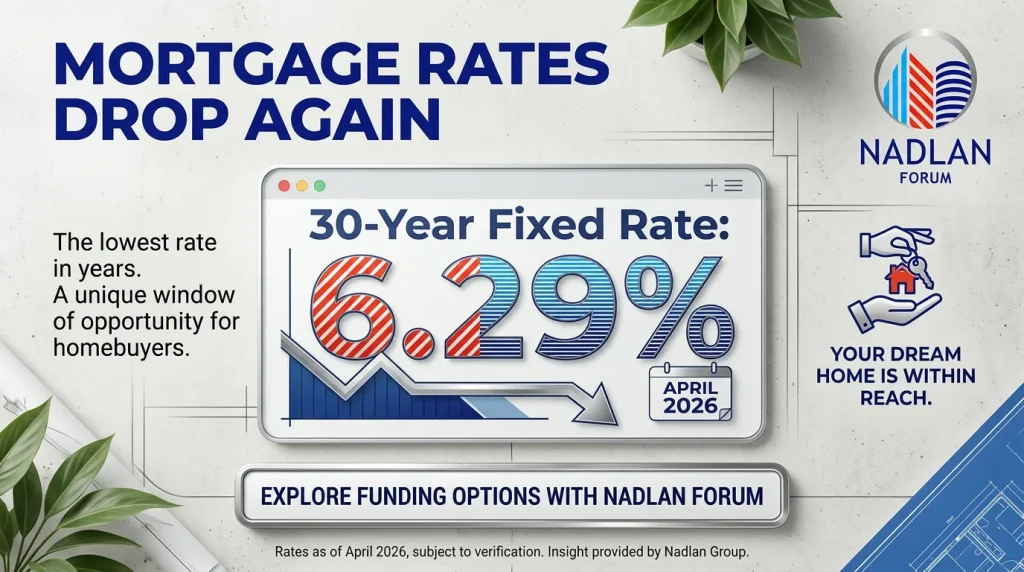

Mortgage rates moved lower for the second straight day, offering some relief after recent increases. The average 30-year fixed mortgage rate is now 6.29%, while the 15-year fixed rate has dropped to 5.73%. This shift comes as investors return to bonds, pushing yields down and helping ease borrowing costs.

Although the decline is modest, it signals how quickly mortgage rates can react to changes in financial markets, especially movements in bond yields.

Current Mortgage Rates Snapshot

Here are the latest national average mortgage rates:

- 30-year fixed: 6.29%

- 20-year fixed: 6.29%

- 15-year fixed: 5.73%

- 5/1 ARM: 6.13%

- 7/1 ARM: 6.31%

- 30-year VA: 5.96%

- 15-year VA: 5.53%

- 5/1 VA: 5.48%

These averages may vary depending on credit score, location, and lender, but they provide a general view of current market conditions.

Refinance Rates Also Move Lower

Refinance rates followed a similar trend, though they remain slightly higher than purchase rates:

- 30-year fixed refinance: 6.36%

- 20-year fixed refinance: 6.18%

- 15-year fixed refinance: 5.80%

- 5/1 ARM refinance: 6.11%

- 7/1 ARM refinance: 6.60%

- 30-year VA refinance: 5.73%

- 15-year VA refinance: 5.44%

- 5/1 VA refinance: 5.35%

Even with this decline, refinancing may still be less attractive for homeowners who locked in lower rates in previous years.

Why Mortgage Rates Are Falling Now

The recent drop in mortgage rates is tied closely to bond market activity. As investors shift money into safer assets like bonds, yields fall. Mortgage rates tend to follow those yields, which is why borrowing costs are easing.

This movement is happening amid ongoing uncertainty in global markets, including geopolitical tensions and economic concerns. When investors seek stability, mortgage rates often benefit.

30-Year vs. 15-Year Mortgage: Key Differences

Choosing between a 30-year and 15-year mortgage remains one of the most important decisions for buyers.

A 30-year mortgage offers lower monthly payments, making it easier for many households to afford a home. However, borrowers pay more interest over time due to the longer loan term.

A 15-year mortgage, on the other hand, comes with lower interest rates and allows homeowners to pay off their loan faster. The trade-off is higher monthly payments, which may not fit every budget.

For buyers who can manage the higher payments, a shorter loan term can lead to significant long-term savings.

Adjustable-Rate Mortgages: Still Worth Considering?

Adjustable-rate mortgages (ARMs) remain an option, though their advantage is less clear right now.

Loans like a 5/1 ARM or 7/1 ARM offer a fixed rate for an initial period before adjusting annually. These loans typically start with lower rates, but current data shows that ARM rates are sometimes close to or even higher than fixed rates.

This means borrowers should carefully compare options before choosing an ARM, especially if they plan to stay in the home long-term.

How Buyers Can Take Advantage of Current Rates

Even small changes in mortgage rates can impact affordability. Buyers looking to take advantage of current conditions can:

- Improve credit score before applying

- Reduce existing debt

- Save for a larger down payment

- Compare multiple lenders for the best offer

Some buyers may also explore rate buydown options, which can lower initial payments, though they come with upfront costs.

Are Mortgage Rates Going Down Long Term?

Despite the recent dip, mortgage rates remain higher than earlier in the year. Market volatility continues to influence rate movements, making it difficult to predict long-term trends.

Current forecasts suggest that mortgage rates may stay around the 6% range through the rest of 2026, with only gradual changes expected.

The Bottom Line

Mortgage rates have declined slightly for the second day in a row, bringing the 30-year fixed rate down to 6.29%. While this offers some short-term relief, the broader trend still reflects a market adjusting to higher borrowing costs.

For buyers and homeowners, the key is to stay flexible, monitor market changes, and act when rates align with their financial goals. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.