2025 Housing Affordability in Review: What Improved, What Didn’t, and What Comes Next

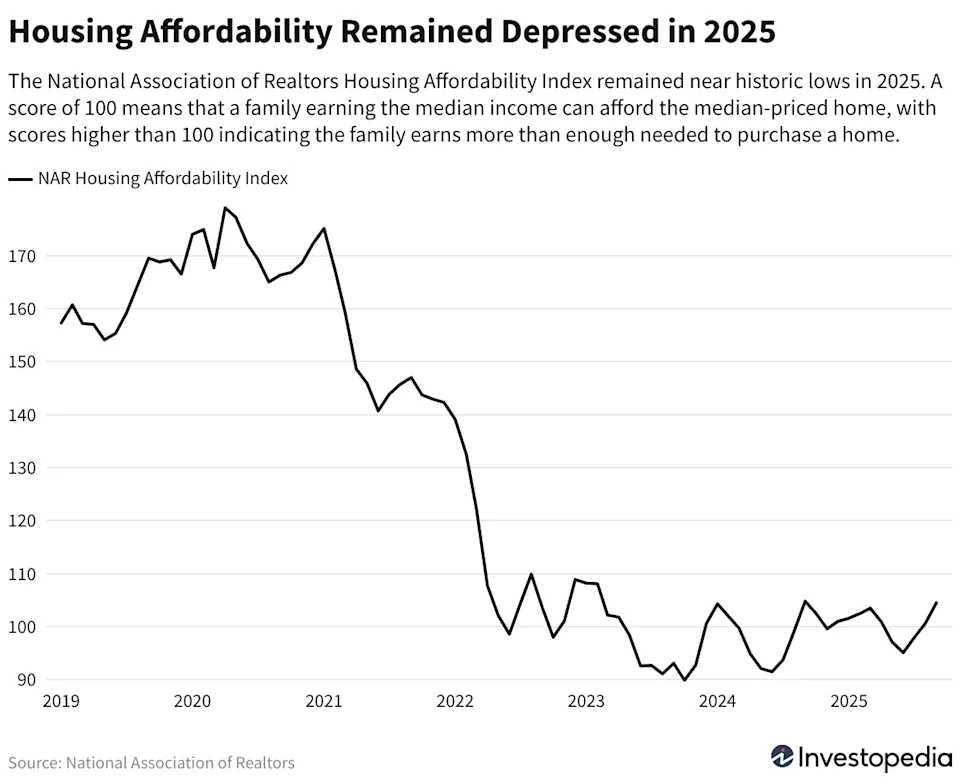

Housing affordability remained one of the biggest challenges of 2025. While there were small signs of progress, high mortgage rates and elevated home prices continued to put pressure on buyers across much of the country.

For many households, especially first-time buyers, the year felt like more waiting than winning. Experts say some relief may come in 2026, but it is likely to arrive slowly and unevenly, depending on where you live and how much you earn.

Why Housing Affordability Matters

Housing costs affect more than just buyers and sellers. When homes are hard to afford, families spend more of their income on housing and less elsewhere. That can slow consumer spending, limit wealth-building for younger households, and weigh on economic growth.

According to a market outlook from Compass, affordability is no longer falling fast, but it is not rebounding quickly either.

After several years of decline, affordability is now expected to improve slowly through a mix of flat home prices, rising incomes, and gradual drops in mortgage rates rather than a sharp price correction.

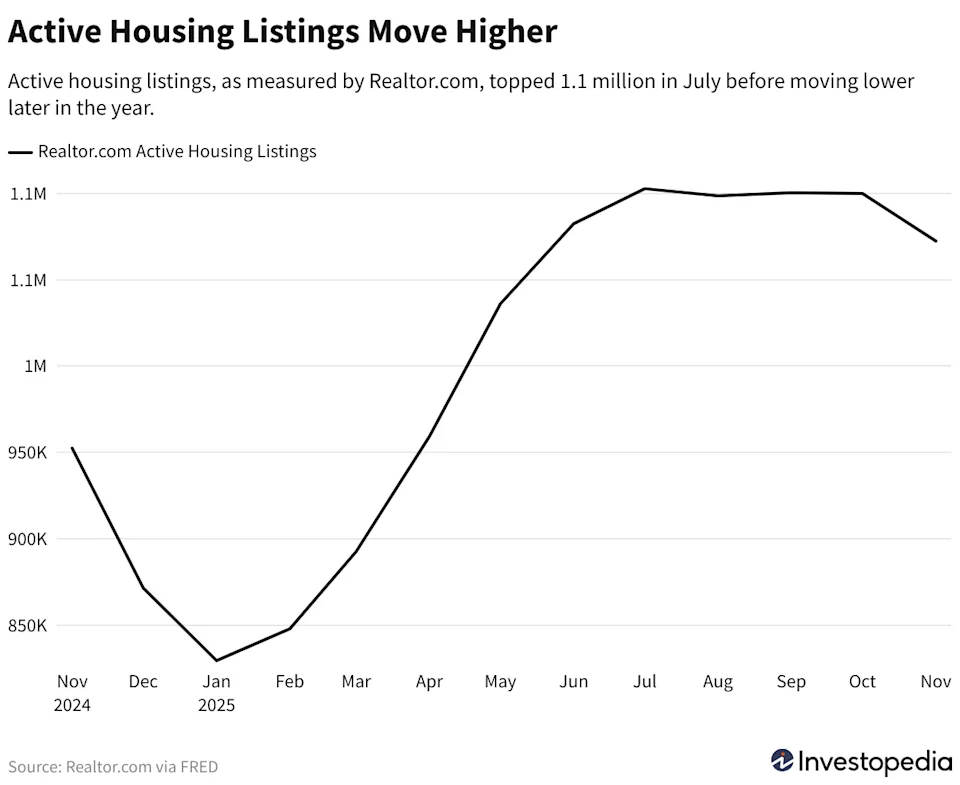

More Homes Hit the Market, but Not Enough

Home sales stayed weak through most of 2025, but inventory did rise.

Early in the year, the number of homes for sale jumped about 25% compared with 2024 as buyers backed away from mortgage rates near 7%. Later in the year, as rates eased and some sellers pulled listings, inventory growth slowed to about 11% year over year by October, based on data from the National Association of Realtors.

Looking ahead, Compass expects active listings to grow another 10% to 15% in 2026. Single-family listings could top 1 million during the summer for the first time since 2017.

Even so, this increase still falls short. Analysts at Goldman Sachs estimate the U.S. needs 3 million to 4 million additional homes to bring supply and demand into balance.

Mortgage Rates Fell, but Still Hurt Affordability

Mortgage rates moved lower in 2025, but they remained above 6% for most of the year. That kept many buyers on the sidelines.

Economists expect rates to drift lower again in 2026, but most forecasts keep them in the low-6% range rather than returning to the ultra-low levels seen earlier in the decade.

Research from Oxford Economics shows that mortgage rates have had a bigger impact on affordability than home prices. Higher rates not only raise monthly payments, they also shift more of each payment toward interest instead of building equity, especially in the early years of a loan.

Home Prices Stayed High

Even though price growth slowed, home prices still reached new highs in 2025.

Data from the S&P Dow Jones Indices Case-Shiller index shows national home prices peaked in June. By the third quarter, prices were rising in about 77% of U.S. markets, and around 4% of markets saw double-digit gains.

Oxford Economics estimates that a household needed to earn about $110,000 a year in late 2025 to afford a typical single-family home once taxes and insurance are included. That is slightly better than earlier in the year, but still nearly double the income needed in 2020.

Many sellers chose to wait rather than cut prices, which helped keep values high even as sales slowed. According to Redfin, today’s homeowners often have strong credit, low mortgage rates, and significant equity, reducing pressure to sell.

Affordability Looked Very Different by Region

Housing affordability did not move the same way everywhere.

Coastal California and parts of the Northeast remained among the least affordable areas in the country. Some Sun Belt and Midwest markets offered better value, but even those regions began to feel pressure in 2025.

Places like Port St. Lucie and Ocala in Florida, Kansas City, Missouri, and smaller Midwest metros such as Green Bay and Fond du Lac saw some of the sharpest declines in affordability as prices rose faster than incomes.

Will 2026 Be Better?

There is cautious optimism for 2026.

Economists expect mortgage rates to ease slightly and home price growth to slow further. If wages continue to rise faster than home prices, affordability could improve for some buyers.

Still, experts agree that without a larger increase in housing supply, affordability problems will not disappear. Many younger buyers and families may continue to delay homeownership or look for alternative living arrangements as costs remain high.

Bottom line: 2025 brought small steps toward better housing affordability, but not enough to solve the problem. In 2026, progress is expected to continue, but patience will still be required for many would-be buyers. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses