Mortgage applications for newly built homes declined in April as elevated borrowing costs and economic uncertainty continued weighing on housing demand across the United States.

According to the latest Builder Application Survey from the Mortgage Bankers Association, applications for new home purchases fell 2.4% compared to the same period last year.

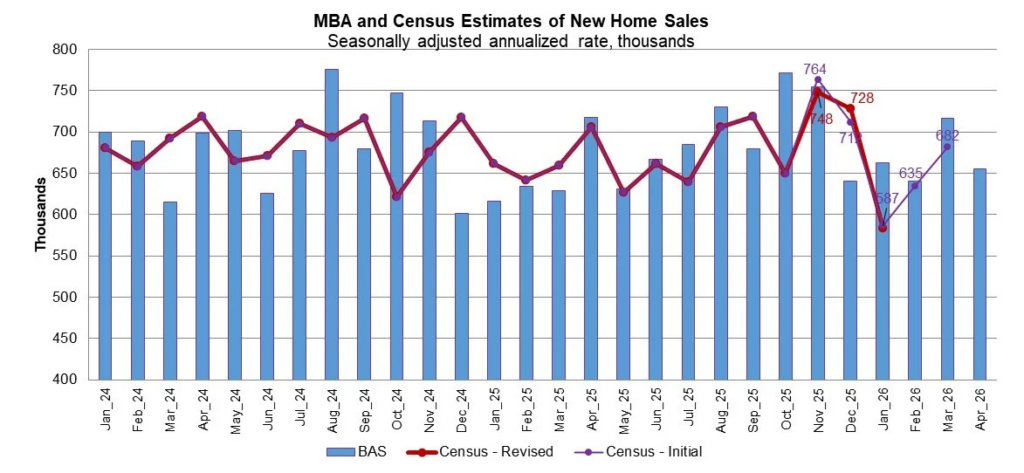

Applications also dropped 10% from March 2026, signaling slower activity during what is traditionally one of the busiest parts of the spring housing season.

Higher Mortgage Rates Continue Impacting Buyers

The decline in mortgage activity comes as mortgage rates remain near their highest levels since late 2025.

Higher financing costs have made affordability more difficult for many buyers, especially first-time homeowners already struggling with elevated home prices, insurance costs, and inflation.

Housing analysts say rising monthly payments continue reducing buyer confidence across both existing and newly built home markets.

According to MBA Deputy Chief Economist Joel Kan, both economic uncertainty and higher mortgage rates played major roles in slowing purchase activity in April.

Applications for newly constructed homes fell below year-ago levels for the first time since October 2025.

New Home Sales Pace Slows in April

MBA estimates show new single-family home sales operated at a seasonally adjusted annual rate of 655,000 units in April.

That represents:

- An 8.6% decline from March

- A slowdown from the previous estimate of 717,000 units

- Lower activity compared to earlier expectations for the spring market

The unadjusted estimate also showed weakness.

MBA estimated roughly 60,000 new home sales in April, down from 69,000 sales in March.

The slower pace reflects the broader cooling trend that has affected much of the housing market during recent months.

Builders Face Softer Spring Demand

The spring housing season typically produces stronger buyer demand, but elevated mortgage rates have weakened momentum in 2026.

Many buyers continue delaying purchases while waiting for:

- Lower mortgage rates

- Improved affordability

- Greater economic stability

- Lower monthly payments

Builders are also dealing with growing levels of unsold inventory in many markets.

As a result, many developers have started offering incentives to attract buyers, including:

- Mortgage rate buydowns

- Closing cost assistance

- Price reductions

- Upgrade packages

- Flexible financing terms

Industry analysts believe these incentives may help support demand later this year if mortgage rates stabilize.

Government Loan Programs Play Bigger Role

One of the more notable trends in April was the growing reliance on government-backed mortgage programs.

According to the report, FHA, VA, and USDA loans accounted for slightly more than half of all applications for newly built homes.

Loan application shares included:

- Conventional loans: 49.5%

- FHA loans: 35.7%

- VA loans: 13.7%

- USDA loans: 1.1%

Government-backed programs have become increasingly important because they often allow:

- Lower down payments

- More flexible credit requirements

- Lower upfront cash needs

- Additional affordability support

These programs continue helping buyers who may struggle qualifying for conventional financing in today’s higher-rate environment.

Average Loan Sizes Move Lower

The average loan size for newly built homes also declined slightly in April.

According to MBA data:

- Average new home loan size in March: $381,938

- Average new home loan size in April: $378,384

The smaller loan amounts may indicate that buyers are adjusting budgets downward as affordability pressure increases.

Some buyers are shifting toward:

- Smaller homes

- Lower-cost markets

- More affordable suburban areas

- Entry-level new construction communities

Builders in several regions are also increasingly focusing on smaller floorplans and lower-priced inventory to attract buyers.

Inventory Levels Continue Rising

Unsold inventory remains elevated in many housing markets.

Over the past two years, builders increased construction activity to address ongoing housing shortages and capitalize on strong demand during earlier market conditions.

However, slower buyer activity combined with higher mortgage rates has created more supply in certain regions.

Housing economists say growing inventory may eventually help stabilize pricing pressure and improve affordability conditions.

Some markets are already seeing:

- Slower home price growth

- Increased builder concessions

- Longer selling times

- More buyer negotiating power

Affordability Remains the Biggest Challenge

Affordability continues to be the largest issue facing the housing market in 2026.

Even when home prices stabilize, higher mortgage rates significantly increase monthly ownership costs.

For many households, affordability challenges now include:

- Higher mortgage payments

- Rising insurance premiums

- Increased property taxes

- Inflation-driven living expenses

- Elevated utility and energy costs

These pressures are limiting purchasing power for many buyers.

Mortgage Rates Continue Creating Uncertainty

Mortgage rates have remained volatile throughout 2026 as financial markets react to inflation reports, Federal Reserve expectations, and global economic conditions.

Recent inflation data has reduced expectations for interest rate cuts later this year.

Some investors are now even considering the possibility of future Federal Reserve rate hikes if inflation remains elevated.

That outlook has contributed to higher Treasury yields and rising mortgage borrowing costs.

Builders Hope Demand Improves Later This Year

Despite weaker April numbers, many builders remain cautiously optimistic about the second half of 2026.

Industry analysts believe several factors could help improve activity later this year:

- Stabilizing mortgage rates

- Slower home price growth

- Increased inventory choices

- Rising wages

- Expanded builder incentives

Builders are also expected to continue adjusting pricing strategies and financing offers to maintain buyer interest.

New Construction Remains Important for Housing Supply

Even with slower sales activity, new home construction remains critical to addressing long-term housing shortages across the country.

Economists continue emphasizing that increasing housing supply is necessary to improve affordability over time.

New construction has become especially important in fast-growing regions where population growth continues exceeding available housing inventory.

While demand has softened temporarily, housing experts believe long-term demographic trends will continue supporting the need for additional residential development in the years ahead. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.