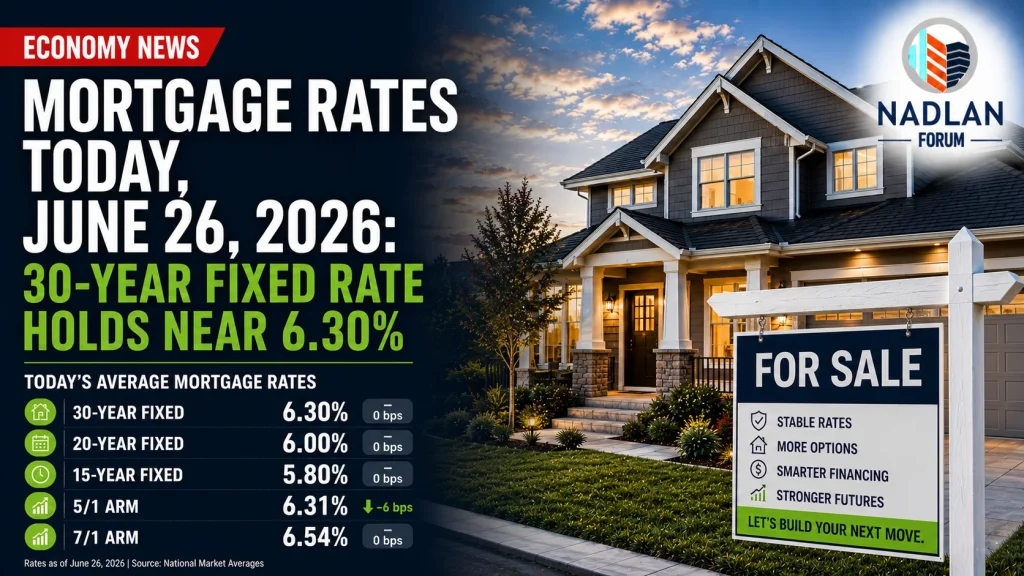

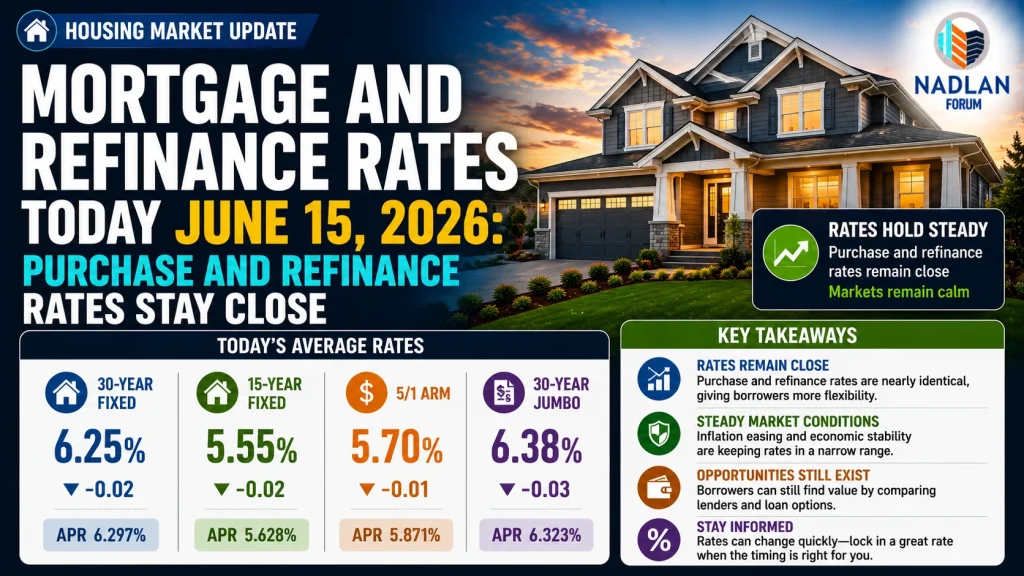

Mortgage Rates Today, June 26, 2026: 30-Year Fixed Rate Holds Near 6.30%

Mortgage interest rates showed very little movement on Friday, June 26, giving homebuyers and homeowners a relatively stable borrowing environment heading into the weekend. While rates continue to fluctuate from day to day, the latest changes were modest, suggesting that lenders remain cautious as financial markets evaluate inflation, Federal Reserve policy, and broader economic conditions.

The average 30-year fixed mortgage rate edged slightly lower, while most other loan products changed very little. For buyers waiting for a major drop in borrowing costs, today’s update indicates that mortgage rates continue to remain within the same general range seen throughout recent weeks.

Current Purchase Mortgage Rates

According to the latest national market averages, mortgage rates for home purchases on June 26, 2026, are:

- 30-year fixed: 6.30%

- 20-year fixed: 6.00%

- 15-year fixed: 5.80%

- 5/1 Adjustable-Rate Mortgage (ARM): 6.31%

- 7/1 ARM: 6.54%

- 30-year VA: 5.84%

- 15-year VA: 5.49%

- 5/1 VA: 5.79%

The 30-year fixed mortgage declined by three basis points compared with the previous day, while the 15-year fixed rate remained unchanged. Adjustable-rate mortgages also experienced only modest daily movement.

Although daily fluctuations are common, today’s changes were relatively small, reflecting a market that is waiting for additional economic data before establishing a clearer direction.

Current Mortgage Refinance Rates

Homeowners considering refinancing also saw relatively stable borrowing costs.

Average refinance rates currently stand at:

- 30-year fixed: 6.24%

- 20-year fixed: 6.07%

- 15-year fixed: 5.77%

- 5/1 ARM: 6.29%

- 7/1 ARM: 6.39%

- 30-year VA: 5.71%

- 15-year VA: 5.37%

- 5/1 VA: 5.68%

While refinance rates are often slightly higher than purchase mortgage rates, current market conditions have narrowed that difference for several loan products.

Whether refinancing makes financial sense depends on several factors, including the homeowner’s existing mortgage rate, remaining loan balance, closing costs, and long-term financial goals.

Why Mortgage Rates Are Holding Steady

Mortgage rates continue to respond to several competing economic forces.

Recent inflation reports have shown that price pressures remain elevated, causing investors to reconsider expectations for future Federal Reserve interest rate decisions. At the same time, lower oil prices and easing geopolitical concerns have helped reduce some inflation expectations.

Because these factors offset one another, mortgage markets have remained relatively stable.

In addition, Treasury yields—which heavily influence mortgage pricing—have traded within a fairly narrow range over the past several sessions, limiting significant changes in lending rates.

Fixed-Rate vs. Adjustable-Rate Mortgages

Borrowers continue to choose between fixed-rate and adjustable-rate mortgage options based on their financial plans and expected time in the home.

Fixed-Rate Mortgages

A fixed-rate mortgage locks in the same interest rate for the entire loan term.

Advantages include:

- Predictable monthly payments

- Protection from future interest rate increases

- Easier long-term budgeting

- Greater financial certainty

The 30-year fixed mortgage remains the most popular option because it offers lower monthly payments compared with shorter loan terms.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages begin with a fixed introductory rate before adjusting periodically according to market conditions.

For example:

- A 5/1 ARM keeps the initial rate fixed for five years before adjusting annually.

- A 7/1 ARM provides a fixed rate for seven years before annual adjustments begin.

Historically, ARMs have attracted borrowers by offering lower starting rates than fixed mortgages.

However, current market conditions have narrowed that advantage considerably. In some cases, adjustable-rate loans are now priced similarly to—or even slightly above—30-year fixed mortgages.

For borrowers planning to remain in a home for many years, carefully comparing long-term costs has become increasingly important.

Choosing Between a 15-Year and 30-Year Mortgage

The decision between a 15-year and 30-year mortgage depends largely on monthly budget and long-term financial goals.

30-Year Fixed Mortgage

Many buyers choose a 30-year loan because it provides:

- Lower monthly payments

- Greater financial flexibility

- Improved cash flow

- Easier qualification for larger loan amounts

The trade-off is paying more total interest over the life of the loan.

15-Year Fixed Mortgage

A 15-year mortgage offers several benefits:

- Lower interest rates

- Faster loan payoff

- Significant long-term interest savings

- Faster home equity growth

However, monthly payments are considerably higher, requiring stronger household income and budgeting discipline.

What Homebuyers Should Consider

Even small differences in mortgage rates can have a meaningful impact on monthly housing costs.

For example, a change of just 0.25 percentage points on a typical mortgage can increase or decrease monthly payments by hundreds of dollars over the life of the loan.

Before locking a mortgage rate, buyers should compare:

- Interest rates

- Loan fees

- Closing costs

- Discount points

- Annual Percentage Rate (APR)

- Lender incentives

- Loan program options

Shopping with multiple lenders often results in more competitive financing terms.

Mortgage Rate Outlook for 2026

Current industry forecasts suggest mortgage rates may remain relatively stable through the remainder of 2026.

Several housing economists expect average 30-year fixed mortgage rates to remain in the 6.4% to 6.5% range, while some forecasts anticipate rates gradually easing toward 6.3% to 6.4% if inflation continues slowing.

Future mortgage rate movements will largely depend on:

- Inflation data

- Federal Reserve policy decisions

- Labor market conditions

- Treasury bond yields

- Economic growth

- Global geopolitical developments

If inflation continues moderating during the second half of the year, mortgage rates could gradually move lower. However, stronger-than-expected inflation could keep borrowing costs elevated for longer.

Final Thoughts

Mortgage rates remained largely unchanged on June 26, 2026, providing buyers with a relatively stable financing environment as the week came to a close. The average 30-year fixed mortgage rate held near 6.30%, while refinance rates also showed only modest movement.

Although borrowing costs remain higher than many buyers would prefer, today’s market offers greater stability than the rapid fluctuations seen in recent years. As investors continue monitoring inflation and Federal Reserve policy, mortgage rates are expected to remain sensitive to new economic data throughout the remainder of 2026.

For buyers and homeowners considering a purchase or refinance, comparing multiple lenders and evaluating different loan options remains one of the most effective ways to secure competitive financing. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses