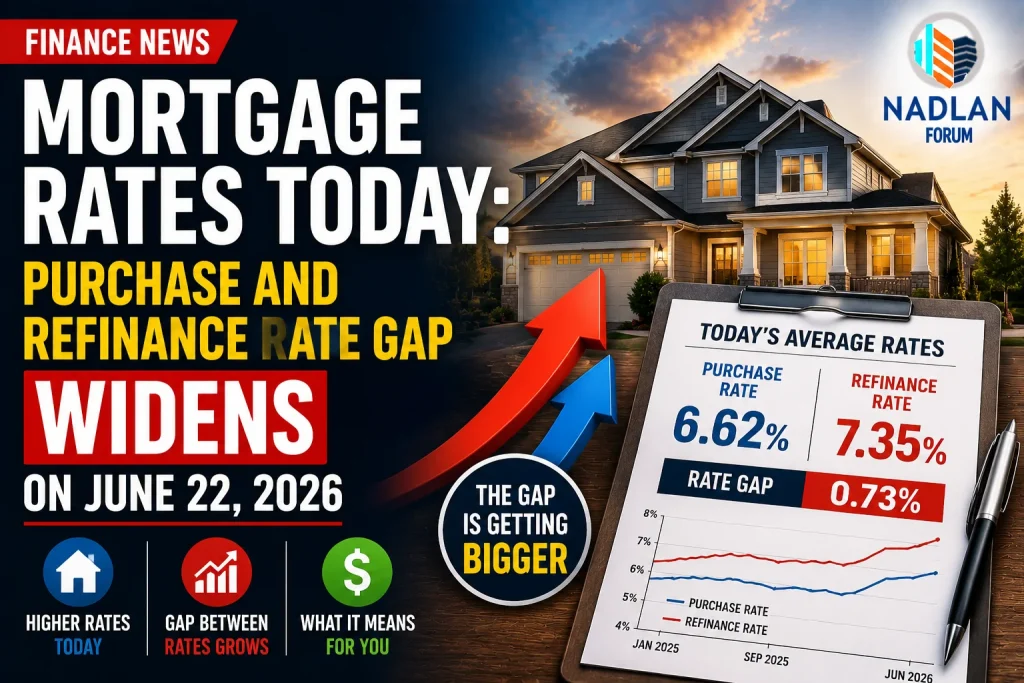

Mortgage rates delivered a mixed performance to start the week, with some loan products moving lower while others increased. One of the most notable developments was the growing difference between purchase mortgage rates and refinance rates, creating a changing landscape for both homebuyers and homeowners.

Although rates remain elevated compared with historical averages, recent fluctuations suggest lenders continue adjusting pricing in response to bond market activity, inflation expectations, and Federal Reserve policy outlooks.

For borrowers considering a home purchase or refinance, understanding today’s rate environment can help with timing and budgeting decisions.

Current Mortgage Rates for Home Purchases

Average mortgage rates for home purchases showed mixed movement across major loan categories.

Current average purchase rates include:

- 30-year fixed: 6.42%

- 20-year fixed: 6.14%

- 15-year fixed: 5.79%

- 5/1 ARM: 6.70%

- 7/1 ARM: 6.27%

- 30-year VA: 5.88%

- 15-year VA: 5.54%

- 5/1 VA: 5.57%

The benchmark 30-year fixed mortgage remains the most widely used home loan product because it offers stable payments and long-term predictability.

Meanwhile, adjustable-rate mortgages moved noticeably higher, making some ARM options less attractive than they have been in previous years.

Current Mortgage Refinance Rates

Homeowners exploring refinancing opportunities saw a slightly different trend.

Current average refinance rates include:

- 30-year fixed: 6.30%

- 20-year fixed: 6.51%

- 15-year fixed: 5.87%

- 5/1 ARM: 6.47%

- 7/1 ARM: 6.31%

- 30-year VA: 5.83%

- 15-year VA: 5.41%

- 5/1 VA: 5.53%

One interesting development is that refinance rates for several products remain below comparable purchase loan rates, particularly within the popular 30-year fixed category.

This widening gap has become an important trend for borrowers evaluating their financing options.

Why the Rate Spread Matters

The difference between purchase and refinance rates can influence homeowner decisions.

Traditionally, refinance loans often carry slightly higher rates due to lender pricing models and market conditions. However, market shifts occasionally reverse that relationship.

When refinance rates are lower than purchase rates, homeowners may find opportunities to:

- Reduce monthly payments.

- Change loan terms.

- Convert adjustable-rate mortgages into fixed-rate loans.

- Access home equity through cash-out refinancing.

However, borrowers should still compare closing costs and overall savings before moving forward.

30-Year Fixed Mortgage Remains the Industry Standard

The average 30-year fixed mortgage rate currently sits at 6.42%.

The popularity of this loan product comes from its combination of predictable payments and relatively affordable monthly costs.

Spreading repayment over three decades helps keep monthly obligations lower than shorter-term alternatives.

While borrowers pay more interest over the life of the loan, many households prefer the flexibility that comes with lower monthly payments.

For buyers focused on affordability, the 30-year fixed mortgage remains the most common choice.

15-Year Mortgages Continue to Offer Interest Savings

The average 15-year fixed mortgage rate is 5.79%.

Although monthly payments are higher, shorter loan terms provide significant long-term advantages.

Benefits of a 15-year mortgage include:

- Faster equity growth.

- Lower interest rates.

- Reduced lifetime interest costs.

- Earlier mortgage payoff.

For financially stable borrowers who can comfortably handle larger payments, a 15-year loan can create substantial savings over time.

Adjustable-Rate Mortgages Become Less Attractive

Adjustable-rate mortgages, commonly known as ARMs, experienced notable increases.

The average 5/1 ARM rose to 6.70%, placing it above many fixed-rate alternatives.

Traditionally, ARMs attract borrowers because they offer lower introductory rates. However, recent market conditions have narrowed or even eliminated that advantage.

Before choosing an ARM, borrowers should carefully compare available options and consider how long they plan to stay in the property.

For many buyers, today’s fixed-rate products may offer better value and greater payment certainty.

What Influences Mortgage Rates?

Mortgage rates are determined by several economic factors.

Key influences include:

- Inflation trends.

- Federal Reserve policy expectations.

- Treasury bond yields.

- Labor market conditions.

- Economic growth.

- Investor demand for mortgage-backed securities.

Although the Federal Reserve does not directly set mortgage rates, its policy decisions often influence broader financial markets and borrowing costs.

Recent market volatility surrounding inflation and future interest rate expectations has contributed to ongoing rate fluctuations.

Strategies for Securing a Lower Mortgage Rate

Borrowers have several ways to improve their chances of receiving competitive loan terms.

Improve Credit Scores

Higher credit scores generally qualify for lower mortgage rates.

Paying bills on time, reducing debt balances, and correcting credit report errors can help strengthen credit profiles.

Increase Your Down Payment

Larger down payments reduce lender risk and often lead to better interest rates.

Reduce Existing Debt

Lower debt-to-income ratios can improve loan eligibility and pricing.

Compare Multiple Lenders

Shopping around remains one of the most effective ways to secure a lower rate.

Even small differences between lenders can produce significant savings over the life of a mortgage.

Consider Discount Points

Borrowers can sometimes pay upfront fees to permanently lower their mortgage interest rate.

This strategy may make sense for homeowners planning to remain in the property for many years.

Will Mortgage Rates Fall Later in 2026?

Most industry forecasts suggest mortgage rates may remain within a relatively narrow range throughout the remainder of the year.

Many housing economists expect average 30-year mortgage rates to stay in the mid-6% range during 2026.

Future rate movements will largely depend on:

- Inflation performance.

- Economic growth.

- Labor market conditions.

- Federal Reserve policy decisions.

If inflation continues easing, mortgage rates could gradually improve. However, significant declines appear unlikely unless economic conditions change substantially.

What This Means for Homebuyers

For prospective buyers, current rates continue to present affordability challenges.

However, housing inventory has improved in many markets compared with recent years, creating more opportunities to negotiate on price and seller concessions.

Buyers who focus on improving their credit profiles and comparing lenders may be able to offset some of the impact of elevated rates.

What This Means for Homeowners

Homeowners considering refinancing should evaluate whether lower refinance rates provide meaningful savings.

Refinancing may be beneficial for those seeking to:

- Lower monthly payments.

- Change loan terms.

- Remove interest-rate uncertainty.

- Access home equity.

A careful review of closing costs and long-term savings remains essential before making a decision.

Bottom Line

Mortgage rates showed mixed movement on June 22, 2026, but one trend stood out: the growing gap between purchase and refinance rates. The average 30-year purchase mortgage remained above comparable refinance rates, creating opportunities for some homeowners while presenting continued affordability challenges for buyers.

As markets continue responding to economic data and Federal Reserve expectations, borrowers should stay informed, compare lenders, and evaluate their financial goals carefully before locking in a mortgage or refinance loan. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.