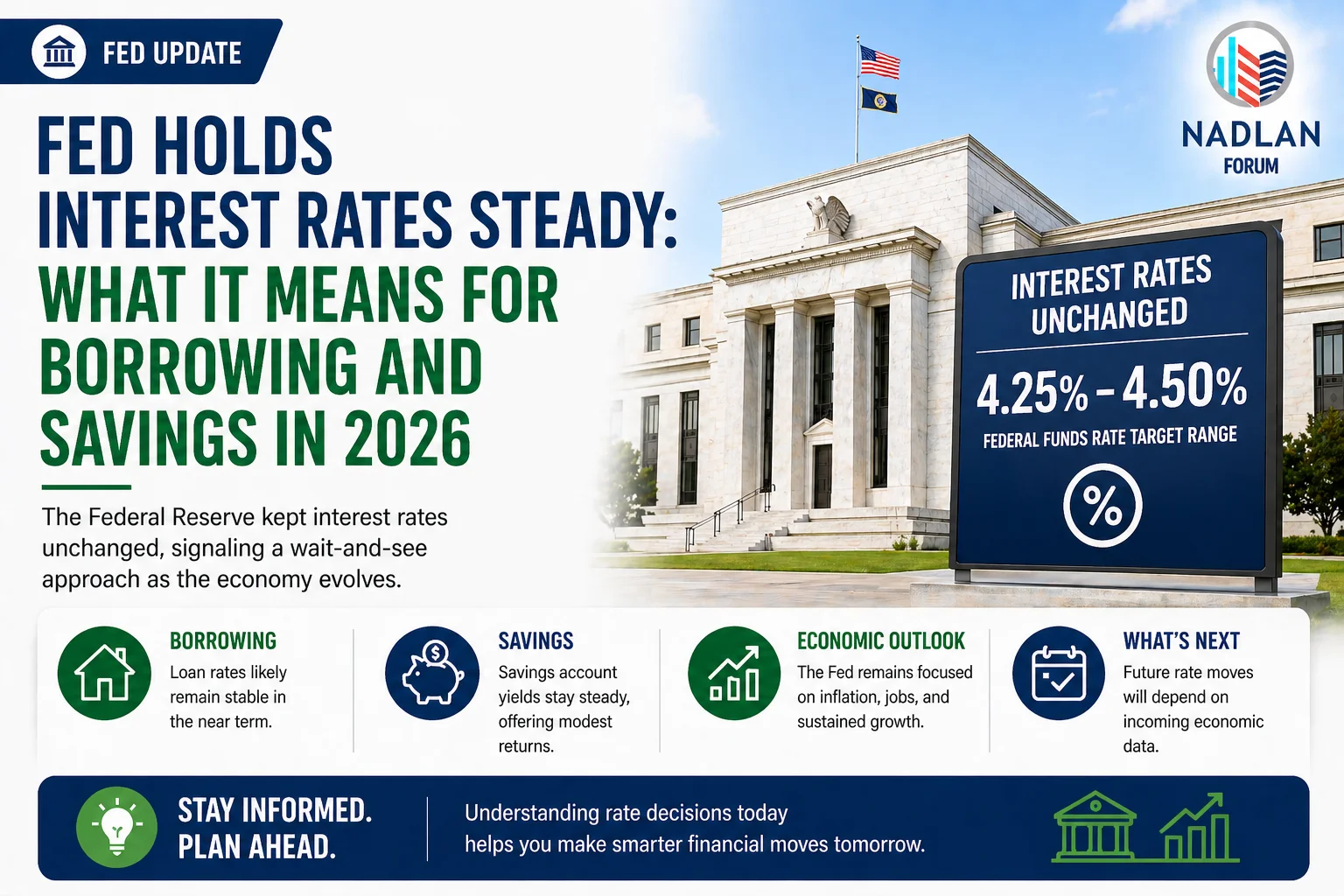

Mortgage and refinance interest rates today, January 31, 2026: Dropping below 6%

Mortgage rates closed out the week with very little movement, even as other parts of the financial market saw sharp swings. In fact, rates were so calm that Wednesday, Thursday, and Friday all posted the exact same average level for 30-year fixed mortgages a rare occurrence that only happens a handful of times each year.

The reason is simple: mortgage rates are tied closely to the bond market, and bonds spent this week in a holding pattern. After a burst of volatility earlier in the month, investors stepped back, allowing rates to settle into a tight range while markets wait for more meaningful economic data expected next week.

Mortgage Rates Today: January 31, 2026

According to data from the Zillow lender marketplace, the average 30-year fixed mortgage rate remains below 6%, holding at 5.91%. The 15-year fixed rate is currently 5.44%.

Zillow’s reported rates often run lower than those published by Freddie Mac because each source collects data differently. Zillow pulls rates directly from lenders offering loans, while Freddie Mac relies on closed loan applications.

Current Mortgage Rates

- 30-year fixed: 5.91%

- 20-year fixed: 5.86%

- 15-year fixed: 5.44%

- 5/1 ARM: 5.93%

- 7/1 ARM: 6.04%

- 30-year VA: 5.50%

- 15-year VA: 5.13%

- 5/1 VA: 5.16%

Rates shown are national averages and rounded to the nearest hundredth.

Mortgage Refinance Rates Today

Refinance rates remain slightly higher than purchase rates, which is typical, though the gap has narrowed compared to recent months.

- 30-year fixed refinance: 6.09%

- 20-year fixed: 5.95%

- 15-year fixed: 5.57%

- 5/1 ARM: 6.16%

- 7/1 ARM: 5.86%

- 30-year VA: 5.54%

- 15-year VA: 5.29%

- 5/1 VA: 5.34%

Lower rates over the past few weeks have already driven a strong increase in refinance applications, and many homeowners are watching closely to see if rates dip further.

Why Mortgage Rates Are Barely Moving

While stocks, currencies, and global bonds have reacted to geopolitical headlines and economic reports, mortgage rates have been mostly insulated. That’s because bond markets are consolidating, not trending sharply in either direction.

Investors are waiting for clearer signals from upcoming data, including inflation readings and labor market reports. Until then, rates are likely to remain range-bound rather than make large moves.

30-Year vs. 15-Year Mortgage Rates

A 30-year fixed mortgage remains the most popular option because it offers lower monthly payments and predictable costs over time. However, it comes with higher total interest paid over the life of the loan.

A 15-year fixed mortgage offers a lower interest rate and faster payoff, saving borrowers a significant amount in interest. The trade-off is a much higher monthly payment.

Choosing between the two often depends on budget flexibility, long-term plans, and comfort with higher monthly costs.

Adjustable-Rate Mortgages: Still Worth Considering?

Adjustable-rate mortgages (ARMs) lock in a rate for a set number of years before adjusting annually. While ARMs can offer lower starting rates, fixed-rate loans have recently been just as competitive — and sometimes even cheaper.

ARMs may still make sense for buyers who plan to sell or refinance before the adjustment period ends, but they carry more risk if rates rise later.

Is Now a Good Time to Buy or Refinance?

Compared to the past two years, today’s housing market looks more balanced. Home prices are no longer surging, inventory has improved in many areas, and mortgage rates are well below last year’s highs.

The best time to buy or refinance is less about timing the market and more about personal needs, financial stability, and long-term plans. Rates under 6% have already opened the door for many buyers and refinancers who were priced out earlier.

Mortgage Rates Today: Key Takeaways

- Mortgage rates ended the week flat after several calm trading days

- The average 30-year fixed rate remains below 6%

- Bond markets are waiting for stronger economic signals

- Refinance activity remains elevated due to recent rate drops

- Short-term rate movement is likely to stay limited until new data arrives

As February begins, all eyes will be on next week’s economic reports to see whether mortgage rates break out of their narrow range or continue to drift quietly sideways. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses