Mortgage Rates Show a Small Decline

Mortgage rates in the U.S. moved slightly lower today after rising earlier this week. This small drop may offer short-term relief for buyers and homeowners who are watching borrowing costs closely.

According to data from Zillow, fixed mortgage rates declined across several common loan terms.

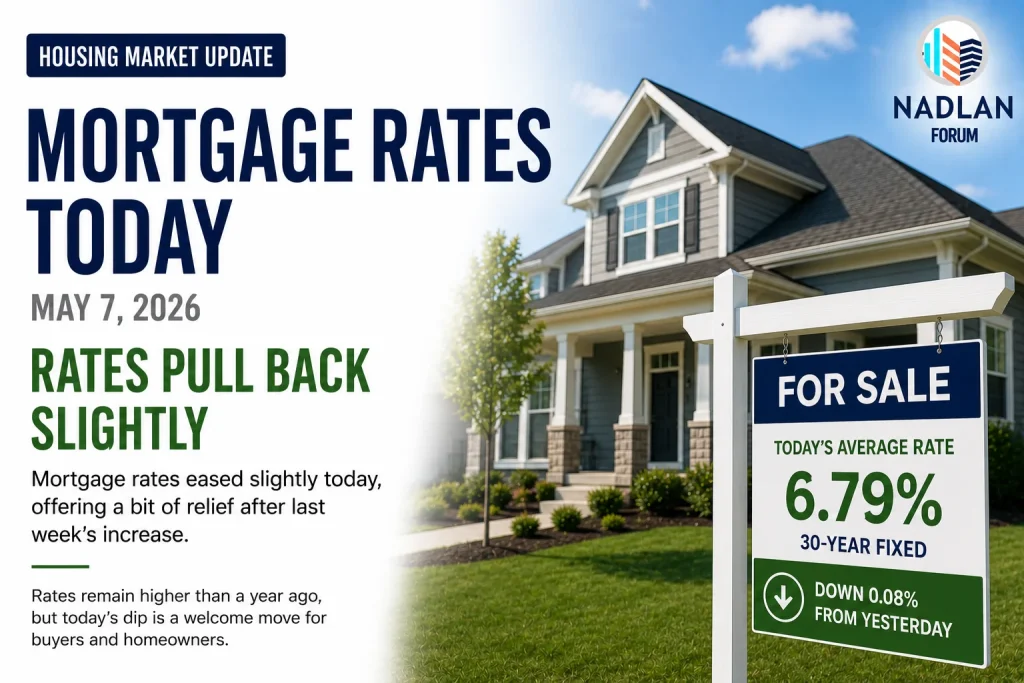

The 30-year fixed mortgage rate fell by five basis points to 6.26%. The 20-year fixed rate dropped to 6.12%, while the 15-year fixed rate declined to 5.60%. Although these changes are small, they show that rates can shift quickly based on market conditions.

Today’s Mortgage Rates

Here are the latest national average mortgage rates:

- 30-year fixed: 6.26%

- 20-year fixed: 6.12%

- 15-year fixed: 5.60%

- 5/1 ARM: 6.21%

- 7/1 ARM: 6.07%

- 30-year VA: 5.75%

- 15-year VA: 5.31%

- 5/1 VA: 5.28%

These rates are averages and may vary depending on location, lender, and borrower profile.

Today’s Refinance Rates

Refinance rates also showed mixed movement but remained close to purchase rates:

- 30-year fixed refinance: 6.27%

- 20-year fixed refinance: 6.24%

- 15-year fixed refinance: 5.76%

- 5/1 ARM refinance: 6.16%

- 7/1 ARM refinance: 6.17%

- 30-year VA refinance: 5.65%

- 15-year VA refinance: 5.15%

- 5/1 VA refinance: 5.19%

In general, refinance rates can be slightly higher than purchase rates, but the difference is not always large.

How Mortgage Rates Work

A mortgage rate is the cost you pay to borrow money from a lender, shown as a percentage. There are two main types of mortgage rates:

Fixed-Rate Mortgage

A fixed-rate mortgage keeps the same interest rate for the entire loan term. For example, if you choose a 30-year loan, your rate will not change during those 30 years. This provides stable monthly payments and makes budgeting easier.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a fixed rate for a set period, such as five or seven years. After that, the rate changes regularly based on market conditions.

For example, a 5/1 ARM keeps the same rate for five years, then adjusts once each year. While the starting rate is often lower, there is a risk that it may increase later.

What Affects Mortgage Rates

Mortgage rates depend on both personal and economic factors.

Factors You Can Control

- Credit score

- Debt-to-income ratio

- Down payment size

- Choice of lender

Borrowers with stronger financial profiles often qualify for lower rates.

Factors You Cannot Control

The broader economy also plays a major role. Inflation, job growth, and overall economic performance influence interest rates.

When the economy is strong, rates tend to rise to control spending. When growth slows, rates may fall to encourage borrowing.

30-Year vs 15-Year Mortgage

Two of the most common loan options are 30-year and 15-year fixed mortgages.

30-Year Mortgage

- Lower monthly payments

- Higher total interest over time

- More flexibility for budgets

15-Year Mortgage

- Higher monthly payments

- Lower interest rate

- Less total interest paid

Choosing between the two depends on your financial situation and long-term goals.

What This Means for Buyers

The small drop in mortgage rates may give buyers a bit more room in their budgets. Even a slight decrease can reduce monthly payments and improve affordability.

However, rates remain higher compared to past years, so buyers should still plan carefully and compare offers from different lenders.

Final Thoughts

Mortgage rates today on May 7, 2026, show a slight pullback after recent increases. While the change is small, it highlights how quickly the market can shift.

For buyers and homeowners, staying informed about rate trends and understanding loan options is key to making the right financial decision. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.