Mortgage rates have experienced significant swings over the past several years, creating uncertainty for homebuyers, homeowners, and real estate investors. Inflation, Federal Reserve policy, global events, and economic growth have all contributed to a market that has been difficult to predict.

Many people are now asking the same question: Where are mortgage rates headed over the next five years?

While no forecast can guarantee future results, economists and market analysts generally expect mortgage rates to gradually move lower as inflation moderates and financial markets stabilize. However, most experts do not expect a return to the exceptionally low rates seen during the pandemic.

Here’s a closer look at what could shape mortgage rates through 2030.

Why Treasury Yields Matter

One of the best indicators of future mortgage rates is the yield on the 10-year U.S. Treasury note.

Although mortgage rates are not directly tied to Treasury yields, they often move in the same direction. Mortgage lenders use Treasury securities as a benchmark because they reflect long-term borrowing costs and investor expectations about the economy.

Mortgage rates are usually higher than Treasury yields because lenders account for additional risks, including borrower defaults, prepayments, and market uncertainty.

The difference between mortgage rates and Treasury yields is known as the spread.

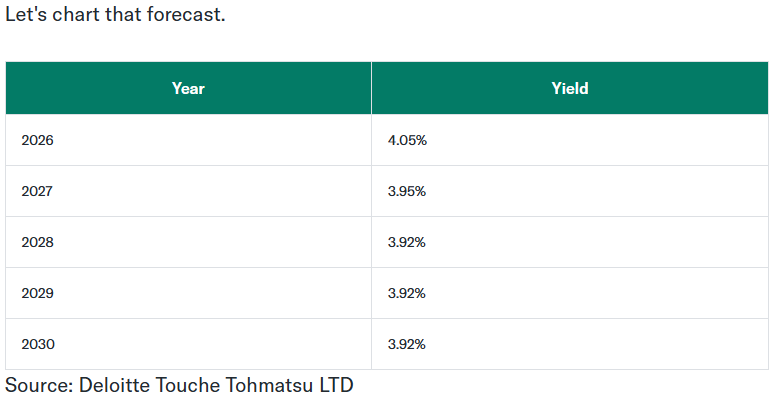

Treasury Yield Forecasts

Several economic forecasts suggest that Treasury yields could gradually stabilize over the next few years.

Some economists expect the Federal Reserve to keep interest rates relatively high until inflation moves closer to its long-term target. As inflation slows, long-term Treasury yields could ease modestly.

A general outlook suggests the 10-year Treasury yield may remain near 4% over the next several years before settling into a more stable range.

While forecasts vary, most projections point to moderate movements rather than dramatic shifts.

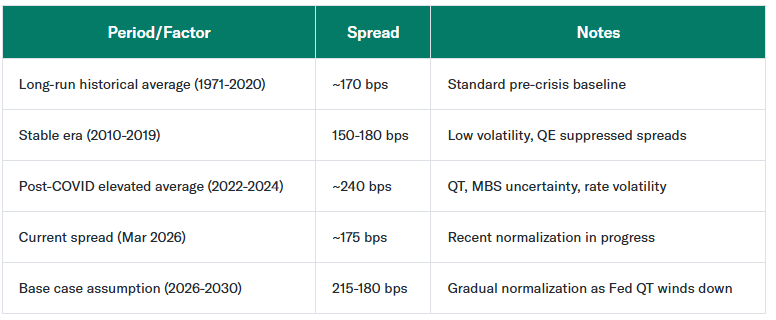

Understanding the Mortgage Rate Spread

The spread between the 10-year Treasury and 30-year mortgage rates has changed significantly over time.

Historically, the average spread was often between 1.5% and 1.8%.

During periods of economic uncertainty and high market volatility, the spread widened as investors demanded greater compensation for risk.

In recent years, factors such as Federal Reserve balance sheet reductions, inflation concerns, and uncertainty in mortgage-backed securities markets pushed spreads above historical averages.

Many analysts expect these spreads to gradually normalize over the next several years, which could help mortgage rates decline even if Treasury yields remain relatively stable.

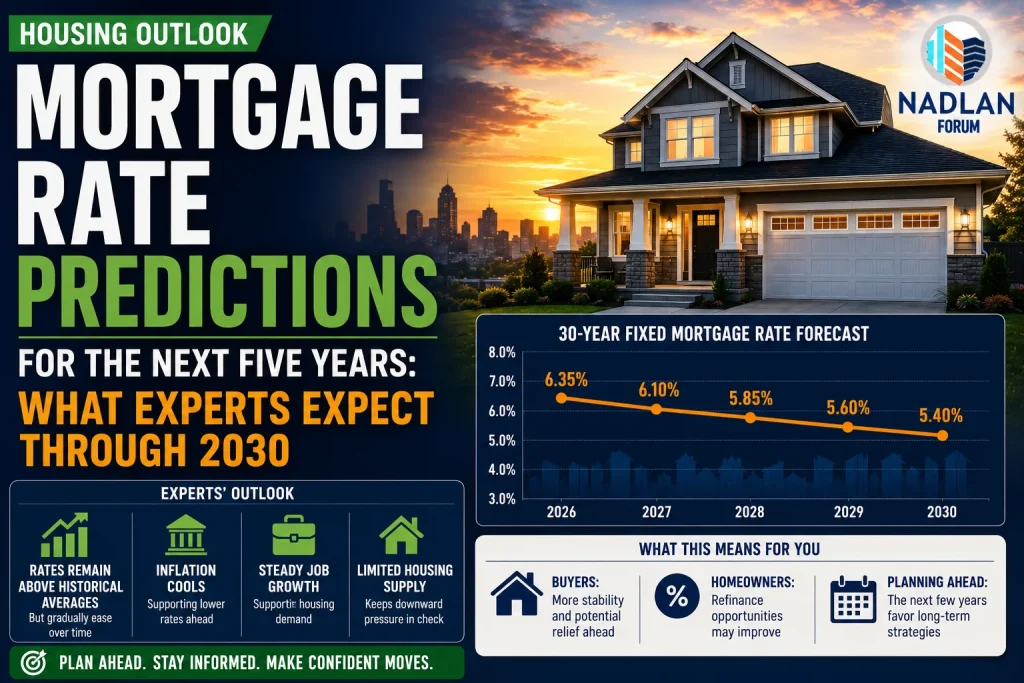

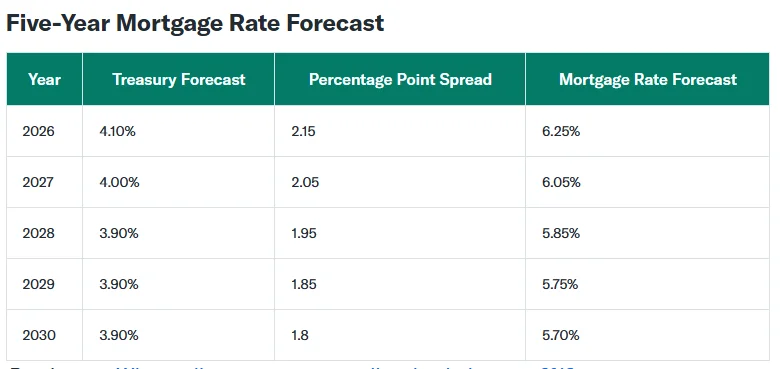

Five-Year Mortgage Rate Forecast

Using current economic expectations and assumptions about Treasury yields and mortgage spreads, a reasonable base-case forecast suggests mortgage rates could slowly improve over time.

Estimated average 30-year fixed mortgage rates:

2026: approximately 6.25%

2027: approximately 6.05%

2028: approximately 5.85%

2029: approximately 5.75%

2030: approximately 5.70%

These estimates suggest a gradual decline rather than a sharp drop.

Borrowers hoping for rates below 4% may have to wait much longer, unless unexpected economic events significantly change market conditions.

A Positive Scenario for Mortgage Rates

The most optimistic outlook assumes that inflation continues falling while the economy avoids a major recession.

Under this scenario:

- Inflation returns close to the Federal Reserve’s target.

- Interest rates gradually decline.

- Treasury yields move lower.

- Mortgage-backed securities markets stabilize.

- Mortgage spreads return to historical averages.

In this environment, mortgage rates could approach 5% by the end of the decade.

Such an outcome would improve affordability and could encourage more home sales and refinancing activity.

A Higher Rate Scenario

There is also a less favorable possibility.

If inflation remains persistent and government borrowing continues to grow rapidly, long-term interest rates could stay elevated.

Additional risks include:

- Ongoing geopolitical tensions.

- Rising government deficits.

- Higher energy prices.

- Strong consumer spending.

- Unexpected inflation shocks.

Under this scenario, mortgage rates could remain above 6% for much of the next several years and temporarily move toward 7% before gradually easing.

Factors That Could Change the Forecast

Long-term predictions should always be viewed as estimates rather than guarantees.

Several factors could alter the outlook.

Federal Reserve Policy

Changes in interest rate policy can quickly affect financial markets and investor expectations.

Inflation

Lower inflation would likely support lower mortgage rates, while higher inflation could keep borrowing costs elevated.

Economic Growth

A slowing economy could reduce interest rates, while stronger growth could push them higher.

Recession Risk

Economic downturns often lead investors toward Treasury bonds, lowering yields and potentially reducing mortgage rates.

Global Events

Wars, financial crises, supply chain disruptions, and other unexpected events can rapidly change market conditions.

Will Mortgage Rates Ever Return to 3%?

Most economists believe a return to 3% mortgage rates is unlikely during the next five years.

The historically low rates seen during 2020 and 2021 resulted from extraordinary circumstances, including aggressive Federal Reserve intervention and emergency economic measures during the pandemic.

Without a similar economic shock, mortgage rates are expected to remain well above those levels.

What Could Mortgage Rates Look Like in 2027?

Current long-term forecasts suggest that average 30-year fixed mortgage rates could move closer to 6% during 2027.

Actual rates will depend on inflation trends, Federal Reserve decisions, and broader economic conditions.

Small monthly fluctuations should be expected as financial markets react to new economic data.

Should Buyers Wait for Lower Rates?

Trying to perfectly time mortgage rates can be difficult.

For many buyers, waiting for significantly lower rates may not produce the expected savings, especially if home prices continue rising or housing inventory remains limited.

Some buyers choose to purchase when they find a home that fits their budget and refinance later if rates improve.

This approach allows homeowners to begin building equity rather than waiting for uncertain market conditions.

Fixed-Rate or Adjustable-Rate Mortgage?

For borrowers considering adjustable-rate mortgages, the decision should depend largely on personal circumstances.

A shorter fixed period may work well for buyers planning to move within a few years.

Borrowers intending to stay in their homes for the long term may prefer the stability of a traditional fixed-rate mortgage, especially during periods of economic uncertainty.

The best option depends on financial goals, expected ownership length, and comfort with changing interest rates.

What This Means for the Housing Market

Mortgage rates are expected to remain relatively high compared with the ultra-low levels of the early pandemic years, but most forecasts suggest gradual improvement through the end of the decade.

A steady decline toward the mid-5% range could help improve affordability, increase home sales, and encourage more refinancing activity.

At the same time, buyers and homeowners should remember that mortgage rates are only one part of the housing equation. Home prices, income growth, local market conditions, and personal financial readiness are equally important when making real estate decisions.

Bottom Line

Most expert forecasts suggest mortgage rates could gradually decline over the next five years, though dramatic drops appear unlikely. Current estimates point to average 30-year mortgage rates moving from roughly 6.25% in 2026 to around 5.70% by 2030.

While inflation, Federal Reserve policy, and global economic conditions will continue influencing the market, borrowers should avoid making decisions based solely on long-term forecasts. Buying or refinancing should ultimately depend on personal finances, housing needs, and long-term goals rather than trying to predict exactly where mortgage rates will go next. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.