Unexpected expenses can happen at any time. A vehicle repair, medical bill, utility payment, or emergency home repair can quickly create financial pressure, especially when payday is still days away.

When cash is needed urgently, many people look at borrowing options such as payday loans or personal loans. While both provide access to money, they differ significantly in cost, repayment structure, qualification requirements, and long-term financial impact.

Understanding these differences can help borrowers make better financial decisions and avoid costly mistakes.

What Is a Personal Loan?

A personal loan is a type of installment loan offered by banks, credit unions, and online lenders. Borrowers receive a lump sum of money and repay it through fixed monthly payments over a set period.

Most personal loans have repayment terms ranging from two to seven years, although some lenders offer shorter or longer options.

Personal loans can be used for many purposes, including:

- Emergency expenses.

- Medical bills.

- Car repairs.

- Home improvements.

- Debt consolidation.

- Major purchases.

Because personal loans are typically unsecured, borrowers do not need to provide collateral such as a vehicle or savings account.

Benefits of Personal Loans

Lower Interest Rates

One of the biggest advantages of personal loans is their relatively low interest rates compared to payday loans.

Depending on credit qualifications, borrowers may receive rates ranging from approximately 7% to 36%.

This can result in significant savings over time.

Predictable Monthly Payments

Personal loans use installment payments, making budgeting easier.

Borrowers know exactly how much they owe each month and when the loan will be fully repaid.

Larger Loan Amounts

Many lenders offer personal loans ranging from $1,000 to $100,000.

This makes them useful for both small emergencies and larger financial needs.

Flexible Uses

Unlike some financing products that restrict how funds can be spent, personal loans can generally be used for nearly any legal purpose.

Drawbacks of Personal Loans

Credit Requirements

Most lenders review credit history before approving a loan.

Borrowers with poor credit may have fewer options or may qualify only for higher interest rates.

Higher Minimum Loan Amounts

Many lenders have minimum borrowing requirements, often around $1,000.

For someone who needs only a few hundred dollars, this can mean borrowing more than necessary.

Funding May Take Longer

While some lenders offer same-day funding, others may take several business days to process and release funds.

For urgent situations, that delay can be a disadvantage.

What Is a Payday Loan?

A payday loan is a short-term loan designed to provide quick cash until a borrower’s next paycheck arrives.

These loans are usually small, often ranging from $100 to $500.

Unlike personal loans, payday loans generally require repayment in full within two to four weeks.

Approval is typically based on proof of income rather than credit history.

Many lenders require:

- Recent pay stubs.

- Employment verification.

- An active checking account.

- Authorization for automatic repayment.

Because qualification standards are minimal, payday loans are often marketed toward borrowers with limited credit options.

Benefits of Payday Loans

Fast Access to Cash

One reason payday loans remain popular is speed.

Borrowers can often receive funds within minutes or hours after approval.

Limited Credit Requirements

Most payday lenders do not perform traditional credit checks.

This makes payday loans accessible to borrowers with damaged or limited credit histories.

Small Borrowing Amounts

Borrowers can request relatively small amounts, allowing them to cover immediate expenses without taking on a larger loan.

Drawbacks of Payday Loans

Extremely High Costs

The biggest concern with payday loans is cost.

Fees associated with these loans often translate into annual percentage rates exceeding 400%.

This makes payday loans one of the most expensive borrowing options available.

Very Short Repayment Period

Repayment is usually due within a few weeks.

For households already struggling financially, repaying the entire balance at once can be difficult.

Risk of Debt Cycles

Many borrowers are unable to repay the loan on time and end up renewing or rolling over the debt.

This creates additional fees and can trap borrowers in a cycle of repeated borrowing.

Single Lump-Sum Repayment

Unlike personal loans that allow monthly installments, payday loans generally require full repayment in one payment.

This can place significant strain on household finances.

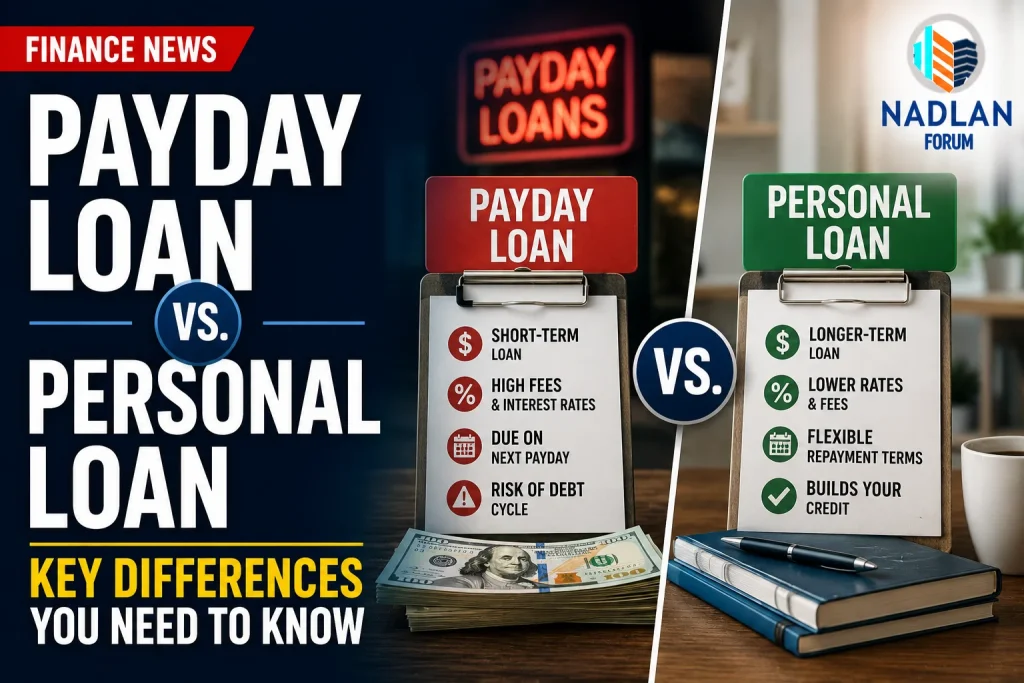

Payday Loan vs. Personal Loan: Major Differences

Cost

The largest difference between these two products is cost.

Personal loans generally offer substantially lower interest rates.

For example, a borrower taking out a personal loan may pay only a fraction of the interest and fees charged by a payday lender.

Payday loans can become extremely expensive even when borrowing relatively small amounts.

Repayment Structure

Personal loans are repaid through fixed monthly installments over several years.

Payday loans are usually repaid in one lump sum within a few weeks.

The installment structure of personal loans is often easier to manage.

Loan Amounts

Personal loans can provide thousands of dollars for larger expenses.

Payday loans are designed for smaller, short-term borrowing needs.

Qualification Requirements

Personal loan lenders typically review:

- Credit scores.

- Income.

- Employment history.

- Debt levels.

Payday lenders focus primarily on proof of income and an upcoming paycheck.

Funding Speed

Payday loans generally provide faster access to cash.

Personal loans may take longer but often offer significantly better terms.

Which Loan Is Better?

For most borrowers, a personal loan is usually the safer and less expensive choice.

Lower interest rates, predictable payments, and longer repayment periods make personal loans easier to manage financially.

Payday loans may provide quick cash, but the high costs and short repayment timelines can create long-term financial problems.

Whenever possible, borrowers should explore alternatives before considering a payday loan.

Alternatives to Payday Loans

If you need money quickly but want to avoid expensive payday loans, consider these options.

Credit Union Emergency Loans

Many credit unions offer small emergency loans with lower fees and more manageable repayment terms.

These loans are often designed specifically to replace payday lending products.

Employer Pay Advances

Some employers allow workers to access a portion of earned wages before payday.

This can provide immediate cash without borrowing from a lender.

Credit Card Cash Advances

A credit card cash advance may be expensive, but it is often still less costly than a payday loan.

Borrowers should review fees and repayment terms carefully before using this option.

Cash Advance Apps

Several financial apps allow workers to access a portion of earned wages before payday.

These services often charge lower fees than traditional payday lenders.

Selling Unused Items

Selling electronics, furniture, tools, clothing, or collectibles can generate quick cash without taking on debt.

Many online marketplaces make the process relatively simple.

How to Choose the Right Borrowing Option

Before taking out any loan, ask yourself several questions:

- How much money do I actually need?

- How quickly can I repay the debt?

- Can I qualify for a lower-cost option?

- What will the total borrowing cost be?

- Will the payment fit comfortably within my budget?

Taking time to compare options can help prevent financial stress later.

Bottom Line

Both payday loans and personal loans provide access to cash during financial emergencies, but they serve very different purposes.

Personal loans generally offer lower costs, longer repayment periods, and more manageable monthly payments. Payday loans provide fast cash and easier approval but come with extremely high fees and significant repayment risks.

For most borrowers, a personal loan or another lower-cost alternative is usually the better choice. Understanding the true cost of borrowing can help you protect your finances and avoid unnecessary debt. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.