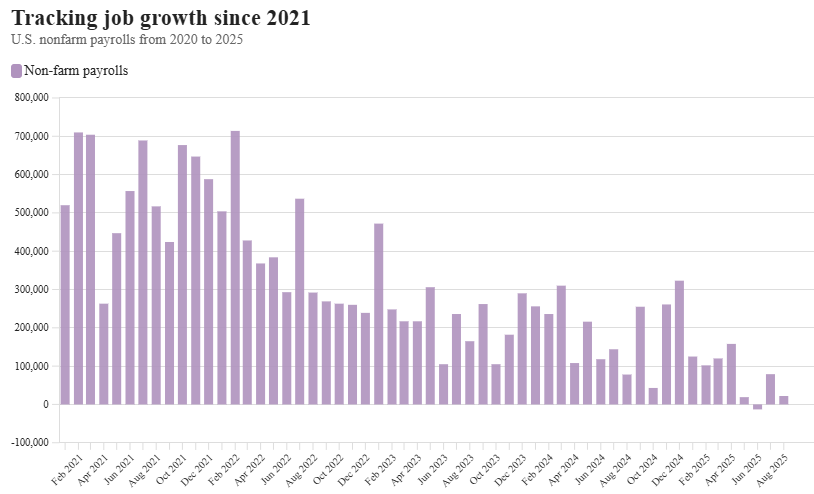

The U.S. labor market showed unexpected signs of weakness in August, with job growth falling far below expectations, further fueling concerns over the nation’s economic outlook. According to the latest data from the U.S. Labor Department, nonfarm payrolls increased by just 22,000 jobs in August, well under the 75,000 predicted by economists surveyed by LSEG. This miss has raised alarms about a potential slowdown in economic activity, especially after a string of weaker-than-expected reports over the past few months.

The unemployment rate also saw a slight uptick, rising to 4.3% from 4.2% in July, in line with analysts’ forecasts. This marks the first rise in the unemployment rate in several months, indicating that the job market may be cooling off after a period of steady gains.

Revised Data Shows Continued Softness

In addition to the August data, the Labor Department also revised the job numbers for June and July, showing that job growth in the prior two months was weaker than initially reported. Specifically, June’s job creation was revised down from 14,000 to a loss of 13,000, and July’s increase was adjusted upward by 6,000, from 73,000 to 79,000. Altogether, employment in June and July combined was 21,000 jobs lower than previously reported.

These downward revisions suggest that the labor market’s recovery is not as strong as previously thought, adding to the growing concerns about the U.S. economy’s resilience.

Sector Performance and Regional Trends

The jobs report revealed uneven trends across sectors. Private payrolls added 38,000 jobs in August, significantly underperforming the 75,000 forecasted by economists. On the other hand, the government sector lost 16,000 jobs, driven by a 15,000 decline in federal government positions and a 13,000 reduction in state government employment.

While some industries struggled, the healthcare sector showed continued strength, adding 30,600 jobs, although this was slightly below its average monthly gain of 42,000 over the past year. Social assistance also saw an increase, with 16,200 jobs added. Conversely, manufacturing experienced a significant setback, losing 12,000 jobs, more than double the 5,000 decline that had been expected.

The Fed’s Response and Economic Outlook

The August jobs data arrives at a pivotal time, as the Federal Reserve is closely monitoring the labor market in its ongoing effort to curb inflation without stalling economic growth. The disappointing job gains, combined with concerns over inflation and ongoing tariff impacts, have led to growing expectations that the Fed will consider rate cuts in its upcoming September meeting.

Fed Chair Jerome Powell has signaled that the central bank may lean towards easing rates, particularly in light of weaker labor data. However, inflation remains a significant concern, with prices continuing to rise above the Fed’s 2% target. The most recent consumer price index (CPI) report showed 2.7% inflation for July, while the personal consumption expenditures (PCE) inflation gauge came in at 2.6% for the same period.

Despite these inflation concerns, LPL Chief Economist Jeffrey Roach predicts that the Fed will likely opt for a 25 basis-point rate cut in September, as labor market weakness may outweigh inflationary pressures. “The labor market is at a standstill, and businesses are slowing the pace of hiring due to uncertainty over tariffs and Fed policy,” Roach explained.

Recession Risks and Economic Sentiment

This data is adding to growing fears of a recession, with some analysts warning that the U.S. economy could soon enter a period of stagflation a mix of stagnant growth and persistent inflation. Seema Shah, Chief Global Strategist at Principal Asset Management, described the August jobs report as a balancing act for the markets. “It strikes a balance between the likelihood of Fed rate cuts and concerns about a slowing economy,” she said. “If the labor market continues to deteriorate, it may signal that bad news is becoming just bad news, which would be a major concern for the economy.”

The continued slowdown in job creation, combined with rising unemployment and the persistence of inflation, has created a delicate situation. Many would-be buyers and businesses are holding off on major decisions, waiting for clearer signals from both the Fed and broader economic indicators.

Impact on Homebuyers and Builders

For homebuyers, the rising mortgage rates and elevated home prices have already made the housing market challenging. As interest rates continue to hover in the high 6% range, many are reluctant to commit to buying a home. However, some analysts are hopeful that a rate cut from the Fed will help lower borrowing costs and re-energize the housing market.

In the meantime, homebuilders remain cautious. Although they have benefitted from some easing in mortgage rates in recent weeks, rising material costs, labor shortages, and regulatory hurdles continue to dampen demand and slow construction in certain regions.

Looking Ahead

As we head into the fall, economic uncertainty looms large. The Federal Reserve faces difficult decisions ahead as it balances the job market slowdown with the ongoing fight against inflation. For job seekers, homebuyers, and investors, the next few months could prove pivotal in determining the direction of the U.S. economy and whether the country can avoid a full-blown recession. The final CPI report for August and Federal Reserve announcements in the coming weeks will likely play a major role in shaping the market’s future expectations.

What does this mean for you? Stay tuned for our in-depth analysis of the job market and Federal Reserve policy, as well as tips for navigating potential economic challenges in the coming months. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.