FHFA Data Shows Rise in Forbearance and Refinancing as Mortgage Rates Fall

The latest data from the Federal Housing Finance Agency (FHFA) reveals an uptick in mortgage forbearance and refinancing in October 2025, as rates continued to decrease. While these trends signal relief for some homeowners, they also show ongoing challenges for others who are still grappling with affordability and long-term housing stability.

Increase in Foreclosure Prevention Efforts

In October 2025, Fannie Mae and Freddie Mac took 17,032 foreclosure prevention actions, raising the total to over 7.28 million since conservatorships began in 2008. Of these actions, nearly 39% were permanent loan modifications, reflecting the ongoing efforts to keep homeowners in their homes despite economic challenges.

The number of permanent loan modifications in October reached 7,210, bringing the total to 2.82 million. Notably, 64% of these modifications involved principal forbearance, while 36% were adjustments that extended loan terms. The increase in payment deferrals suggests that many borrowers are still facing financial difficulty, with the number of borrowers receiving deferrals rising from 5,616 in September to 6,208 in October.

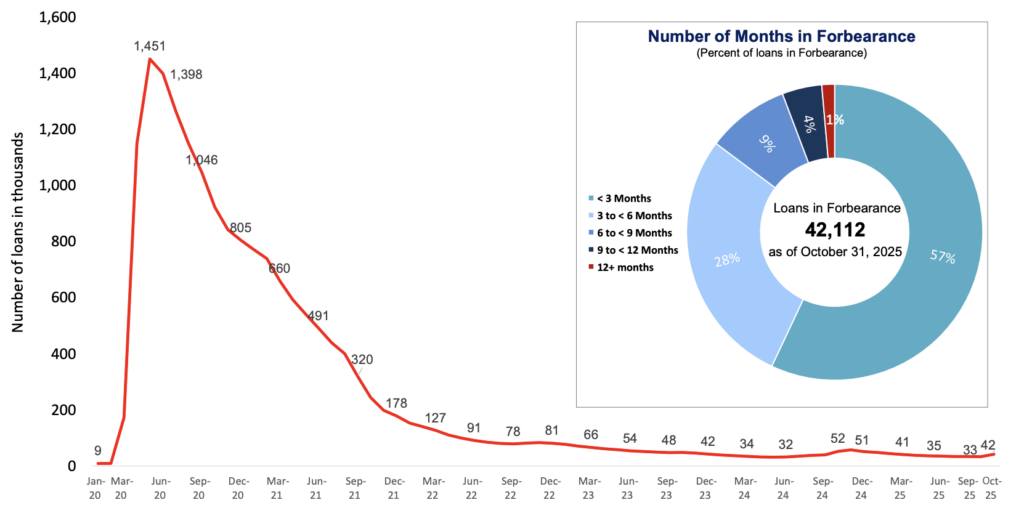

Forbearance Plans on the Rise

October saw a significant surge in forbearance plans, with the number of new plans starting at 17,075, a dramatic increase from 7,863 in September. By the end of the month, 42,112 loans were in active forbearance, compared to 33,360 in September. Although forbearance remains a small percentage of the overall market, it reflects ongoing financial strain for some borrowers.

At the end of October, about 0.14% of all serviced loans were in forbearance, and 8% of delinquent loans were under forbearance plans. Notably, only 1.4% of loans had been in forbearance for more than 12 months, which suggests that most borrowers are able to resolve their payment issues within a year.

Refinancing Activity Gets a Boost

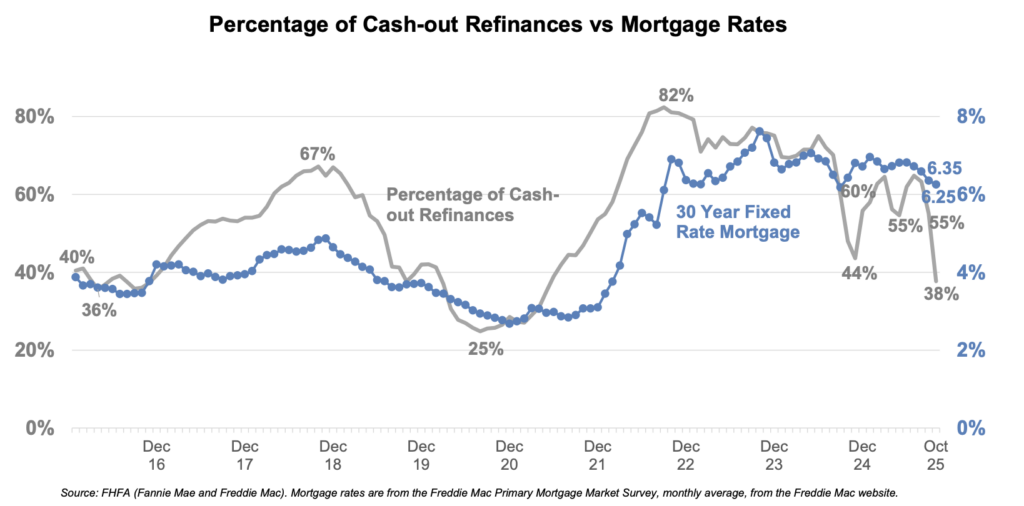

As mortgage rates continued to decline, refinancing activity increased in October 2025. The average 30-year fixed mortgage rate fell from 6.35% in September to 6.25% in October, which led to a rise in refinancing applications.

However, cash-out refinances as a share of total refinances dropped from 55% in September to 38% in October, signaling a shift in borrower behavior. The drop in cash-out refinances is significant because this type of refinance had reached a high of 82% in recent years.

Additionally, 15-year mortgage refinances accounted for just 17% of total refinances in October, down from previous months. This drop is largely due to a narrowing rate spread between 15-year and 30-year mortgages, making shorter terms less appealing for many homeowners.

Mortgage Delinquencies Remain Low

Despite the rise in forbearance activity, mortgage delinquencies remained low. The percentage of loans 30 to 59 days delinquent dropped to 0.93%, while the rate for serious delinquencies (loans 90+ days late) stayed at 0.55%. These figures suggest that while some homeowners are still struggling, the overall health of the housing market remains stable.

In addition, foreclosure starts increased by 3% to 9,255 in October, and the number of third-party and foreclosure sales rose by 13%, reaching 1,317. While these numbers reflect a slight increase in foreclosure activity, they are still far below the peaks seen during the last financial crisis.

What It Means for Homebuyers and Homeowners

The FHFA’s report provides a snapshot of a housing market that is showing signs of stabilization, albeit with ongoing challenges. Forbearance and refinancing activity have been boosted by lower mortgage rates, but homeowners are still dealing with affordability issues, particularly in the face of high home prices.

The increase in refinancing reflects the benefits of falling mortgage rates for some borrowers, but for others, especially those still relying on forbearance, the path forward remains uncertain. With home prices still rising in certain regions, the affordability gap continues to put pressure on homebuyers, especially in high-demand areas.

While the market is moving in a positive direction for many, it is clear that the effects of rising rates in previous years are still being felt, and it will take time for the full benefits of the current rate environment to reach all segments of the housing market.

Conclusion

The FHFA report confirms that while the housing market is showing some signs of recovery, particularly through refinancing, many homeowners still face challenges. The increase in forbearance and refinancing activity highlights the complex dynamics of the housing market as it adjusts to lower mortgage rates. For those looking to buy or refinance, the current market offers opportunities, but potential homebuyers should be prepared for regional variations in home prices and competition

Call-to-Action:

If you’re considering refinancing or need mortgage assistance, now could be a great time to explore your options as rates remain attractive. Be sure to shop around and consult multiple lenders to find the best deal. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses