, with many experts predicting a cut to its benchmark interest rate. While the latest inflation figures remain higher than expected, the market is pricing in a 96% chance of a 25 basis-point rate reduction when the Fed meets on Wednesday. This move is anticipated to offer some relief to consumers dealing with high-interest costs, especially as the economy faces challenges like a weak labor market. Here’s how you can position yourself to take advantage of the Fed’s decision.

1. Pay Down High-Interest Debt

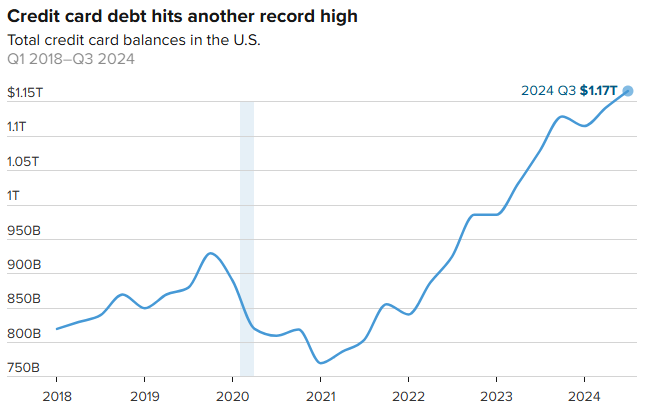

A rate cut by the Fed will likely bring some relief to borrowers, particularly those with high-interest, variable-rate debts such as credit cards. However, the reduction might not be drastic enough to immediately ease the burden on credit card balances. If the Fed cuts rates by a quarter-point, borrowers might see their credit card APRs fall slightly, but it’s unlikely to lead to dramatic savings right away.

Experts recommend that, instead of waiting for a minor rate reduction, consumers should take proactive steps now to reduce high-interest debts. One effective strategy is transferring balances to a zero-interest balance transfer credit card or consolidating debt with a personal loan. Lowering debt now can not only help improve your financial situation but also position you for better loan terms down the line.

“For those carrying significant debt, especially credit card debt or high-interest car loans, focusing on paying that off should be a priority,” says Stephen Kates, certified financial planner and analyst at Bankrate.

2. Make the Most of Your Savings

On the flip side, savers can still benefit from the Fed’s actions. While interest rates on savings accounts, money markets, and CDs are expected to drop, high-yield savings accounts and CDs offering rates above 4% remain an attractive option for those looking to maximize returns. These accounts currently offer rates that are 10 times the national average.

By locking in a CD or moving funds into a high-yield savings account, you could secure returns for the coming months, even if the Fed cuts rates. For instance, a typical saver with about $8,000 in a checking or savings account could earn an additional $320 annually by moving that money into an account offering a 4% interest rate, according to a recent survey by Santander Bank.

3. Consider Buying or Refinancing Your Home

The housing market, which has already seen some improvement due to lower mortgage rates, could see further momentum from a rate cut. Historically, lower interest rates have been beneficial to homebuyers by unlocking more affordable mortgage payments, especially for those who have been waiting to buy in a high-rate environment.

“Lower rates could unlock the frozen housing market, helping buyers who were hesitant to sell their homes due to their current low mortgage rates,” says Bob Schwartz, senior economist at Oxford Economics.

Mortgage rates have already dropped from over 7% earlier this year to around 6.3% for a 30-year fixed mortgage. If the Fed continues its rate-cutting path, it could lower rates even further, which may encourage more people to enter the market, leading to a more competitive environment and more inventory.

4. Work on Improving Your Credit Score

Finally, one of the best ways to secure better terms on any loan whether it’s for a mortgage, car, or credit card—is by boosting your credit score. The higher your score, the lower the interest rate you’ll pay, regardless of Fed policy changes. To improve your credit score, focus on paying your bills on time, keeping your credit card balances low, and avoiding unnecessary credit applications.

A simple strategy to improve your score is to ensure that you keep your revolving debt below 30% of your available credit. Even one late payment can significantly affect your score, so be sure to check your credit report regularly for any errors and address them promptly. A higher credit score can make a big difference in securing favorable terms and reducing overall debt costs.

Conclusion

While the Fed’s expected rate cut may seem like a small step, it can have a meaningful impact on your financial strategy, from paying down high-interest debt to making smarter savings and investment decisions. By preparing ahead of time, you can take full advantage of the opportunities presented by lower rates and strengthen your financial position for the future. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.