For years, renters have heard the same advice: buying a home is cheaper in the long run. New data suggests that statement is still largely true but with an increasingly important caveat.

According to the newly released 2026 Rental Affordability Report from ATTOM, owning a home is more affordable than renting a three-bedroom property in a majority of U.S. counties. However, while the monthly math may favor buyers, rising home prices and steep upfront costs are making it harder for many households to actually make the leap.

So where does homeownership truly win and where does affordability remain out of reach?

What the ATTOM Report Found

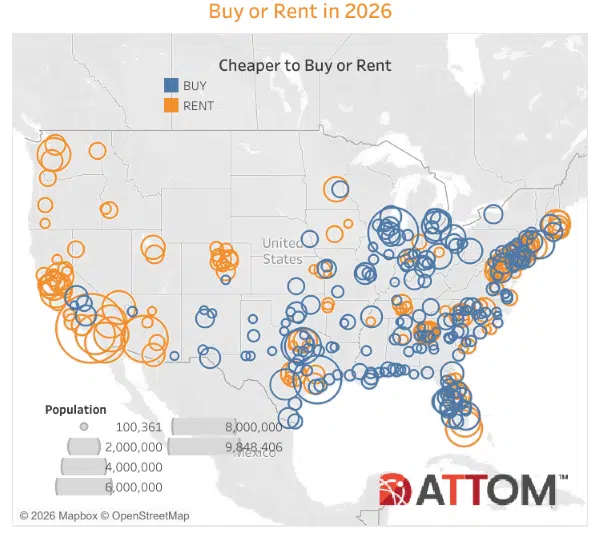

ATTOM analyzed 364 U.S. counties with sufficient population and housing data to compare the cost of owning versus renting.

Here are the most important findings:

- In 57.7% of counties (210 out of 364), owning a home required a smaller share of wages than renting a three-bedroom home

- In 69% of counties, median home prices rose faster than rents in 2025

- Homeownership costs exceeded one-third of wages in 65.7% of counties

- Renting a three-bedroom home consumed over one-third of wages in 76.9% of counties

- Midwest counties showed the strongest affordability advantage for buyers

The takeaway? Buying often wins on monthly affordability but only if buyers can clear the upfront hurdle.

Why Buying Still Looks Better Over the Long Term

On a purely monthly basis, homeownership often provides better value than renting, especially in markets where rents have risen aggressively over the past few years.

Mortgage payments, while higher than in the pre-pandemic era, can still be more predictable than rent increases particularly for buyers with fixed-rate loans. Over time, owners also benefit from equity accumulation, something renters never capture.

That long-term advantage is exactly what many households are weighing right now.

As Rob Barber, CEO of ATTOM, explains:

“Buying is typically the most affordable long-term option, but as the housing market sets new record-high prices quarter after quarter, affording the initial investment becomes increasingly challenging.”

Does long-term savings matter if you can’t get past the down payment?

The Down Payment Problem: Where the Math Breaks Down

While ownership may cost less over time, getting into a home has become significantly harder.

By the end of 2025, U.S. home prices reached new record highs. In more than two-thirds of the counties ATTOM studied, home prices grew faster than rents last year. That trend increases the size of required down payments often tens of thousands of dollars more than just a few years ago.

This creates a paradox:

- Monthly ownership costs may be lower than rent

- But the upfront cash needed to buy keeps rising

For first-time buyers, young families, and relocating professionals, this gap is often the deciding factor.

Where Home Prices Are Rising Faster Than Rents

In many of the nation’s largest counties, home prices continue to outpace rent growth, further complicating affordability.

Among the most populous counties where home prices rose faster than rents:

- Los Angeles County

- Harris County

- Maricopa County

- San Diego County

- Orange County

In these markets, even modest price appreciation can dramatically increase the barrier to entry for buyers.

Where Rent Is Rising Faster Than Home Prices

The opposite trend rent rising faster than home prices appeared in fewer but still notable markets.

Counties where rent increases outpaced home prices include:

- Cook County

- Alameda County

- Palm Beach County

- Hillsborough County

- Orange County

In these areas, renters may feel growing pressure to buy but still face the same upfront affordability constraints.

A Strong Regional Divide Emerges

One of the clearest patterns in ATTOM’s report is the sharp regional split between where buying makes sense and where it doesn’t.

Homeownership was more affordable than renting in:

- 81.5% of Midwest counties

- 66.3% of Southern counties

- 48.8% of Northeastern counties

- Just 16.9% of Western counties

The Midwest stands out as the clear affordability leader, while the West remains the most challenging region for buyers.

Why the difference? Lower home prices, slower appreciation, and steadier wage-to-cost ratios play a major role.

Where Owning Is Most Affordable

Some counties stand out nationally for how little income is required to own a home assuming a 20% down payment.

The most affordable counties for homeownership include:

- Peoria County – 14.5% of wages

- Wayne County – 14.9%

- Mobile County – 15.1%

- Jefferson County – 16.3%

- Montgomery County – 16.7%

In these markets, ownership remains not just attainable but clearly advantageous compared to renting.

Where Both Renting and Owning Are Expensive

Affordability challenges aren’t limited to buyers.

In nearly 77% of all counties analyzed, renting a three-bedroom home consumed more than one-third of the typical resident’s wages.

By region:

- West: 95.4% of counties

- Northeast: 90.7%

- South: 77.7%

- Midwest: 40.7%

This means many households are stretched regardless of tenure choice buying or renting.

Is affordability becoming less about which option you choose and more about where you live?

What This Means for Renters Considering Buying

For renters, the data sends mixed signals.

On one hand, buying often offers better long-term affordability and stability. On the other, saving for a down payment has become the biggest obstacle especially in high-growth or coastal markets.

Renters who can access:

- Down payment assistance

- Family support

- Employer relocation benefits

may be better positioned to take advantage of ownership’s long-term edge.

What This Means for Buyers and Investors

For buyers, especially in the Midwest and parts of the South, the math still strongly favors ownership—if financing and cash reserves allow.

For investors, the data reinforces why rental demand remains strong in high-cost regions, even as ownership looks cheaper on paper. When entry costs rise faster than wages, renting becomes a necessity rather than a choice.

That dynamic supports long-term rental demand but also highlights growing affordability stress.

The Bigger Picture: Affordability Isn’t One-Size-Fits-All

ATTOM’s findings make one thing clear: national housing headlines often miss the local reality.

In some counties, owning is a clear financial win. In others, both renting and buying stretch household budgets to the limit. And across the country, rising prices are making the transition from renting to owning harder even when ownership would eventually cost less.

Conclusion: Long-Term Value vs. Short-Term Barriers

Homeownership still beats renting in most U.S. counties when measured over time. But rising home prices and upfront costs are complicating that equation for millions of households.

At Nadlan Capital Group, we believe smart housing decisions start with understanding local data not national averages. The “right” choice depends on wages, prices, timing, and long-term goals.

Do you think rising home prices will eventually push more renters into buying or keep them renting longer? Share your thoughts with us and stay connected with Nadlan Capital Group for practical, data-driven insights into today’s housing market.