Mortgage activity slowed modestly last week, extending a two-week decline but maintaining a much higher pace than last year. According to the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending October 10, overall application volume slipped 1.8% on a seasonally adjusted basis and 2% unadjusted. The pullback followed a notable September surge that had lifted demand to some of the strongest levels seen in 2025.

While the drop reflects a brief pause in momentum, analysts say it’s not an indication of fading housing demand. The market remains considerably more active than it was this time last year, as a small dip in mortgage rates and slightly improved inventory continue to draw buyers back in.

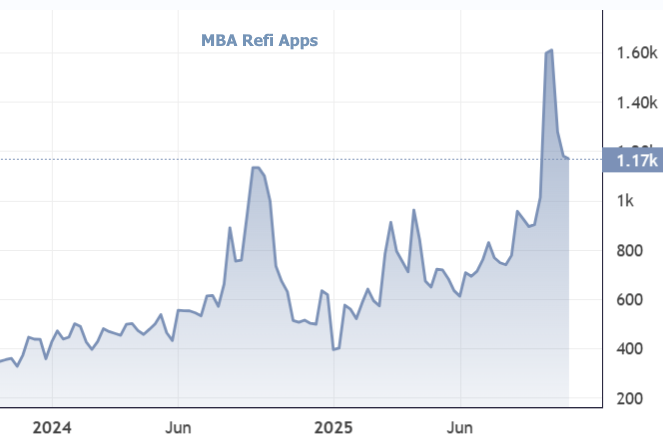

Refinancing Cools, But Still Outpaces 2024

The Refinance Index fell 1% from the previous week, yet remains 59% higher than the same week in 2024. After the sharp increase seen in September driven largely by lower rates and renewed optimism around potential future Fed cuts refi activity has plateaued but continues to hold at elevated levels.

Many homeowners with FHA loans are finding new opportunities to save, as FHA rates remain roughly 10 basis points lower than comparable conventional loans. This spread has prompted a noticeable uptick in FHA refinances, even as overall refi momentum steadies.

“Mortgage rate movements were mixed last week, with the 30-year fixed rate decreasing slightly to 6.42 percent,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Mortgage applications were lower overall, as conventional and VA activity pulled back. However, FHA applications particularly refinances posted a strong week, increasing 12 percent as borrowers sought to capitalize on more favorable rate spreads.”

Purchase Activity Slows, But Still Ahead of 2024 Levels

Purchase applications declined 3% on a seasonally adjusted basis and 2% unadjusted compared to the prior week. Even with the decline, activity is still 20% higher than the same time last year, highlighting a continued recovery from 2024’s depressed buying conditions.

Kan noted that the pullback was relatively minor considering the strong gains made earlier in the fall:

“Purchase activity is moderating, but we’re still seeing healthy levels of demand compared to a year ago. Improved inventory in certain markets and slight relief in mortgage rates are helping to sustain homebuyer interest, even as affordability remains tight.”

That resilience is especially notable given broader economic uncertainty. Many would-be buyers remain cautious due to high home prices and budget pressures, but the combination of steadier rates and more listings has made conditions slightly more favorable.

Market Composition and Loan Share Shifts

The refinance share of total mortgage activity rose to 53.6%, while the adjustable-rate mortgage (ARM) share declined to 9.3%, indicating that most borrowers are favoring stability over flexibility amid uncertain rate trends.

Among government-backed loan programs:

- FHA share increased to 20.5% (from 19.8%)

- VA share slipped to 14.9% (from 15.3%)

- USDA share held steady near 0.5%

This shift toward FHA lending aligns with recent trends showing more activity among moderate-income borrowers and first-time buyers taking advantage of lower down payment requirements.

Mortgage Rate Snapshot

| Loan Type | Average Rate | Previous Week | Points |

|---|---|---|---|

| 30-Year Fixed | 6.42% | 6.43% | 0.61 (from 0.60) |

| 15-Year Fixed | 5.77% | Unchanged | 0.70 (from 0.79) |

| 30-Year Jumbo | 6.47% | 6.60% | 0.53 (from 0.44) |

| FHA 30-Year | 6.19% | Unchanged | 0.76 (from 0.73) |

| 5/1 ARM | 5.63% | 5.49% | 0.59 (from 0.74) |

Rates have remained remarkably steady through October, hovering near their lowest levels since mid-September. This stability has prevented a sharper decline in refinance activity and helped preserve some purchase demand heading into the slower fall season.

However, analysts warn that volatility could return. Recent movements in Treasury yields and pending economic data especially on inflation and employment could influence mortgage pricing in the coming weeks.

Outlook: Holding Steady Amid Crosscurrents

Even with a mild dip in applications, the housing market appears to be holding firm after a turbulent year of rate swings and affordability challenges. Industry experts say the key factors to watch heading into November will be Treasury yield trends, Fed policy guidance, and inventory growth.

If rates remain stable or drift slightly lower, refinancing could pick up again, especially among FHA borrowers and homeowners who missed earlier opportunities. On the purchase side, gradual inventory recovery and a potential moderation in home prices could sustain demand even as seasonal slowdowns begin.

For now, mortgage activity remains resilient proof that, despite financial headwinds, many Americans are still eager to enter or stay in the housing market while opportunities last. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.