Rising Mortgage Rates and Insurance Costs: Growing Risk for Homeowners

Rising Costs Are Putting Pressure on Homeowners

The housing market is facing pressure from multiple directions. Mortgage rates have recently increased, while insurance costs continue to climb. Together, these changes are making homeownership more expensive and creating new risks for homeowners.

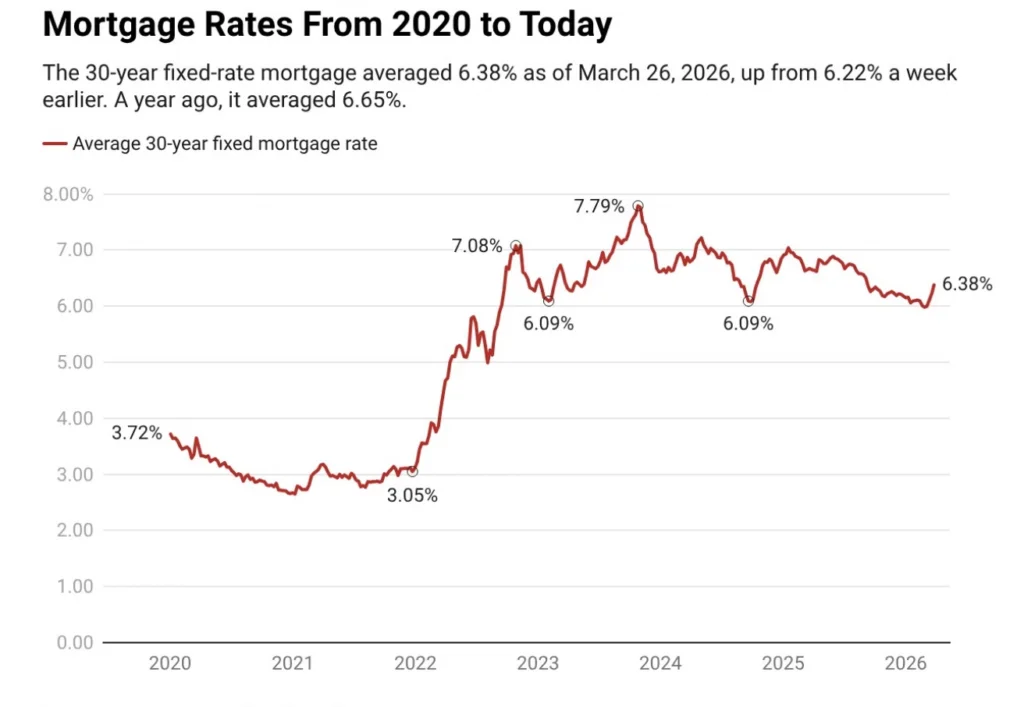

Data from Freddie Mac shows that mortgage rates saw a sharp increase in March, marking one of the fastest short-term rises in more than a year. Even though rates are still lower than last year, the sudden jump has affected affordability for many buyers.

At the same time, higher fuel prices and general inflation are reducing household budgets, making it harder for both buyers and existing homeowners to manage costs.

What Is Driving Underinsurance

One of the growing concerns in this environment is underinsurance. This happens when a homeowner’s insurance policy does not fully cover the cost to rebuild or repair their home.

Several factors are contributing to this issue:

- Rising construction and labor costs

- Higher prices for building materials

- Increased risk from natural disasters

- Limited availability of insurance in certain areas

Over time, these factors can cause insurance coverage limits to fall behind actual replacement costs.

Insurance Market Changes and Coverage Gaps

The insurance market itself is also changing. Some insurers are reducing coverage options or leaving areas that are considered high risk, such as regions prone to wildfires, floods, or storms.

As a result, homeowners may have fewer choices and may be forced to accept policies with lower coverage limits.

In some cases, homeowners choose reduced coverage simply to keep premiums affordable. While this lowers monthly costs, it increases financial risk if damage occurs.

Data Shows Growing Underinsurance Risk

Research highlights how widespread this issue has become. Studies show that a large share of homeowners do not have enough coverage to fully rebuild their homes after major damage.

Older insurance policies are especially at risk. If coverage limits were set years ago, they may not reflect today’s higher rebuilding costs.

Even policies with automatic adjustments for inflation may not keep up during periods of rapid price increases.

Impact on Homeowners and the Housing Market

Underinsured homeowners face serious financial consequences. If a major event occurs, they may need to cover a large portion of rebuilding costs out of pocket.

This risk is increasing at a time when homeowners are already dealing with:

- Higher mortgage payments

- Rising insurance premiums

- Increased living expenses

For buyers, these conditions may lead to hesitation in entering the market. For sellers, it may result in slower transactions and longer listing times.

Additional Coverage Gaps to Consider

Standard home insurance policies often do not cover all risks. For example:

- Flood damage usually requires separate insurance

- Earthquake coverage is often excluded

- Building code upgrades may have limited coverage

Because of these gaps, homeowners may still be underinsured even if they have a basic policy.

Adding extra coverage can help, but it also increases costs, which many households are already struggling to manage.

Balancing Cost and Protection

Homeowners are increasingly facing a difficult choice between affordability and adequate protection.

Some choose to lower their coverage to reduce premiums, while others keep full coverage but adjust other parts of their budget.

Experts recommend regularly reviewing insurance policies and updating coverage limits to reflect current rebuilding costs.

Housing Market Signals Remain Mixed

Despite these challenges, there are some positive signs in the housing market. Data from Realtor.com shows that asking prices have slightly decreased compared to last year.

At the same time:

- Housing inventory is increasing

- Homes are staying on the market longer

- Buyers are taking more time to make decisions

These trends suggest a shift toward a more balanced market, even as affordability remains a concern.

Broader Trends Affecting Renters and Buyers

Affordability challenges are also shaping renter behavior. Different groups are responding in different ways:

- Long-term renters are staying in place to keep lower rents

- Families are seeking affordable regions with more space

- Younger households are moving to mid-sized cities with lower costs

These patterns highlight how both renters and buyers are adjusting to higher housing expenses.

Final Thoughts

The combination of rising mortgage rates and increasing insurance costs is creating new risks in the housing market. Underinsured homeowners are particularly vulnerable, as coverage gaps can lead to significant financial losses.

As costs continue to rise, reviewing insurance policies and planning ahead will be essential. For both buyers and current homeowners, understanding these risks is key to making informed decisions in today’s housing environment. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses