The Homeownership Equation Is Shifting: Rent vs. Buy Gap Narrows Nationwide

New data from Realtor.com reveals a surprising trend: the long-standing financial divide between renting and buying a home is beginning to narrow. For many Americans weighing whether to stay put or take the leap into homeownership, the answer might soon be changing.

In June 2025, the national median asking rent for 0–2 bedroom units dropped to $1,711 a 2.1% year-over-year decline. This marks the 23rd consecutive month of falling rents, bringing the national rent just $48 below its peak in August 2022. Yet, despite this modest decline, rental prices remain nearly 19% higher than they were in June 2019.

According to Danielle Hale, Chief Economist at Realtor.com, affordability remains the biggest driver of housing decisions. “High mortgage rates and lingering elevated home prices still make renting the cheaper option in most markets,” she said. “But the fact that the cost gap is narrowing is a signal to renters: the tide may be turning.”

Where the Numbers Stand

Across the 50 largest U.S. metro areas, median rents declined $36 year-over-year, while all property sizes saw drops: studio rents fell 2.3%, one-bedrooms decreased 2.6%, and two-bedrooms dipped 2.1%.

Despite these softening trends, buying a home is still more expensive than renting in 49 of the top 50 metros. The outlier? Pittsburgh, where monthly costs of homeownership remain slightly below average rental prices.

But the scales may be tipping. The average monthly cost difference between renting and buying in the U.S. now sits at $908 a $48 improvement for buyers compared to last year. In markets like San Jose, where renters previously saved over $2,600 per month versus buyers, that margin has shrunk by $349 in the past year alone. Even in Austin, Texas a city that saw explosive growth during the pandemic renters are now saving less than they were in 2024, signaling a slow but steady shift in the market.

Markets in Motion

Several metros are experiencing dramatic swings in housing dynamics. Memphis, Tennessee, for example, has shifted from being a buying-favored market to one where renting is more cost-effective. Similarly, Birmingham, Alabama has seen rental savings surge, while areas like Fresno, California and Spokane, Washington once magnets for remote workers during the pandemic—are experiencing an uptick in out-of-market searches as affordability erodes.

“Market conditions can flip quickly,” Hale noted. “What’s true in one year might look very different the next, especially as interest rates, housing stock, and economic trends evolve.”

What’s Fueling the Shift?

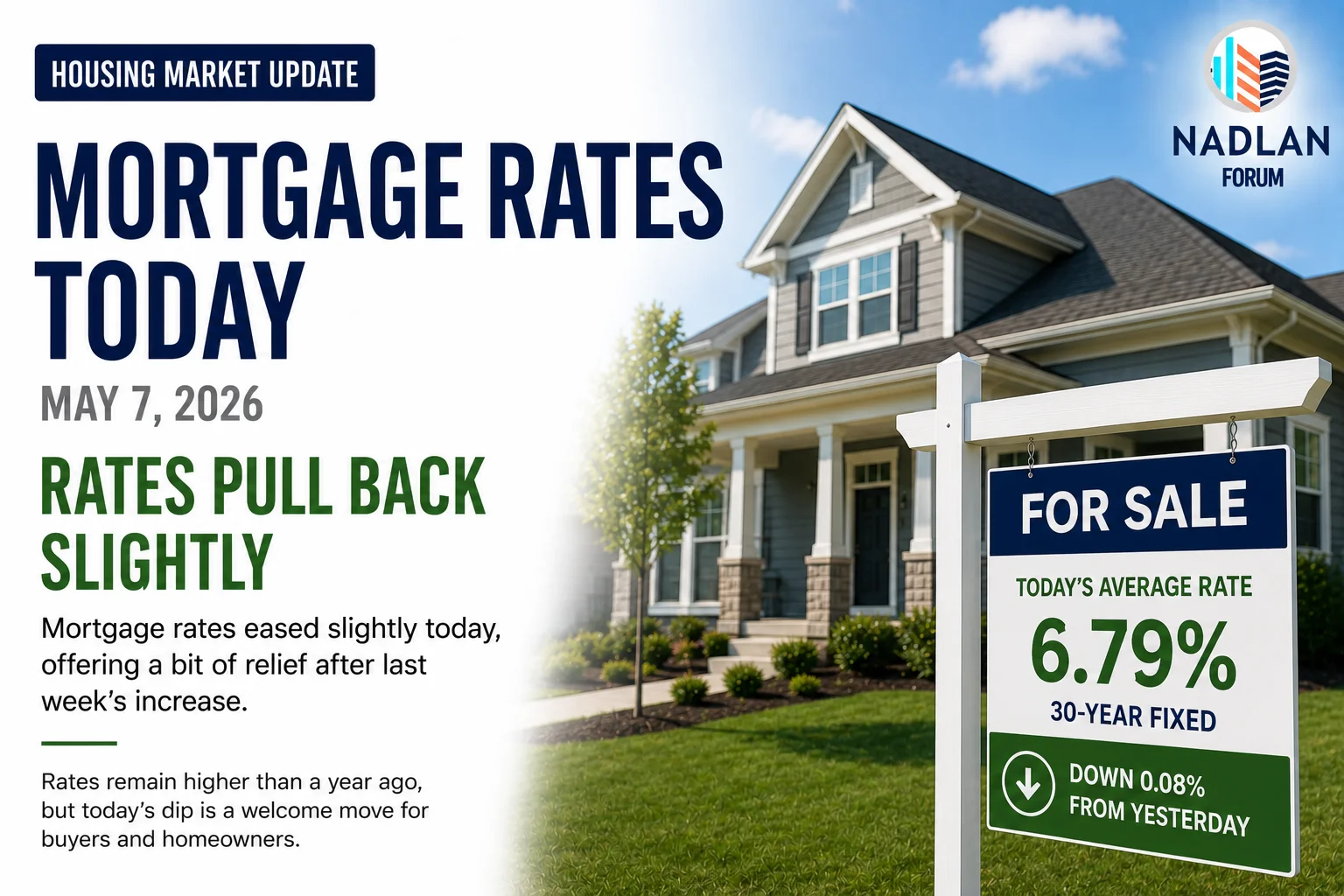

The direction of mortgage rates remains a key factor. As of mid-July, Freddie Mac reported the average 30-year fixed-rate mortgage at 6.75%, slightly up from last week but still consistent with rates over the past year. A year ago, the same loan averaged 6.77%.

Sam Khater, Chief Economist at Freddie Mac, believes stability in mortgage rates even if slightly elevated combined with growing inventory, could be enough to nudge would-be buyers off the sidelines.

And indeed, inventory is rising. Realtor.com’s June report shows that active listings have grown for 20 consecutive months, with a 28.9% year-over-year increase last month. That follows a 30.1% surge in May, offering renewed hope to buyers long frustrated by tight supply.

For the second month in a row, the number of available homes exceeded 1 million, a promising sign that the market is normalizing after years of pandemic-fueled disruptions. Inventory levels are still 12.9% below their 2017–2019 averages, but the gap is narrowing faster than expected.

All four major U.S. regions reported increased housing supply in June, with the West leading the way at 38.3%, followed by the South at 29.4%, the Midwest at 21.3%, and the Northeast at 17.6%.

What It Means for Homebuyers and Renters

For renters who have been patiently waiting for their opportunity to buy, the landscape is starting to shift. The growing inventory gives buyers more choices, while a stable interest rate environment provides a window for planning ahead.

Still, affordability remains a challenge. Even as the rent-versus-buy gap closes, buying remains a premium option in most urban markets at least for now. But if rates decline and inventory continues to build, the balance could tip.

“Consumers who are watching the market closely particularly renters should stay informed,” Hale advised. “With inventory rising and price pressures moderating, their moment may come sooner than they think.”

In a housing market still regaining its footing, the narrowing rent-buy gap is more than a number. It’s a signal that change is underway and for many, the American dream of homeownership may be within reach once again. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses