The U.S. housing market is facing a new challenge as foreclosure activity continues increasing after several years of historically low default rates. Rising mortgage payments, higher insurance premiums, increasing property taxes, and elevated living costs are putting additional pressure on some homeowners who are struggling to keep up with monthly expenses.

While foreclosure levels remain below the housing crisis period of the late 2000s, recent data shows that default activity has climbed to its highest point in nearly seven years.

For buyers and investors, the increase in distressed properties creates potential opportunities. However, foreclosed homes often come with significant risks, including repair costs, financing challenges, and legal complications.

Foreclosure Rates Reach Highest Level in Years

Foreclosure activity has been steadily increasing after remaining unusually low during and immediately after the pandemic.

Government assistance programs, mortgage payment protections, and rising home equity helped many homeowners avoid default during previous years.

However, those protections have largely ended, and financial pressure has increased.

By early 2026, the national new foreclosure rate reached approximately 0.24%, approaching levels last seen before the pandemic.

Although this remains far below historical crisis levels, the upward trend reflects growing affordability challenges affecting certain homeowners.

Why Foreclosures Are Increasing

Several factors are contributing to the rise in foreclosure activity.

The biggest pressures include:

- Higher mortgage payments

- Rising property insurance costs

- Increased property taxes

- Higher everyday expenses

- Slower wage growth compared with housing costs

- Limited homeowner equity for recent buyers

Many homeowners who purchased after 2021 entered the market with much higher prices and interest rates compared with earlier buyers.

Because mortgage payments are structured so that borrowers pay more interest during the early years of the loan, newer homeowners often have built less equity than long-term owners.

Recent Buyers Face Greater Risk

Homeowners who purchased properties after 2023 may face greater financial vulnerability.

Many of these buyers:

- Bought near peak price levels

- Started mortgages with higher interest rates

- Have less accumulated home equity

- May have fewer options if financial problems occur

If home values decline in certain areas, some recent buyers could face the risk of becoming underwater, meaning they owe more on their mortgage than the home is currently worth.

This situation can make selling the property more difficult if homeowners experience financial hardship.

What Are REO Properties?

When a home does not sell at a foreclosure auction, it can become a Real Estate Owned (REO) property.

An REO property is owned by the lender and is typically placed back on the market for sale.

These properties are usually sold:

- In their current condition

- Without major repairs

- Without traditional seller improvements

For investors and experienced buyers, REO homes may offer discounted purchase opportunities.

However, buyers must carefully evaluate the property’s condition before making an offer.

Foreclosed Homes Can Sell Below Market Value

Distressed properties often attract investors because of potential discounts.

Recent data shows that REO properties sold for approximately 27.2% below estimated market value.

However, lower prices often reflect additional costs and risks.

Buyers may need to account for:

- Renovation expenses

- Property damage

- Delayed maintenance

- Insurance difficulties

- Financing challenges

- Legal requirements

A lower purchase price does not always mean a lower total investment.

Foreclosure Listings Represent More Inventory

Foreclosed homes currently represent a small but growing portion of the housing market.

In April 2026:

- REO properties represented approximately 1.3% of active listings nationwide

- These homes received significantly more online attention than traditional listings

- They typically remained on the market longer

REO properties received approximately 26.5% more online views compared with standard listings, showing strong buyer interest.

However, they stayed listed about 11 additional days longer, partly because buyers need more time to evaluate repairs and risks.

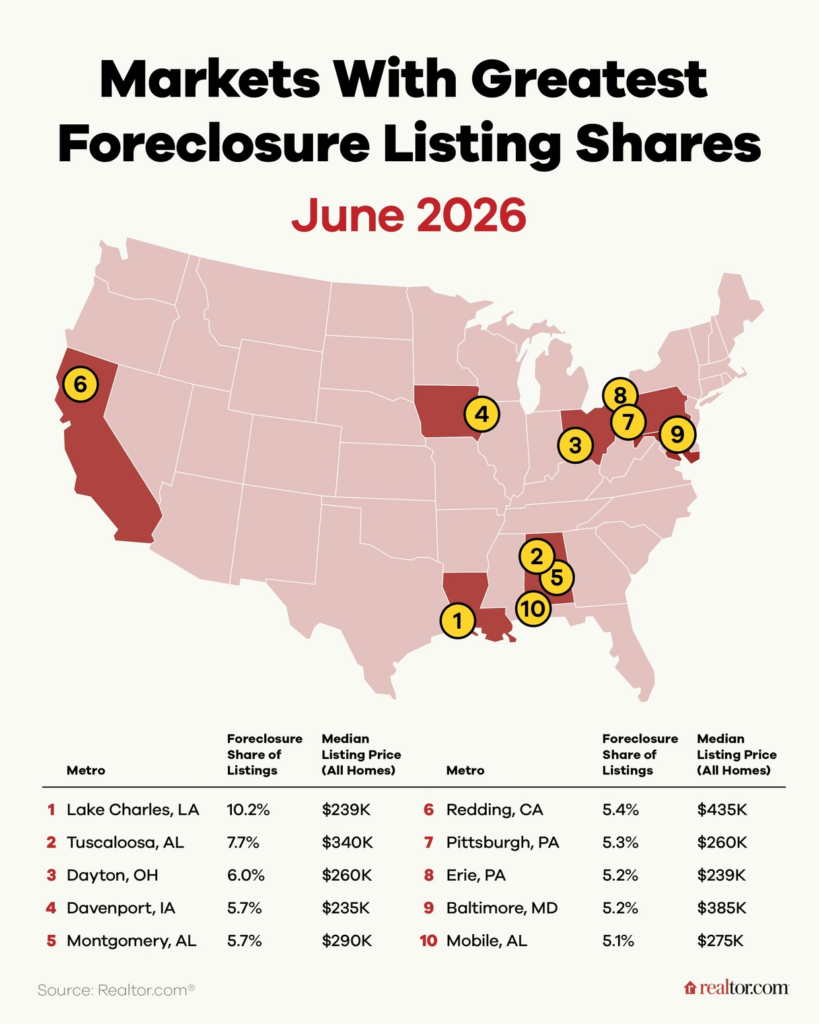

Markets With the Highest Share of Foreclosure Listings

Foreclosure activity varies significantly across different regions.

The markets with the largest share of foreclosure listings include:

- Lake Charles, Louisiana — 10.2%

- Tuscaloosa, Alabama — 7.7%

- Dayton, Ohio — 6.0%

- Davenport, Iowa — 6.0%

- Montgomery, Alabama — 5.7%

Although larger cities may have more total foreclosure properties, smaller and more affordable markets often experience higher foreclosure percentages.

Why Smaller Markets Are Seeing More Pressure

Many markets with higher foreclosure rates share similar characteristics:

- Lower home prices

- More first-time homeowners

- Lower household incomes

- Greater exposure to rising costs

Affordable housing markets often allow more households to transition from renting into ownership.

However, buyers with limited financial flexibility may have fewer resources available when unexpected costs arise.

This creates a situation where affordability helps people buy homes but can also increase vulnerability during financial stress.

Lake Charles Faces Unique Challenges

Lake Charles, Louisiana, currently has one of the highest foreclosure rates in the country.

Local housing challenges have been influenced by several factors, including:

- Severe weather events

- Rising insurance costs

- Repair expenses

- Inflation pressures

- Increasing household costs

Following major storms, some homeowners faced long insurance claim processes and significant out-of-pocket repair expenses.

For some families, these financial challenges became difficult to overcome.

Insurance Costs Become a Growing Concern

Insurance affordability has become an increasingly important issue for homeowners and buyers.

In areas vulnerable to storms or natural disasters, rising premiums can significantly increase monthly housing costs.

For distressed properties, insurance can create additional challenges because:

- Older homes may require repairs before coverage is available

- Damaged properties may be harder to insure

- Premiums may reduce affordability

Buyers considering foreclosed homes should investigate insurance availability before completing a purchase.

Opportunities for Investors

Foreclosures can create opportunities for experienced real estate investors.

Potential advantages include:

- Lower purchase prices

- Renovation opportunities

- Equity creation

- Rental investment potential

- Value-add strategies

Investors who have:

- Reliable contractors

- Renovation experience

- Cash reserves

- Knowledge of local markets

are often better positioned to handle distressed properties successfully.

Risks Buyers Should Understand

Foreclosure purchases require careful preparation.

Common risks include:

Property Condition

Many foreclosed homes have been vacant for extended periods and may experience:

- Water damage

- Mold issues

- Plumbing problems

- Electrical problems

- Deferred maintenance

Financing Challenges

Some distressed properties may not qualify for traditional financing if they require significant repairs.

Legal Complications

Certain states have unique foreclosure laws that can create additional risks for buyers.

Understanding local regulations is essential before purchasing a foreclosure property.

Alabama Buyers Need Extra Caution

Some states have additional legal protections that can affect foreclosure purchases.

In Alabama, buyers should understand the possibility of a statutory redemption period.

This allows previous homeowners under certain conditions to reclaim the property after foreclosure by meeting specific legal requirements.

Because of these rules, buyers must carefully research the process before investing.

What Foreclosures Mean for the Housing Market

The increase in foreclosure activity does not indicate a repeat of the 2008 housing crisis.

Today’s market differs significantly because:

- Most homeowners have substantial equity

- Mortgage underwriting standards are stronger

- Supply remains limited in many regions

- Foreclosure levels remain historically moderate

However, the increase highlights growing affordability challenges affecting certain segments of homeowners.

Impact on Homebuyers

For buyers, distressed properties may provide opportunities to purchase below traditional market prices.

However, buyers should:

- Complete inspections

- Estimate repair costs

- Research title issues

- Confirm insurance availability

- Understand local foreclosure laws

- Avoid focusing only on the purchase price

A discounted property can become expensive if hidden problems are overlooked.

Impact on Real Estate Investors

Investors may find increased opportunities as foreclosure activity rises.

Potential strategies include:

- Fix and flip projects

- Rental property acquisitions

- Value-add renovations

- Long-term investment purchases

However, successful investors must evaluate the complete financial picture, including repairs, financing, taxes, insurance, and holding costs.

Looking Ahead

Foreclosure activity is likely to remain an important housing market trend as affordability pressures continue.

Rising insurance costs, higher monthly payments, and elevated living expenses may create additional challenges for financially vulnerable homeowners.

At the same time, distressed properties may provide opportunities for prepared buyers and investors who understand the risks involved.

The current foreclosure increase reflects a housing market adjusting after several unusual years. While it does not represent a return to the housing crash era, it highlights the growing importance of affordability, financial planning, and careful decision-making in today’s real estate environment. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.