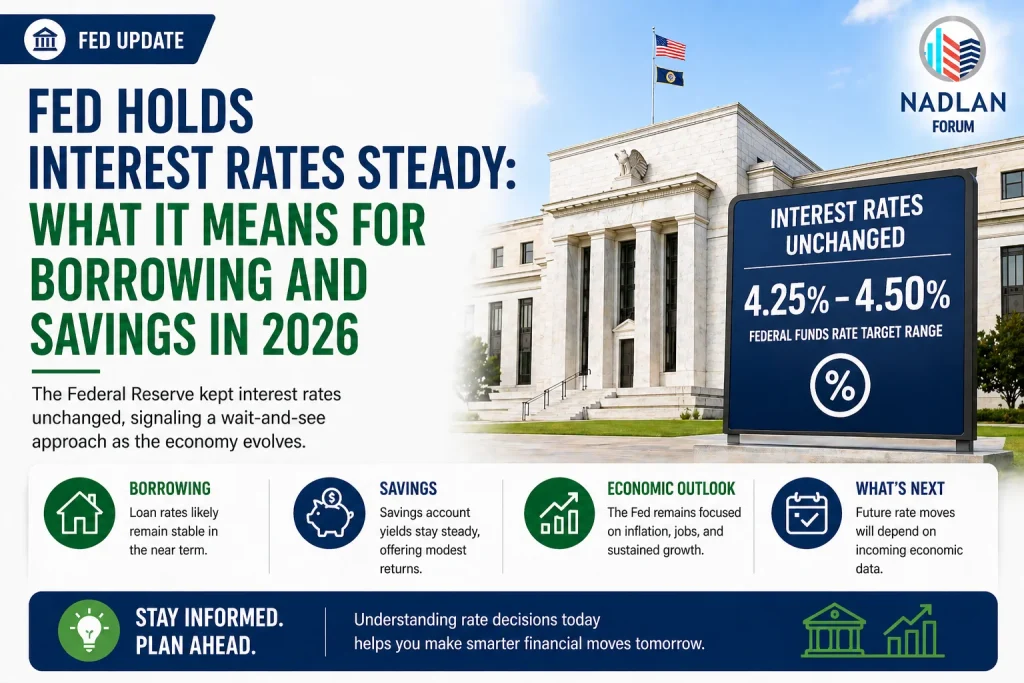

Fed Holds Interest Rates Steady: What It Means for Borrowing and Savings in 2026

The Federal Reserve has decided to keep interest rates unchanged following its latest policy meeting in April 2026. This decision keeps the federal funds rate within a target range of 3.5% to 3.75%.

The move comes during a period of economic uncertainty, rising inflation, and leadership transition at the central bank. It may also mark the final meeting led by Jerome Powell before a potential change in leadership.

Why the Fed Is Holding Rates Steady

Policymakers are balancing several key concerns:

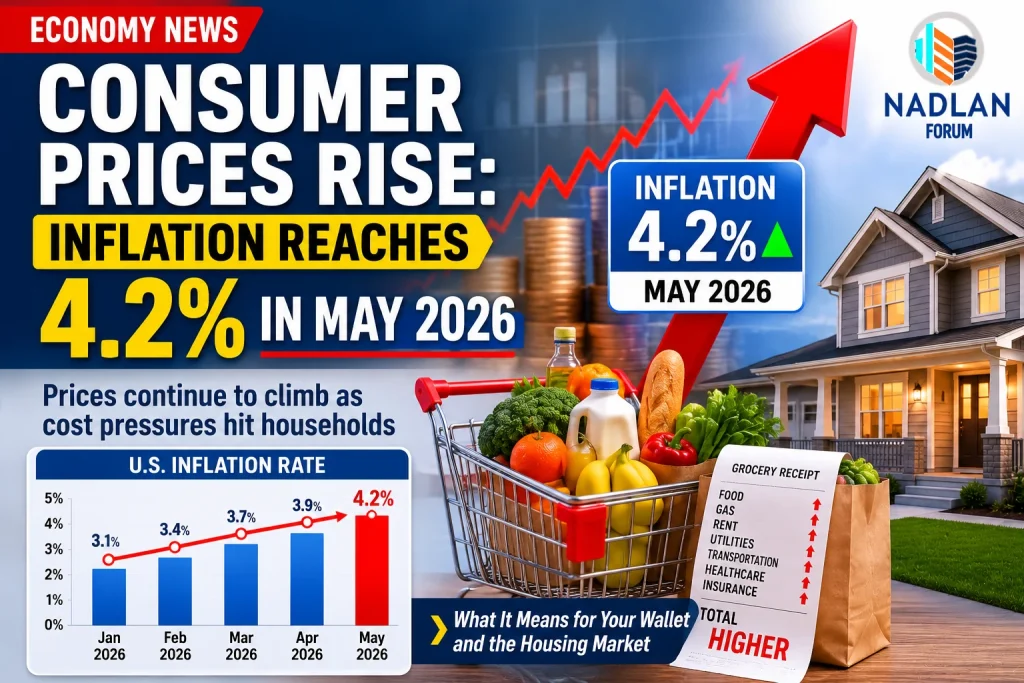

- Inflation has increased, partly due to higher energy costs

- Global tensions are adding pressure to the economy

- The job market is showing slower growth

Because of these factors, the Fed has chosen not to adjust rates for now. Holding rates steady allows time to evaluate how these conditions develop before making further changes.

What This Means for Consumers

The Fed’s benchmark rate influences many financial products, even though it does not directly set all borrowing costs. When rates remain unchanged, many consumer rates also stay elevated.

Here’s how the decision affects different areas of personal finance:

Credit Cards: High Rates Continue

Credit cards are one of the most directly affected by Fed policy because they typically have variable interest rates.

- Average credit card rates remain close to 20%

- Carrying a balance continues to be expensive

- Without rate cuts, relief is unlikely in the near term

For borrowers, this means paying off high-interest debt should remain a priority.

Mortgage Rates: Still Elevated

Mortgage rates do not move directly with the Fed but are influenced by long-term bond yields and inflation expectations.

Recent data shows that 30-year mortgage rates have moved higher compared to earlier in the year.

- Rates are above 6% in most cases

- Higher borrowing costs are limiting affordability

- Many homeowners are holding onto older, lower-rate mortgages

This has slowed buying and refinancing activity, as fewer borrowers are willing to take on higher rates.

Student Loans: Limited Impact

Federal student loans are less affected by short-term rate decisions.

- Rates are set based on government bond yields

- Current undergraduate loan rates are around 6.39%

- Existing borrowers are mostly protected from changes

Future rates will depend on upcoming Treasury auctions, but overall, student loan costs remain relatively stable.

Car Loans: Payments Stay High

Auto loan rates are influenced by both the Fed’s benchmark and broader market conditions.

- Interest rates for car loans remain high

- Monthly payments have reached record levels

- Buyers are choosing longer loan terms to reduce monthly costs

For example, the average monthly payment for a new car has climbed above $700, reflecting both higher prices and financing costs.

Savings Rates: A Positive Side

One benefit of higher interest rates is better returns for savers.

- High-yield savings accounts offer around 4%

- Certificate of deposit (CD) rates remain competitive

- Returns are still above inflation in some cases

Although rates have come down slightly from recent peaks, they are still stronger than in previous years.

Broader Economic Impact

Keeping interest rates steady has wider effects on the economy:

- Borrowing remains expensive, slowing spending

- Businesses may delay expansion due to higher costs

- Consumers may cut back on non-essential purchases

At the same time, stable rates provide some predictability, which can help financial markets and long-term planning.

Leadership Change at the Fed

This decision comes as leadership at the central bank may soon change. Donald Trump has nominated Kevin Warsh to replace Powell as chair.

A change in leadership could influence future interest rate policy, depending on economic conditions and policy priorities.

Key Takeaways

- The Fed kept interest rates unchanged at 3.5% to 3.75%

- Credit card and loan rates remain high

- Mortgage rates continue to affect housing affordability

- Savings rates remain relatively strong

- Economic uncertainty is delaying any rate cuts

Final Outlook

The Fed’s decision to hold rates steady reflects a cautious approach during uncertain economic conditions. While this helps control inflation, it also keeps borrowing costs high for consumers.

For now, households should focus on managing debt, comparing financial options, and taking advantage of higher savings returns where possible.

Future rate changes will depend on how inflation, job growth, and global conditions evolve in the months ahead. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses