Mortgage Rates Fall to Lowest Level in Over a Year, Refinancing Surges 111%

Mortgage rates continued their steady decline for the fourth week in a row, dropping to their lowest level since September 2024 and breathing new life into both home purchase and refinance activity. According to the Mortgage Bankers Association (MBA), total mortgage application volume climbed 7.1% last week compared to the previous week, as homeowners and prospective buyers rushed to take advantage of lower borrowing costs.

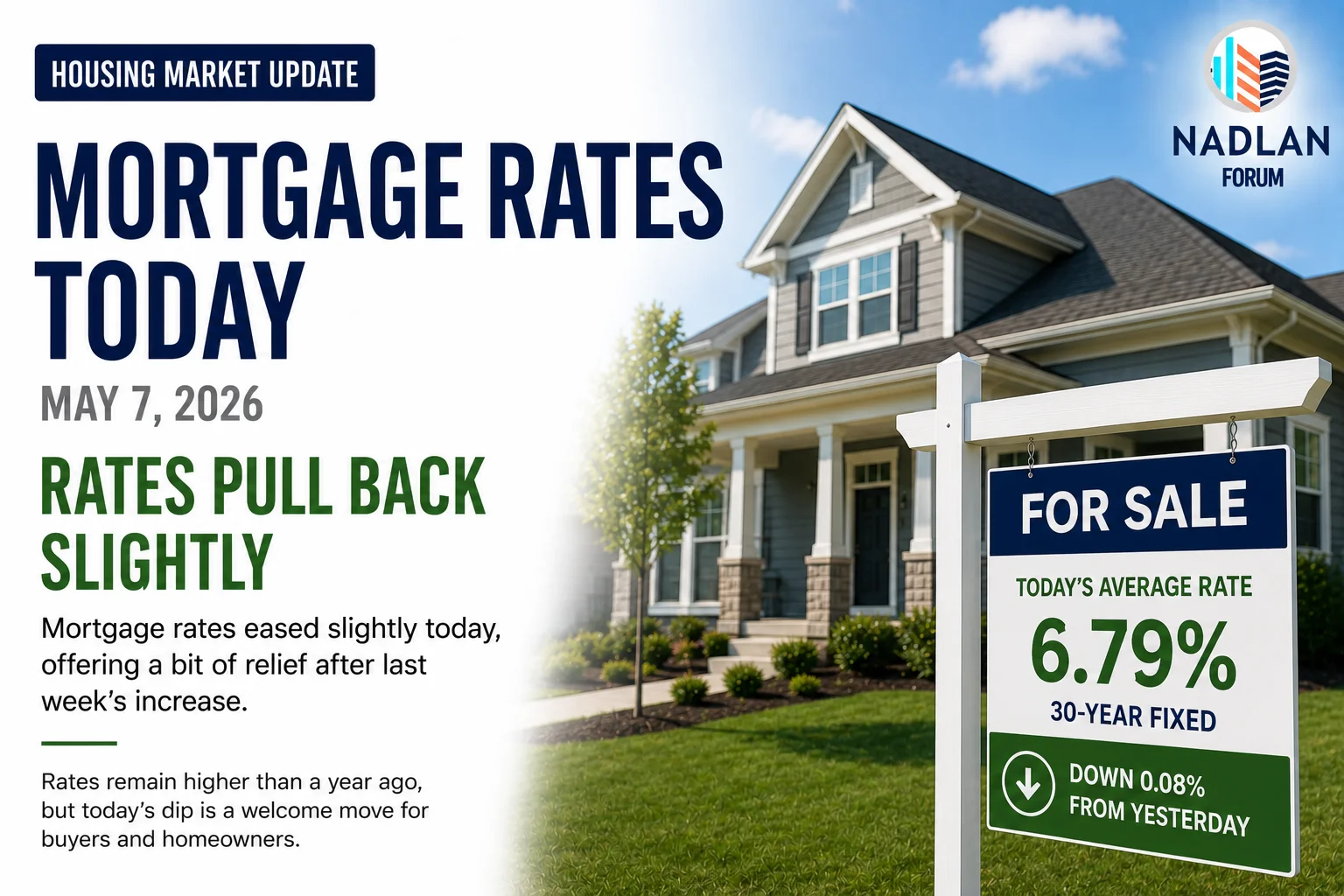

The average contract interest rate for a 30-year fixed-rate mortgage with conforming loan balances of $806,500 or less fell to 6.30% from 6.37%, while average points decreased slightly to 0.58 from 0.59 for loans requiring a 20% down payment. That’s a meaningful improvement, marking the lowest rate in more than a year and signaling a potential turning point after months of stubbornly high borrowing costs.

“This recent decline in rates spurred the second consecutive week of increased refinance activity, driven mainly by conventional refinance applications,” said Joel Kan, MBA’s vice president and deputy chief economist. “We also saw the adjustable-rate mortgage (ARM) share of applications dip below 10%, as more borrowers opted for fixed-rate loans to lock in favorable terms.”

Refinancing Boom Gains Steam

Refinance activity, which is typically the first to react when rates fall, jumped 9% week over week and surged 111% higher than the same week a year ago. This marks one of the strongest annual increases in refinancing since the pandemic-era lows, when rates hovered near 3%.

The average loan size for a refinance remained elevated at $393,900, indicating that higher-income borrowers or those with larger loan balances are seeing the biggest financial benefit from the recent dip in rates. For example, a homeowner refinancing a $400,000 loan from 7% to 6.3% could save roughly $200–$250 per month, or more than $70,000 in interest over the life of the loan.

“Borrowers with larger balances stand to gain the most, but even moderate declines in rates can make a meaningful difference in monthly payments,” Kan noted. “For many homeowners who purchased or refinanced in the past two years, this could finally be the window to restructure their debt at more manageable costs.”

Home Purchase Activity Rebounds

On the purchase side, mortgage applications to buy a home increased 5% for the week and were 20% higher than a year ago. While that signals some renewed buyer interest, affordability remains a major challenge across most U.S. markets, with home prices still near record highs.

“Purchase applications increased across most loan types, though USDA applications fell sharply down more than 26% likely due to the ongoing government shutdown,” Kan explained.

Even with the improvement, buyers continue to navigate a tough mix of high prices, limited inventory, and economic uncertainty. Many are waiting for further rate cuts or price corrections before jumping back into the market in full force.

What’s Driving the Drop in Rates

The recent decline in mortgage rates reflects broader movement in the bond market, which heavily influences mortgage pricing. Investors have grown more cautious amid limited access to government data due to the shutdown, relying instead on market signals and speculation about the Federal Reserve’s next policy steps.

According to a separate daily survey from Mortgage News Daily (MND), rates dropped even further to start this week, as traders bet that slowing economic momentum will encourage the Fed to ease policy more aggressively in the coming months.

However, experts caution that a Fed rate cut does not directly translate into lower mortgage rates. Instead, mortgage rates move in response to expectations for long-term inflation and Treasury yields.

“We already know the Fed will be cutting rates,” wrote Matthew Graham, chief operating officer at MND. “But that rate cut itself doesn’t dictate what happens next for mortgage rates. The real driver will be the tone of the Fed’s press conference and any indications about future bond buying policies or inflation expectations.”

A Glimmer of Relief — With Caveats

For many Americans, the current rate environment represents the most affordable borrowing landscape in more than a year. Yet experts warn that volatility remains a risk. If inflation surprises on the upside or if economic data rebounds once government reporting resumes, rates could easily climb again.

Still, for now, the drop in rates is a welcome development for both homeowners and buyers hoping for relief after years of elevated costs. While affordability challenges remain steep, particularly in high-cost markets, even modest declines in borrowing costs are providing some breathing room and could help reenergize the sluggish housing market as 2025 winds down.

“This is a positive sign for the market,” said Kan. “If rates continue trending lower, we may finally see more sellers and buyers re-entering the market, creating a healthier balance heading into the new year.” For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses