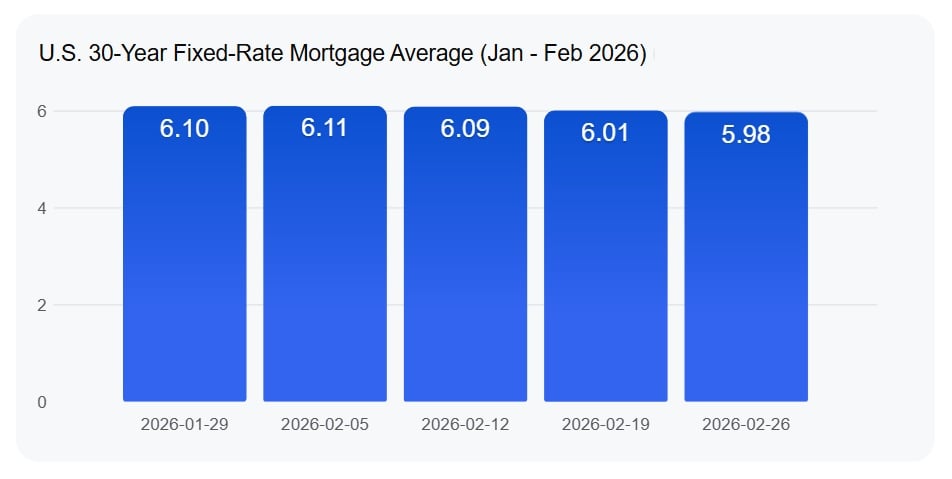

The 30-year fixed mortgage rate March 2026 has reached an important milestone. According to the latest report from Freddie Mac, the average 30-year fixed-rate mortgage now stands at 5.98%.

This marks the first time in more than three years that the rate has moved back into the 5% range. While the weekly decline was small, the year-over-year change tells a much bigger story. Compared to the same time last year, rates are down 78 basis points a significant shift in borrowing costs.

Understanding the 78 Basis Point Drop

A basis point equals one-hundredth of a percentage point. So a 78 basis point drop means mortgage rates have fallen by 0.78%.

Last year around this time, the 30-year fixed mortgage rate was closer to 6.76%. Moving from 6.76% to 5.98% may not sound dramatic at first glance, but over the life of a mortgage, it makes a real difference.

For example, on a $400,000 loan:

- At 6.76%, the monthly principal and interest payment would be roughly $2,597.

- At 5.98%, the payment would drop to about $2,462.

That’s a savings of roughly $135 per month, or more than $1,600 per year. Over 30 years, the total interest savings can reach tens of thousands of dollars.

The 15-year fixed mortgage rate is also lower than a year ago. It currently sits at 5.44%, about 50 basis points below last year’s average, even though it ticked slightly higher this week.

Why Dropping Below 6% Matters

The move under 6% carries more weight than just the math.

1. Psychological Impact

For many buyers, the difference between a rate starting with “6” and one starting with “5” feels meaningful. Buyers who were hesitant when rates were near 7% may feel more comfortable moving forward now.

Round numbers often act as mental barriers in financial decisions. Seeing a “5-handle” can motivate action.

2. Improved Affordability

Lower mortgage rates increase purchasing power. With the 30-year fixed mortgage rate March 2026 now below 6%, households can afford slightly higher home prices while keeping the same monthly payment.

This could help first-time buyers who were previously stretched by higher rates.

3. Potential Boost to Inventory

Many current homeowners locked in ultra-low rates near 3% during 2020 and 2021. They have been reluctant to sell because moving meant taking on a much higher rate.

While today’s rates are still above pandemic lows, the gap is shrinking. As rates decline, some owners may feel more comfortable listing their homes, which could improve supply.

Impact on the Spring Housing Market

This rate decline comes as the spring homebuying season begins — traditionally the busiest time of year for real estate.

Lower rates combined with seasonal activity could:

- Increase buyer traffic

- Boost refinance applications

- Encourage more listings

Early data already shows rising interest in refinancing among borrowers who took out loans at rates above 7% in recent years.

What’s Driving the Rate Movement?

Mortgage rates are influenced by several factors, including:

- U.S. Treasury yields

- Inflation expectations

- Federal Reserve policy

- Investor demand for mortgage-backed securities

Recent moderation in inflation data and expectations for steady Federal Reserve policy have helped ease pressure on bond markets. When bond yields fall, mortgage rates often follow.

While the Federal Reserve does not directly set mortgage rates, its policy stance influences broader financial conditions.

Should Buyers and Homeowners Act Now?

For buyers, the 30-year fixed mortgage rate March 2026 presents an opportunity that hasn’t been available in several years.

For homeowners with higher rates, refinancing could lower monthly payments or reduce total interest paid over time. However, refinancing decisions should consider closing costs, break-even timelines, and long-term plans.

It is also important to remember that rates can change quickly. Economic reports, especially inflation and employment data, can influence bond markets and mortgage pricing.

The Bigger Picture

The move to 5.98% does not signal a return to the historic lows of 2020 and 2021. But it does mark progress after a period when rates climbed above 7%.

A 78 basis point year-over-year decline is meaningful. It improves affordability, strengthens purchasing power, and may help restore activity in a market that slowed under higher borrowing costs.

For now, the sub-6% rate represents a turning point for many buyers and homeowners. Whether this trend continues will depend on upcoming economic data and broader market conditions, but the shift is already reshaping housing conversations in early 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.