Mortgage rates moved lower during the final week of June, giving homebuyers and homeowners slightly better borrowing conditions as the month came to a close. After several weeks of modest fluctuations, the latest market data shows that most major mortgage products declined compared with the beginning of the week, offering some relief for borrowers still waiting for financing costs to improve.

The average 30-year fixed mortgage rate fell to 6.17%, marking one of the lowest average levels seen in recent weeks. Adjustable-rate mortgages also posted noticeable declines, while refinance rates remained relatively stable across most loan programs.

Although rates remain higher than many borrowers would like, the recent downward trend is an encouraging sign as financial markets continue reacting to inflation data, Treasury yields, and expectations for future Federal Reserve policy.

Current Purchase Mortgage Rates

According to the latest national averages, today’s mortgage rates for home purchases are:

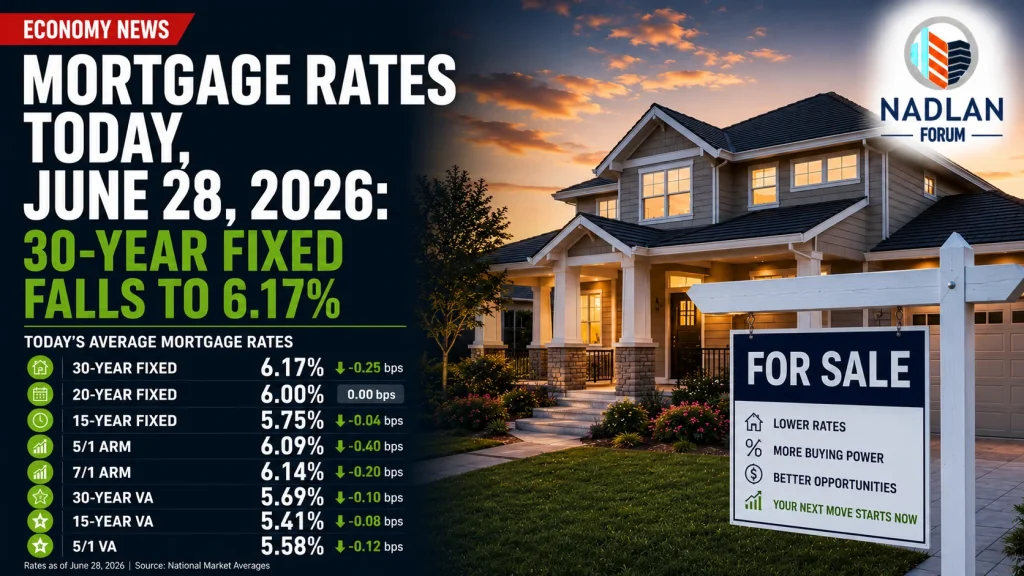

- 30-year fixed: 6.17%

- 20-year fixed: 6.00%

- 15-year fixed: 5.75%

- 5/1 Adjustable-Rate Mortgage (ARM): 6.09%

- 7/1 ARM: 6.14%

- 30-year VA: 5.69%

- 15-year VA: 5.41%

- 5/1 VA: 5.58%

Compared with Monday, June 22:

- The 30-year fixed mortgage declined by 25 basis points.

- The 15-year fixed mortgage fell by 4 basis points.

- The 5/1 ARM dropped by 40 basis points, representing the largest weekly improvement among the most common loan products.

These changes provide buyers with modest savings on monthly mortgage payments, particularly for larger loan amounts.

Current Mortgage Refinance Rates

Homeowners considering refinancing also saw relatively stable rates.

Current refinance averages include:

- 30-year fixed: 6.26%

- 20-year fixed: 5.96%

- 15-year fixed: 5.73%

- 5/1 ARM: 6.18%

- 7/1 ARM: 6.18%

- 30-year VA: 5.61%

- 15-year VA: 5.34%

- 5/1 VA: 5.56%

While refinance rates often run slightly higher than purchase mortgage rates, current pricing remains competitive for homeowners looking to reduce monthly payments, shorten their loan term, or tap into home equity, depending on their existing mortgage.

Mortgage Rates Continue to Respond to Economic Data

Mortgage rates are influenced by several economic factors rather than Federal Reserve decisions alone.

Recent inflation reports, Treasury bond yields, labor market conditions, and investor expectations all continue shaping daily mortgage pricing.

Although inflation remains above the Federal Reserve’s long-term target, improving market confidence and slightly lower Treasury yields helped reduce mortgage rates during the past week.

Investors are now watching upcoming economic reports closely to determine whether inflation continues easing during the second half of 2026.

If inflation continues to moderate, mortgage rates could remain stable or gradually decline over the coming months.

30-Year vs. 15-Year Mortgage

Choosing between a 30-year and 15-year mortgage depends largely on a buyer’s financial priorities.

30-Year Fixed Mortgage

The 30-year fixed mortgage remains the most popular loan option because it offers:

- Lower monthly payments

- Predictable fixed interest rates

- Greater financial flexibility

- Easier budgeting over the long term

Although borrowers pay more total interest over 30 years, the lower monthly payment often improves affordability.

15-Year Fixed Mortgage

A 15-year mortgage provides several long-term financial advantages.

Benefits include:

- Lower interest rates

- Faster loan repayment

- Significant interest savings

- Quicker equity growth

The primary drawback is a considerably higher monthly payment, which requires stronger household cash flow.

For borrowers who can comfortably afford the larger payment, a 15-year loan can save tens of thousands of dollars in interest over the life of the mortgage.

Fixed-Rate vs. Adjustable-Rate Mortgages

Borrowers should also carefully compare fixed-rate and adjustable-rate mortgage options.

Fixed-Rate Mortgage

A fixed-rate mortgage locks in the same interest rate for the full loan term, protecting borrowers from future rate increases.

This option is generally preferred by homeowners planning to remain in the property for many years.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a fixed introductory rate before adjusting periodically based on market conditions.

For example:

- A 5/1 ARM remains fixed for five years before annual adjustments begin.

- A 7/1 ARM provides seven years of fixed payments before yearly adjustments.

Historically, ARMs often offered substantially lower starting rates than fixed mortgages.

Today, however, the gap has narrowed considerably, making fixed-rate loans attractive for many borrowers seeking payment stability.

Tips for Getting the Best Mortgage Rate

While market rates are important, individual financial qualifications still play a major role in determining the rate offered by lenders.

Borrowers may qualify for better pricing by:

- Improving their credit score

- Saving for a larger down payment

- Reducing outstanding debt

- Lowering their debt-to-income ratio

- Comparing multiple lenders

- Exploring different loan programs

Obtaining several loan estimates within a short period allows buyers to compare rates, lender fees, and Annual Percentage Rates (APR) without significantly affecting their credit score.

Looking beyond the advertised interest rate and reviewing total borrowing costs can often result in meaningful long-term savings.

What This Means for Homebuyers

The decline in mortgage rates offers welcome news for buyers entering the housing market.

Although affordability challenges remain due to elevated home prices in many regions, lower financing costs can improve purchasing power and reduce monthly payments.

For example, even a quarter-point decline in mortgage rates can lower monthly payments and reduce total interest costs over the life of a loan.

Combined with rising housing inventory in many markets, improving mortgage rates may encourage more buyers to move forward with home purchases during the second half of 2026.

Mortgage Rate Outlook for the Rest of 2026

Most housing economists expect mortgage rates to remain within a relatively narrow range for the remainder of the year.

Forecasts generally place the average 30-year fixed mortgage between 6.3% and 6.5%, although additional improvements are possible if inflation continues slowing and financial markets gain confidence that the Federal Reserve can eventually ease monetary policy.

Future mortgage rate movements will continue depending on:

- Inflation reports

- Federal Reserve policy

- Treasury bond yields

- Employment data

- Consumer spending

- Global economic conditions

Because these factors change frequently, mortgage rates are likely to remain responsive to new economic data throughout the rest of 2026.

Final Thoughts

Mortgage rates ended the week on a positive note, with the average 30-year fixed mortgage falling to 6.17%, its lowest level of the week. The decline offers modest but meaningful savings for homebuyers and homeowners considering refinancing.

While borrowing costs remain above the historically low levels seen several years ago, the recent downward trend suggests financing conditions may gradually improve if inflation continues easing. Buyers should continue comparing loan offers from multiple lenders and monitor market conditions as they prepare for one of the biggest financial decisions of their lives. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.