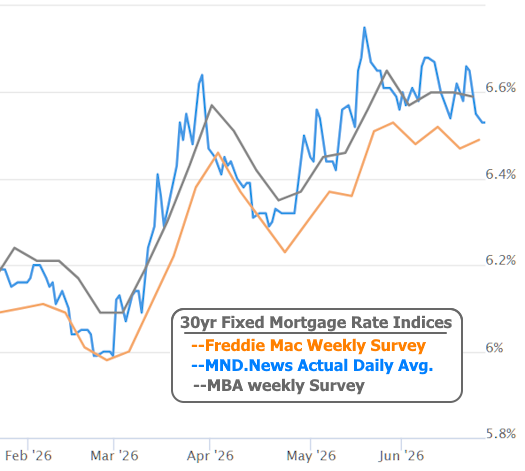

Mortgage rates ended the final full week of June on a positive note, reaching their lowest levels in more than a month despite the absence of any major economic or political headlines. Instead of reacting to a single news event, financial markets were driven by a combination of lower inflation pressures, declining oil prices, and increased demand for U.S. government bonds as institutional investors adjusted their portfolios before the end of the quarter.

For homebuyers and homeowners considering refinancing, the improvement provided welcome relief after several weeks of relatively elevated borrowing costs.

Although mortgage rates remain well above the historic lows seen during the pandemic, the recent decline suggests that financial markets are becoming more optimistic about inflation and future interest rate conditions.

Mortgage Rates Reach Their Best Levels Since Mid-May

After moving higher early in the week, mortgage rates reversed course and steadily improved during the second half of the week.

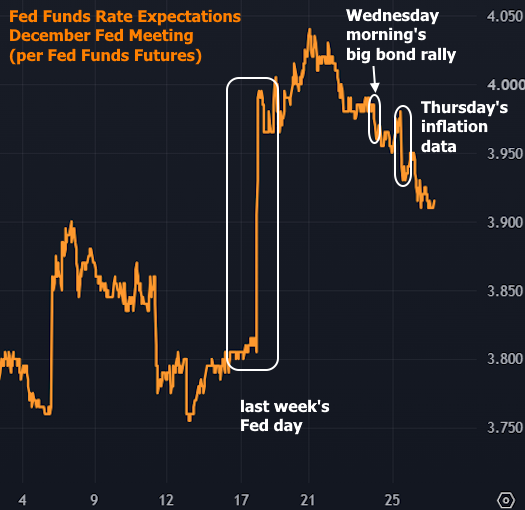

The strongest gains occurred on Wednesday and were largely maintained through Friday, allowing average mortgage rates to finish at their lowest point since the middle of May.

Unlike previous market swings that were triggered by major economic reports or geopolitical developments, this week’s improvement resulted from a combination of smaller market forces working together.

That made the decline especially notable because it reflected improving market conditions rather than a temporary reaction to unexpected news.

Bond Market Activity Drove Much of the Improvement

One of the biggest reasons mortgage rates declined was increased demand for U.S. Treasury bonds.

Mortgage rates closely follow movements in the bond market. When investors buy more bonds, bond prices rise while bond yields fall. Lower Treasury yields generally translate into lower mortgage rates for consumers.

During the final weeks of each financial quarter, many large investment firms rebalance their portfolios to maintain target allocations between stocks and bonds.

Since stock markets had significantly outperformed bond markets during recent months, many institutional investors increased their bond holdings before quarter-end.

This additional buying created downward pressure on interest rates throughout the week.

Quarter-End Portfolio Rebalancing Explained

Portfolio rebalancing is a routine investment practice used by pension funds, mutual funds, insurance companies, and other institutional investors.

For example, if a portfolio is designed to hold 60% stocks and 40% bonds, a strong stock market rally may shift that balance to 65% stocks and 35% bonds.

To restore the original allocation, investors sell a portion of their stock holdings and purchase additional bonds.

This increased demand for bonds often pushes bond yields lower, indirectly benefiting mortgage rates.

Although portfolio rebalancing receives less public attention than inflation reports or Federal Reserve meetings, it can still have a meaningful short-term impact on financial markets.

Inflation Data Also Supported Lower Rates

The week’s market performance also benefited from relatively encouraging inflation data.

Recent reports suggested that inflation continues moving gradually toward more stable levels, even though price pressures remain above the Federal Reserve’s long-term target.

Lower inflation generally improves bond market performance because investors become more confident that future interest rate increases are less likely.

As inflation expectations improve, long-term borrowing costs—including mortgage rates—often move lower.

Although inflation remains an important concern, the latest economic data provided markets with additional confidence that price pressures may continue easing during the second half of 2026.

Falling Oil Prices Helped Improve Market Sentiment

Energy prices also contributed to improving financial conditions.

Crude oil prices declined during the week as concerns surrounding global energy supplies eased and shipping activity through the Strait of Hormuz stabilized.

Lower oil prices can reduce transportation, manufacturing, and operating costs across the economy, helping slow inflation over time.

Because energy prices influence nearly every sector of the economy, declines in oil often improve investor confidence and support lower long-term interest rates.

While oil prices were not the primary reason mortgage rates declined, they added to the overall positive market environment.

A Quiet Week Still Produced Strong Results

Interestingly, much of the week’s improvement occurred without major scheduled market-moving events.

Monday saw rates move slightly higher without a clear explanation.

Tuesday was one of the quietest trading sessions in months.

Wednesday delivered the largest improvement as institutional bond buying accelerated.

Thursday’s inflation report initially helped bonds strengthen further before markets settled later in the day.

Friday remained relatively calm, allowing mortgage rates to hold onto nearly all of the week’s gains.

The absence of dramatic headlines demonstrates that financial markets sometimes move based on technical trading patterns and investor positioning rather than breaking news.

Investors Are Now Turning Their Attention to Economic Data

Although quarter-end trading supported mortgage rates this week, its influence is temporary.

Once institutional portfolio adjustments are complete, financial markets will return to focusing primarily on economic fundamentals.

Several important reports scheduled for early July could have a much larger influence on mortgage rates than quarter-end trading.

Among the most closely watched will be:

- Monthly employment data

- Labor market trends

- Wage growth

- Inflation reports

- Treasury bond yields

- Federal Reserve expectations

These indicators will help determine whether the recent decline in mortgage rates can continue.

The Jobs Report Could Be the Next Major Market Driver

The next monthly U.S. employment report is expected to become the most significant event for mortgage markets.

Because of the Independence Day holiday schedule, the report will be released on Thursday rather than its usual Friday publication.

Employment data plays a major role in determining interest rate expectations.

A stronger-than-expected labor market could increase concerns that inflation will remain elevated, potentially pushing mortgage rates higher.

Conversely, signs of moderating job growth could reinforce expectations that inflation will continue easing, allowing mortgage rates to remain stable or decline further.

As a result, many lenders and investors are expected to closely monitor the report before making major pricing adjustments.

What This Means for Homebuyers

The recent improvement in mortgage rates provides slightly better affordability for prospective homebuyers entering the market during the summer buying season.

Even relatively small declines in interest rates can reduce monthly mortgage payments and increase purchasing power, particularly on larger loan amounts.

While affordability challenges remain due to elevated home prices in many regions, lower financing costs may encourage more buyers to move forward with home purchases if rates continue improving.

Borrowers should still compare offers from multiple lenders, review Annual Percentage Rates (APR), and evaluate both fixed-rate and adjustable-rate loan options before locking in financing.

Final Thoughts

Mortgage rates finished the week at their lowest levels since mid-May, offering encouraging news for buyers and homeowners despite the lack of major market-moving headlines. Strong demand for U.S. Treasury bonds, quarter-end portfolio rebalancing, easing inflation concerns, and lower oil prices all contributed to improved borrowing conditions.

Looking ahead, the focus will quickly shift from technical market activity to upcoming economic reports, particularly the monthly employment data. Those reports will likely determine whether the recent decline in mortgage rates continues or whether borrowing costs begin moving higher again.

For now, the market appears to be moving in a favorable direction, giving borrowers a better opportunity to secure financing as the second half of 2026 begins. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.