Mortgage and Refinance Rates Today June 12, 2026: Why Home Loan Costs Are Climbing Again

The mortgage market moved higher this week as fresh economic reports suggested that inflation remains a challenge and the U.S. economy is still showing resilience. Strong job growth and rising consumer prices have changed expectations for Federal Reserve policy, pushing Treasury yields and mortgage rates upward.

While higher borrowing costs continue to create affordability concerns, the housing market has remained surprisingly active. Buyers and sellers are still entering the market, although many are adjusting their expectations as mortgage rates stay near recent highs.

Mortgage Rates Move Higher

The average 30-year fixed mortgage increased this week, reflecting growing concerns that interest rates could remain elevated for a longer period.

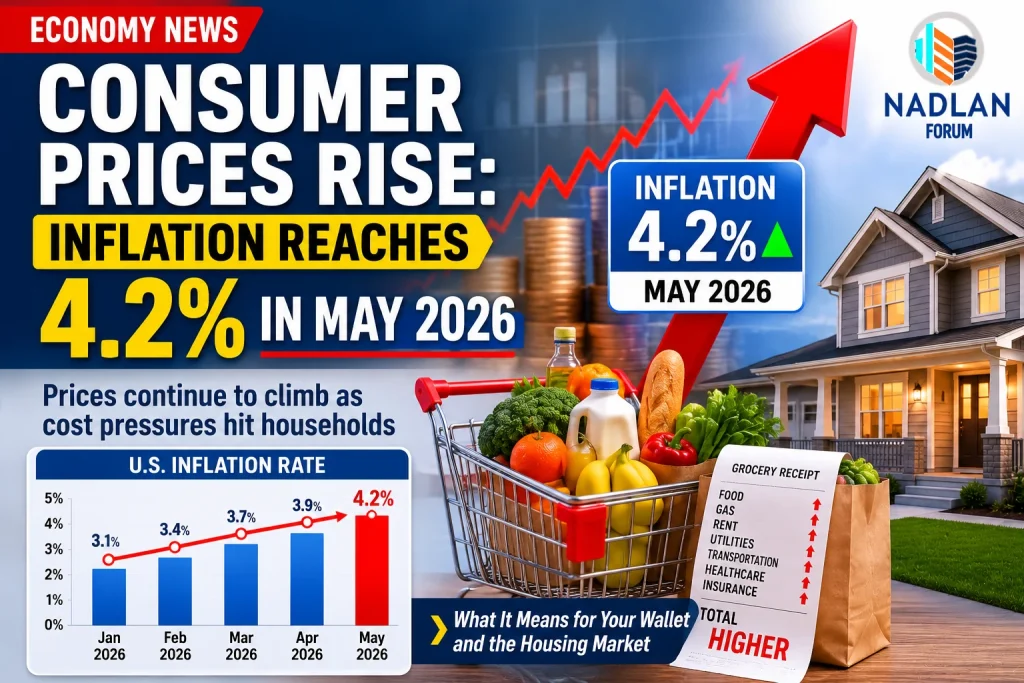

Recent economic data played a major role in the increase.

The U.S. economy added around 172,000 jobs during May, exceeding many forecasts and showing that the labor market remains relatively healthy. At the same time, inflation accelerated, with consumer prices rising 4.2% compared with a year ago. Higher energy prices have been one of the biggest factors contributing to inflation pressures.

These developments have reduced hopes for interest rate cuts and increased expectations that the Federal Reserve could tighten monetary policy again if inflation remains stubborn.

Although the Fed does not directly set mortgage rates, its policies heavily influence bond markets and investor expectations, which in turn affect home loan costs.

Current Mortgage Rates

According to the latest market data, national average mortgage rates include:

Purchase Loans

30-year fixed: 6.40%

20-year fixed: 6.34%

15-year fixed: 5.86%

5/1 adjustable-rate mortgage: 6.51%

7/1 adjustable-rate mortgage: 6.46%

30-year VA: 5.89%

15-year VA: 5.54%

5/1 VA: 5.70%

Mortgage rates can vary depending on location, lender, credit score, down payment, and overall financial profile.

Current Refinance Rates

Homeowners considering refinancing are seeing similar borrowing costs.

Current national average refinance rates are:

30-year fixed: 6.35%

20-year fixed: 6.35%

15-year fixed: 5.82%

5/1 ARM: 6.34%

7/1 ARM: 6.46%

30-year VA: 5.87%

15-year VA: 5.46%

5/1 VA: 5.77%

Unlike in some market cycles, refinance rates are currently very close to purchase mortgage rates, with some products even offering slightly lower averages.

Why Mortgage Rates Are Rising

Several factors are working together to keep mortgage rates elevated.

Strong Job Market

A healthy labor market supports consumer spending and economic growth. Strong employment numbers reduce the urgency for the Federal Reserve to lower interest rates.

Higher Inflation

Inflation remains above the Fed’s long-term target. Rising prices for energy and other goods continue to put pressure on policymakers to maintain tighter financial conditions.

Treasury Yields

Mortgage rates closely follow movements in the 10-year Treasury yield. When investors expect higher inflation or future rate hikes, Treasury yields often increase, pulling mortgage rates higher as well.

Federal Reserve Expectations

Financial markets are now pricing in a greater possibility that the Fed could raise benchmark rates again before the end of the year if inflation does not improve.

Housing Market Continues to Show Activity

Despite higher financing costs, the housing market has not stalled.

Home sales and buyer activity improved during May, suggesting that many households are adapting to the current interest rate environment. Limited housing inventory in many markets and steady job growth continue to support demand.

Some buyers are also accepting today’s rates with plans to refinance later if borrowing costs decline in future years.

At the same time, sellers who locked in extremely low mortgage rates during 2020 and 2021 remain reluctant to move, limiting the supply of existing homes available for sale.

Fixed-Rate vs. Adjustable-Rate Mortgages

Homebuyers generally choose between fixed-rate and adjustable-rate loans.

A fixed-rate mortgage keeps the same interest rate throughout the life of the loan. Monthly principal and interest payments remain predictable, making budgeting easier.

An adjustable-rate mortgage, or ARM, starts with a fixed introductory rate before adjusting periodically based on market conditions. These loans may offer lower initial payments but carry the risk of future rate increases.

The right choice depends on a borrower’s financial goals, risk tolerance, and expected length of homeownership.

30-Year vs. 15-Year Mortgages

The two most common mortgage terms each have advantages.

A 30-year mortgage provides lower monthly payments because the loan is spread over a longer period. However, borrowers pay more total interest over time.

A 15-year mortgage usually comes with a lower interest rate and significantly reduces total interest costs. The trade-off is a higher monthly payment.

Borrowers should compare both options carefully based on income, long-term plans, and overall financial flexibility.

What Determines Your Mortgage Rate?

Some factors affecting mortgage rates are outside a borrower’s control, while others can be improved.

Factors borrowers can influence include:

- Credit score.

- Debt-to-income ratio.

- Down payment amount.

- Loan type.

- Shopping among multiple lenders.

- Property type and occupancy.

Economic conditions, inflation, Federal Reserve policy, and bond market movements are external factors that affect mortgage pricing for everyone.

Improving credit and reducing debt before applying for a loan can help secure better financing terms.

Should Homeowners Refinance?

Whether refinancing makes sense depends on individual circumstances.

In the past, many experts suggested waiting for at least a 2% reduction in interest rates before refinancing. Others believe a 1% improvement can be worthwhile depending on closing costs and how long the homeowner plans to keep the property.

Refinancing may also help borrowers switch from an adjustable-rate mortgage to a fixed-rate loan, shorten their loan term, or tap home equity for major expenses.

Calculating the break-even point between refinancing costs and monthly savings remains one of the most important steps before making a decision.

Outlook for Mortgage Rates

The path for mortgage rates during the remainder of 2026 will largely depend on inflation, employment data, and Federal Reserve decisions.

If inflation slows and economic growth moderates, rates could gradually ease. However, continued strength in the labor market and persistent price pressures may keep borrowing costs elevated.

For buyers and homeowners, waiting for dramatically lower mortgage rates may not be the best strategy. Housing experts increasingly suggest focusing on affordability, personal finances, and long-term housing needs rather than trying to perfectly time the market.

Bottom Line

Mortgage rates moved higher after stronger economic data reinforced expectations that interest rates could remain elevated for longer. Inflation and job growth continue to influence financial markets, keeping borrowing costs under pressure.

Even with mortgage rates hovering around 6.5%, housing activity remains steady as buyers adapt to the current environment. Whether purchasing a home or considering a refinance, comparing lenders, improving financial health, and understanding available loan options can help borrowers make informed decisions in a changing market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses