Nonbank mortgage lending now accounts for the majority of home loans in the United States, according to a recent review by the U.S. Government Accountability Office (GAO). The agency examined why nonbank lenders have gained ground, what risks they may pose, and how federal regulators monitor their financial health.

The findings show a major shift in the structure of the mortgage market over the past decade.

What Is a Nonbank Mortgage Lender?

Unlike traditional banks, nonbank mortgage companies do not accept deposits. Banks use customer deposits as a stable funding source for loans. Nonbanks, by contrast, rely heavily on short-term borrowing and credit lines to fund mortgage originations and servicing operations.

That funding model can work well in stable markets. But it may create vulnerabilities during recessions or financial stress, when short-term credit can tighten quickly.

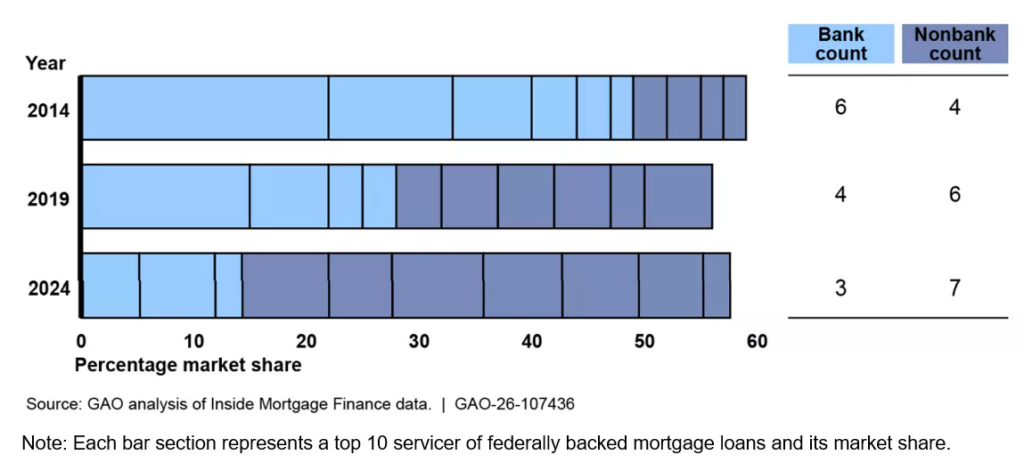

Market Share Has Shifted Dramatically

After the 2008 financial crisis, banks reduced their presence in mortgage lending. Stricter capital requirements made it more costly for banks to hold mortgages on their balance sheets.

At the same time, government support for mortgage-backed securities expanded. Loans guaranteed by federal entities continued to flow, and nonbank lenders stepped in to meet demand.

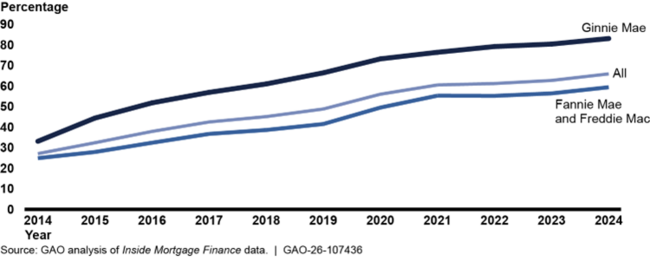

Between 2014 and 2024, nonbanks moved from a minority role to a dominant one in servicing federally backed mortgages. The share of these loans serviced by nonbanks rose from 27% to 66% over that period.

Today, most loans bundled into securities backed by federal guarantees are originated and serviced by nonbank firms.

Major institutions involved in this system include:

- Ginnie Mae, which guarantees nearly $3 trillion in mortgage-backed securities

- Federal Housing Finance Agency, which oversees

- Fannie Mae and

- Freddie Mac

These entities help maintain liquidity in the housing market by backing trillions of dollars in mortgage securities.

Why Nonbanks Grew So Quickly

Nonbank mortgage lending expanded for several reasons.

First, banks pulled back after regulatory changes increased capital requirements.

Second, nonbanks adopted digital tools quickly. Many offer fully online mortgage applications, faster processing, and automated underwriting systems.

Third, nonbank lenders often serve borrowers with lower incomes or limited credit access. They play a key role in federally insured loan programs.

Companies such as Rocket Mortgage and others built large national platforms based on technology and scale.

For many borrowers, nonbanks offer convenience and competitive pricing.

What Are the Risks?

The GAO report highlights one main concern: funding risk.

Because nonbanks rely on short-term borrowing, they are sensitive to disruptions in credit markets. If lenders providing warehouse lines of credit pull back, nonbanks could struggle to:

- Originate new mortgages

- Advance payments to investors

- Manage servicing obligations

If a large nonbank were to fail, it could disrupt mortgage servicing and securities markets. Since many of these loans carry federal guarantees, taxpayers could ultimately bear losses.

This risk is tied to the structure of the funding system rather than the credit quality of borrowers alone.

Oversight Gaps Identified

Unlike banks, nonbank mortgage lenders do not have a single federal safety and soundness regulator.

Instead, oversight is fragmented.

The Federal Housing Finance Agency (FHFA) and Ginnie Mae monitor nonbanks that participate in federally backed programs. However, the GAO identified several weaknesses in current oversight:

1. Financial Data Accuracy

Both agencies rely on financial information self-reported by nonbanks. The GAO found that FHFA does not fully verify the accuracy of this data, which may limit the reliability of risk assessments.

2. Watch Lists

FHFA and Ginnie Mae maintain watch lists of firms considered higher risk. However, the review found that neither agency fully evaluates the risks associated with short-term funding exposure when creating these lists.

3. Stress Testing

Both agencies conduct scenario analyses to assess how economic downturns could affect nonbanks. However, Ginnie Mae currently models only one stress scenario, limiting its ability to evaluate a broader range of potential shocks.

The GAO noted that broader stress testing could improve preparation for market disruptions.

Why This Matters for Homebuyers

For most borrowers, nonbank mortgage lending has expanded access and speed.

But systemic risk matters.

If funding pressure leads to instability among large mortgage servicers, disruptions could affect loan processing, servicing transfers, and market confidence.

While federal guarantees provide a backstop for mortgage securities, they may also increase taxpayer exposure if large nonbank firms fail during downturns.

The issue is not whether nonbanks should operate they now form a central part of the housing finance system. The key question is whether oversight keeps pace with their growing role.

The Bigger Picture

The mortgage market has evolved significantly since the financial crisis. Nonbanks now dominate many federally backed loan channels, supported by government guarantees and investor demand for mortgage-backed securities.

The GAO’s review does not call for eliminating nonbank participation. Instead, it emphasizes stronger monitoring, improved data validation, and broader stress analysis to manage risks tied to short-term funding models.

As housing demand continues and mortgage markets remain central to the U.S. economy, regulators face the challenge of balancing access, innovation, and financial stability.

Nonbank mortgage lending is now a core feature of the system and managing its risks will remain an important policy issue in 2026 and beyond. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.