The real estate market in 2026 is fast-moving, complex, and more competitive than ever before. Investors and developers face greater challenges and opportunities, making the choice of banking partner crucial to success.

In this article, we uncover the top 10 real estate banks to know in 2026. Each bank offers distinct features, financing options, and digital tools designed specifically for property professionals.

We will compare established institutions and digital innovators, highlight their strengths, and provide practical tips to help you choose the best fit for your goals. Ready to navigate the future of real estate banking with confidence? Let’s get started.

What Makes a Top Real Estate Bank in 2026?

Selecting the right real estate banks has never been more critical. In 2026, property professionals face a rapidly changing financial landscape. The best real estate banks meet modern demands with innovation, flexibility, and robust security.

Evolving Needs of Real Estate Investors and Developers

In 2026, real estate banks must keep pace with the increasing complexity of property transactions. Investors and developers now demand digital-first solutions for portfolio management, seeking faster, more flexible financing options.

As portfolio sizes grow, scalability is vital. Digital real estate banks offer sub-accounts for each property, making it easier to track income and expenses. According to the U.S. real estate market outlook 2026, investment activity and sector performance are driving banks to innovate at a record pace.

The ability to handle diverse, multi-property portfolios is now a baseline expectation for leading real estate banks.

Essential Banking Features for Real Estate

Top real estate banks stand out by offering no or low monthly fees, high-yield accounts, and integrated rent collection tools. Dedicated sub-accounts for security deposits and operating expenses help landlords stay organized.

Key features include built-in bookkeeping, automated expense categorization, and multiple payment options such as ACH, wires, checks, and cards. These features streamline operations and improve cash flow management.

For real estate banks to remain competitive, seamless digital functionality and landlord-focused solutions are non-negotiable.

Financing Options and Lending Capabilities

Financing is a cornerstone for all real estate banks. The best institutions provide a range of products, including commercial real estate (CRE) loans, DSCR loans, and flexible lines of credit.

Traditional banks offer breadth and stability, while fintechs stand out for their speed. For instance, Bluevine’s $250,000 line of credit appeals to those needing quick access to capital. In contrast, traditional real estate banks excel in larger, long-term CRE loans.

A bank’s lending capabilities can make or break an investor’s growth strategy, so detailed comparison is essential.

Customer Support and Technology Integration

Customer support and technology are equally important when evaluating real estate banks. Investors expect 24/7 access to responsive service and robust online platforms.

Integration with property management and accounting software is now standard. Platforms like Baselane and Stessa provide all-in-one dashboards, enabling multi-user access and real-time financial tracking.

Real estate banks with strong tech integration help investors save time and reduce errors during portfolio management.

Security, Compliance, and Risk Management

Security and compliance are top priorities for real estate banks in 2026. FDIC insurance, often up to $3M, provides peace of mind. Advanced fraud protection and transparent fee structures are essential.

Banks must also maintain clear lending criteria and adhere to evolving regulatory standards. Comprehensive risk management practices ensure both investors and institutions are protected in a dynamic market.

As expectations rise, only real estate banks with robust security and compliance measures will earn lasting trust.

Top 10 Real Estate Banks to Know in 2026

Navigating the world of real estate banks in 2026 can be overwhelming, with both established players and digital newcomers reshaping the landscape. The right banking partner can streamline your operations, boost your returns, and help you scale confidently.

This curated list highlights the top 10 real estate banks to consider, each offering a unique mix of features, financing, and technology for property professionals. Comparing these banks side by side will empower you to find the best match for your investment goals. For a broader view of the industry, see the Top multifamily finance firms 2026 for more on leading lenders and their market positions.

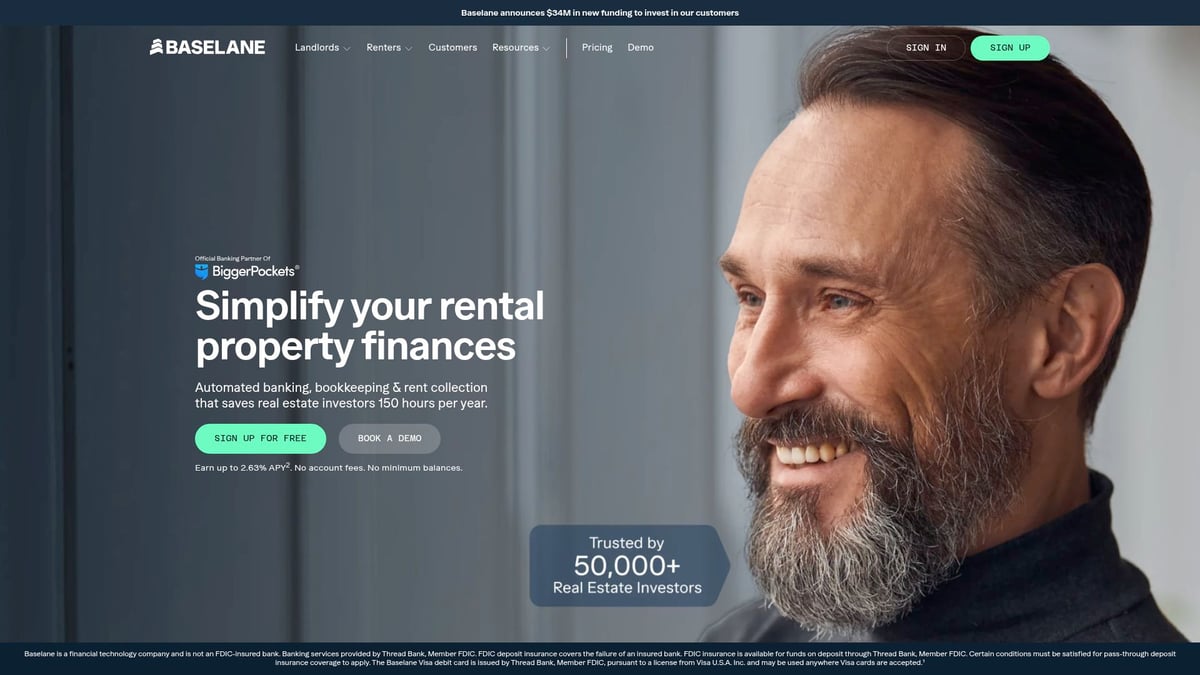

1. Baselane

Baselane stands out among real estate banks with its all-in-one platform designed specifically for landlords and investors. With $0 monthly fees, no minimum balance, and up to 2.63% APY, it’s a cost-effective solution for property professionals.

Core features include unlimited property-specific accounts, integrated rent collection, virtual and physical debit cards, and built-in bookkeeping. Baselane’s automation tools make expense tracking and tax reporting straightforward.

Ideal for: Small to midsize landlords, portfolio investors, and property managers seeking scalable banking.

Pros: No fees, high yield, tailored for real estate, scalable for growth.

Cons: No physical branches, limited to the U.S. market.

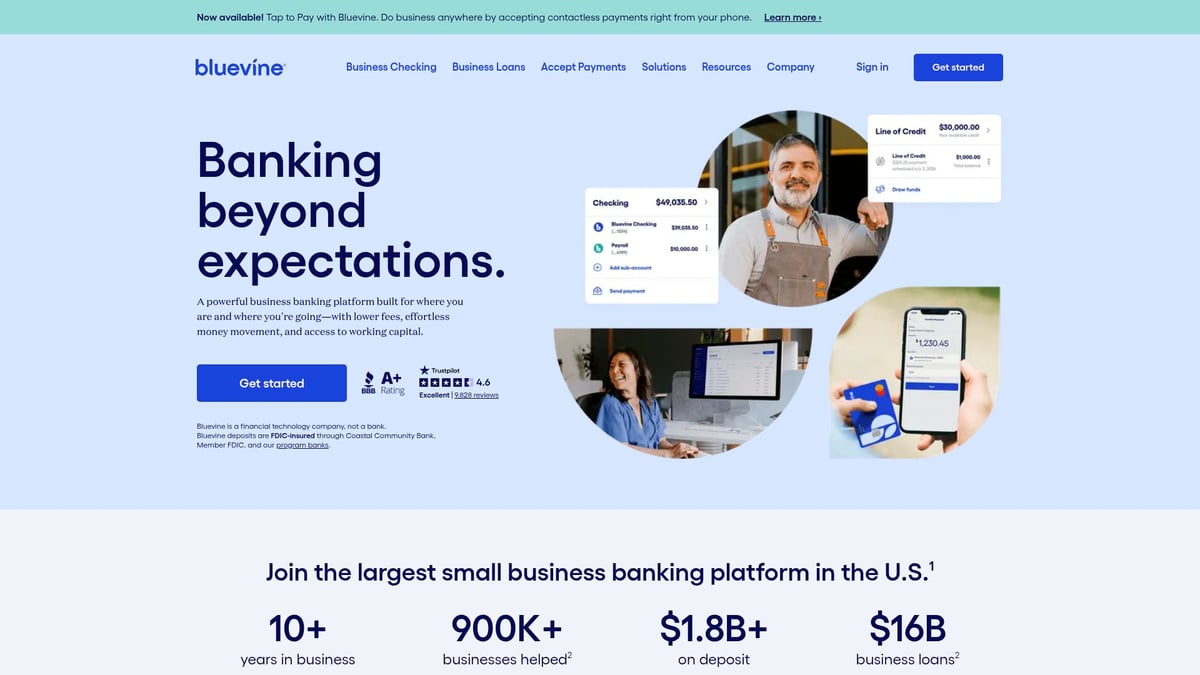

2. Bluevine

Bluevine is a digital-first leader among real estate banks, offering flexible business banking and fast lending. With pricing from $0 to $95+ per month and up to 4.25% APY, it appeals to investors needing agility.

Key features include up to 20 sub-accounts, a line of credit up to $250,000, and virtual debit cards. Bluevine’s streamlined online interface supports quick financing decisions.

Ideal for: Small business owners, investors requiring flexible credit.

Pros: Competitive rates, robust lending, easy-to-use digital tools.

Cons: Limited landlord-specific features, cap on sub-accounts.

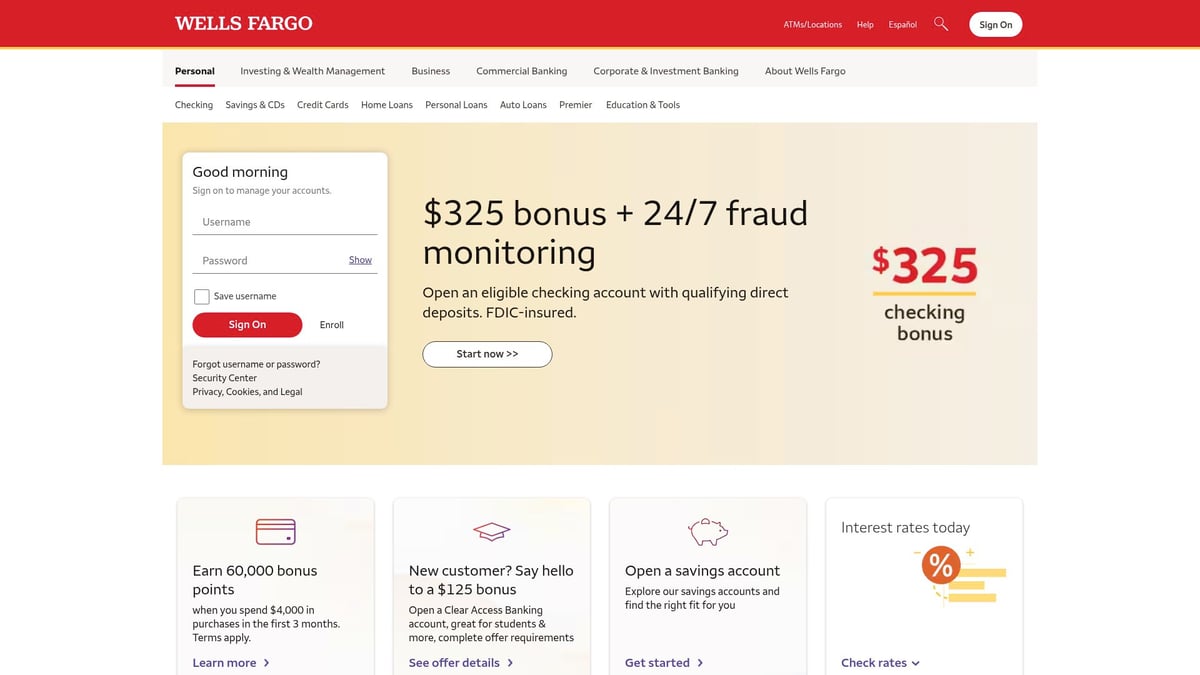

3. Wells Fargo

Wells Fargo is a traditional powerhouse in real estate banks, providing extensive commercial real estate (CRE) loan products and a nationwide branch network. Account pricing varies, with possible monthly fees or waivers.

Features include cash management solutions and a wide array of loan offerings. In-person support and relationship banking are key strengths.

Ideal for: Large-scale investors, developers, and those preferring in-person service.

Pros: Trusted brand, comprehensive lending, physical presence.

Cons: Higher fees, less digital automation compared to newer real estate banks.

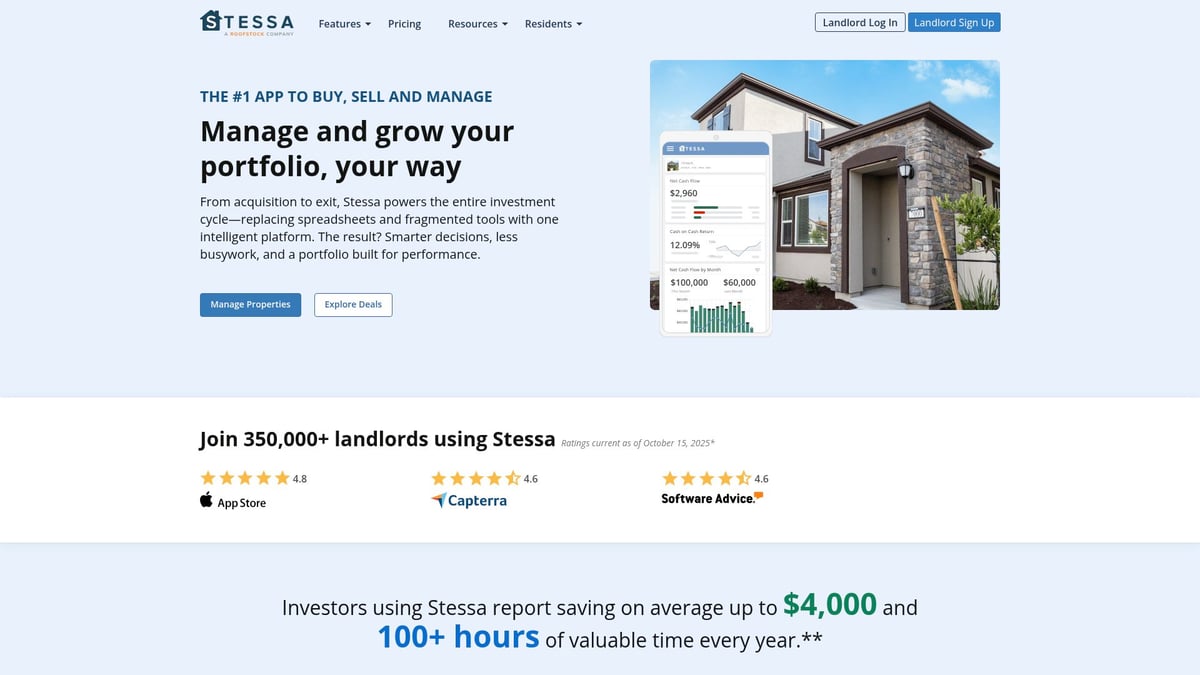

4. Stessa

Stessa brings digital innovation to real estate banks with free banking, up to 3.49% APY, and property-specific accounts. It integrates bookkeeping, automated rent collection, and tenant payment options in a single dashboard.

Landlords benefit from seamless accounting, cash flow tracking, and tax-ready reports. The platform is landlord-focused, making it easy to manage multiple properties.

Ideal for: Landlords with growing portfolios, tech-forward investors.

Pros: Free banking, integrated analytics, automation for taxes.

Cons: Deposit limits, fewer financing options than other real estate banks.

5. Relay Bank

Relay Bank offers flexibility and control for teams within real estate banks. With pricing from $0 to $90+ per month and up to 2.86% APY, it supports up to 20 checking accounts and 50 debit cards.

Multi-user access and basic bookkeeping help manage expenses and streamline operations. Relay’s digital-first platform is ideal for collaborative investing.

Ideal for: Investors with teams, property managers, small businesses.

Pros: Account controls, digital experience, team management.

Cons: No built-in rent collection, caps on accounts.

6. Bank of America

Bank of America remains a top choice among real estate banks for established investors and developers. Monthly fees may apply, but waivers are available for qualifying balances.

Core offerings include CRE loans, business checking and savings, and a broad branch network. Relationship banking and large-scale financing are key advantages.

Ideal for: Established investors, commercial developers.

Pros: National reach, robust lending, diverse account options.

Cons: High balance requirements, lower APY, potential fees for smaller accounts.

7. Axos Bank

Axos Bank is a digital-only contender in real estate banks, offering efficient account setup and competitive rates. With pricing from $0 to $10 per month, investors benefit from high-yield options and no minimum balance requirements.

Axos provides business and real estate loans, cash management tools, and a streamlined online experience. Remote investors find its digital approach highly efficient.

Ideal for: Investors seeking efficiency, remote property owners.

Pros: Low fees, tech-driven platform, real estate lending.

Cons: No physical branches, limited landlord-specific tools compared to other real estate banks.

8. U.S. Bank

U.S. Bank is known for its specialized support within real estate banks, offering CRE lending, property management accounts, and a dedicated real estate team. Pricing varies, with waivable monthly fees.

Custom lending solutions and strong compliance are key draws. U.S. Bank excels in regional expertise and relationship-driven banking.

Ideal for: Investors in U.S. markets needing specialized support.

Pros: Relationship banking, large loan portfolio, compliance.

Cons: Fees for smaller accounts, slower digital innovation than some real estate banks.

9. Capital One

Capital One combines digital banking with flexible lending for real estate banks. Pricing ranges from $0 to $35 per month, with waivable fees and business account options.

Features include CRE financing, business credit cards, and a modern online interface. Business rewards programs add extra value for mixed-use investors.

Ideal for: Mixed-use investors, businesses seeking rewards.

Pros: Competitive products, advanced digital tools, business rewards.

Cons: Limited landlord features, branch network is not nationwide compared to other real estate banks.

10. Ally Bank

Ally Bank rounds out the list of top real estate banks with a no-fee, online-only model. Investors benefit from competitive APY, easy online management, and quick loan approvals.

Ally offers business and real estate loans, high-yield savings, and a user-friendly digital interface. It’s best suited for tech-savvy investors and small business owners.

Ideal for: Tech-focused investors, small business owners.

Pros: No fees, strong savings rates, efficient online platform.

Cons: No in-person service, fewer real estate-specific tools than some other real estate banks.

Quick Comparison Table

| Bank Name | Fees | APY (up to) | Physical Branches | Key Feature |

|---|---|---|---|---|

| Baselane | $0 | 2.63% | No | Unlimited property accounts |

| Bluevine | $0–$95+ | 4.25% | No | Fast lending, sub-accounts |

| Wells Fargo | Varies | N/A | Yes | Nationwide CRE lending |

| Stessa | $0 | 3.49% | No | Bookkeeping integration |

| Relay Bank | $0–$90+ | 2.86% | No | Team expense controls |

| Bank of America | Varies | Low | Yes | Relationship banking |

| Axos Bank | $0–$10 | High | No | Digital-first efficiency |

| U.S. Bank | Varies | Low | Yes | Specialized CRE support |

| Capital One | $0–$35 | Medium | Limited | Digital rewards banking |

| Ally Bank | $0 | High | No | Online-only savings/lending |

These ten real estate banks offer a spectrum of solutions, whether you prioritize digital convenience, in-person support, or specialized lending. Review your needs carefully to identify the best fit for your real estate journey.

How to Choose the Right Real Estate Bank for Your Needs

Selecting the right real estate banks is a pivotal decision that can shape your investment journey for years to come. With the market evolving rapidly, aligning your banking partner to your goals, property type, and growth strategy is more critical than ever.

Start by clarifying your investment approach. Are you focused on long-term rentals, flipping properties, commercial assets, or residential portfolios? Each strategy demands different features from real estate banks, such as flexible lending for flippers or robust loan products for commercial investors.

Next, consider the size and complexity of your portfolio. If you manage multiple units or properties, look for banks with unlimited sub-accounts, built-in bookkeeping, and automated rent collection. For investors with high transaction volumes, digital banks often provide streamlined tools that can simplify your workflow.

Here are key factors to weigh when comparing real estate banks:

- Account Fees & APY: Evaluate monthly charges, interest rates, and minimum balance requirements.

- Lending Options: Assess the availability of CRE loans, lines of credit, and refinancing solutions.

- Digital Tools: Look for integrated rent collection, expense tracking, and property management software compatibility.

- Customer Support: Decide if in-person service or 24/7 online access is more important for your operations.

- Security & Compliance: Confirm FDIC insurance limits and transparent fee structures.

International investors may face unique challenges when opening or managing accounts. For example, Banking in the US for Israeli Investors outlines practical tips and regulatory considerations for accessing US real estate banks from abroad.

Finally, many investors now prefer banks with integrated expense tracking, especially as refinancing and forbearance trends shift. According to FHFA Data Shows Rise in Forbearance and Refinancing, the ability to manage loan adjustments efficiently has become a top priority, reinforcing the value of digital-first real estate banks with robust reporting features.

Real Estate Banking Trends to Watch in 2026

The landscape for real estate banks is evolving rapidly in 2026. Investors and developers are demanding more from their banking partners, prompting both fintechs and traditional institutions to innovate at record speed.

What trends are shaping real estate banks this year? Here are the key developments every property professional should follow:

- All-in-one digital banking platforms: Seamless dashboards integrating rent collection, bookkeeping, and cash management are now a must-have. Platforms like Baselane and Stessa are leading the way for landlords seeking efficiency.

- Fierce competition for CRE lending: Both fintechs and established real estate banks are racing to offer flexible, fast commercial real estate loans. According to Real estate M&A trends 2026, capital rotation and AI integration are accelerating product development and deal flow.

- Enhanced security and compliance: Multi-factor authentication, real-time fraud alerts, and higher FDIC insurance limits (now up to $3M at some banks) are becoming industry standards.

- Integrated rent collection and automated bookkeeping: Real estate banks are embedding these tools to help property owners manage income and expenses with minimal manual effort.

- Expansion of ESG lending: There is a growing demand for Environmental, Social, and Governance loan products, encouraging banks to support sustainable property investments.

- Tokenization and investment accessibility: As highlighted in Real estate tokenization trends 2026, digital assets are making fractional ownership and global real estate investments more accessible.

With CRE loan portfolios in top real estate banks growing over 30% year-over-year (2021 data), these trends are set to define industry leaders. Staying ahead means choosing a bank that not only offers cutting-edge features but also anticipates the next wave of innovation.

After exploring the top real estate banks and seeing how features like flexible financing, digital tools, and streamlined support can make a real difference, you might be thinking about your next step. If you’re ready to put these insights into action and secure the right financing for your property goals in the US, you don’t have to navigate it alone. The Nadlan Forum is here to support you every step of the way. Take the first step toward making your investment plans a reality—Get a mortgage in the US today.