Are Mortgage Rates About to Shift as the Fed Prepares for a Key Decision?

Mortgage rates have been steady for months, but that could change soon. The Federal Reserve is set to announce its next rate decision on December 10, and it may be the most important Fed meeting in more than a year. It’s the first time since mid-2024 that a rate cut is not guaranteed, which means the market could be caught off guard.

According to Fed Funds Futures where investors place bets on what the Fed will do markets believe there is over an 85% chance of a rate cut next week. Usually, when expectations are this strong, the probability is above 95%. That gap leaves room for uncertainty.

Some may think that if the Fed cuts rates, mortgage rates will automatically fall. But the relationship is not that simple, and several factors could influence what happens next.

A Rate Cut May Not Cause Mortgage Rates to Drop

Even if a slice of the market is surprised by a rate cut, longer-term rates like mortgage rates do not always react the same way as the Fed’s short-term rate. Mortgage rates are driven by the bond market, and the bond market looks far beyond today’s Fed move.

One important factor this week will be the Fed’s dot plot, which appears only four times per year. The dot plot shows every Fed official’s forecast for where rates should go over the next few years.

The dot plot often receives more attention than the rate cut itself. That means:

- The Fed could cut rates next week…

- But if the dot plot shows fewer cuts in 2026…

- Mortgage rates could actually rise, even on the same day the Fed cuts.

This has happened before, and markets will be watching closely for any shift in future rate expectations

Fed Chair Powell Could Also Push Rates in Either Direction

Thirty minutes after the rate decision, Fed Chair Jerome Powell will hold a press conference. Powell often clarifies or resets market expectations. His comments can move markets just as much as the announcement or dot plot.

If Powell signals that the Fed may slow its easing plans, the bond market could respond by pushing mortgage rates higher, even if a cut takes place. On the other hand, if he leans toward a more supportive tone, rates could drift lower.

Markets May Wait for the Jobs Report Before Making Big Moves

Another reason mortgage rates have stayed calm is that traders are waiting for missing economic data.

The October jobs report never came out due to the government shutdown. Only half of the report was completed, and it will not be released until December 16, along with the November report.

Because job data is one of the most important indicators for the Fed, the delay leaves markets without a key piece of information they normally rely on before a major meeting.

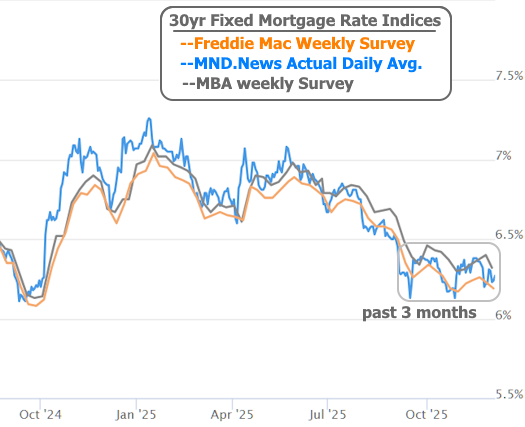

Since early September, mortgage rates have moved mostly sideways, holding near the lowest levels since late 2024. The next big shift may not come until more complete labor market data is available.

Job Openings Data Could Be an Early Signal

The one economic wild card before the Fed decision will be Tuesday morning’s Job Openings report. Normally, job openings trail the employment report by one month, but this time the schedule is reversed because of the shutdown.

This means the job openings number will be the first look at October labor conditions, giving traders a rare early signal before they see full jobs data.

Because of this unusual timing, the report may carry more weight than usual and could move bond markets and mortgage rates ahead of the Fed meeting.

What It All Means for Mortgage Rates

Rates have been calm, but that calm may not last. Several upcoming events could shift the market:

- December 10 Fed rate decision

- Dot plot release

- Powell’s press conference

- Job Openings report

- Delayed October and November jobs reports

Any of these could push rates out of the sideways pattern they’ve held for months. For now, mortgage rates remain near the lowest levels in almost a year, but markets are preparing for potential movement. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses