U.S. Mortgage Delinquencies Fall in March 2026: Foreclosure Inventory Continues to Rise

The U.S. mortgage market showed mixed signals in March 2026. While fewer borrowers fell behind on their payments, the number of homes already in foreclosure continued to grow.

According to new data from Intercontinental Exchange, early-stage loan performance improved during the month, but longer-term risks are still building in the system.

Delinquencies Improve with Seasonal Trends

Mortgage delinquencies moved lower in March, following a pattern that is common during the spring season.

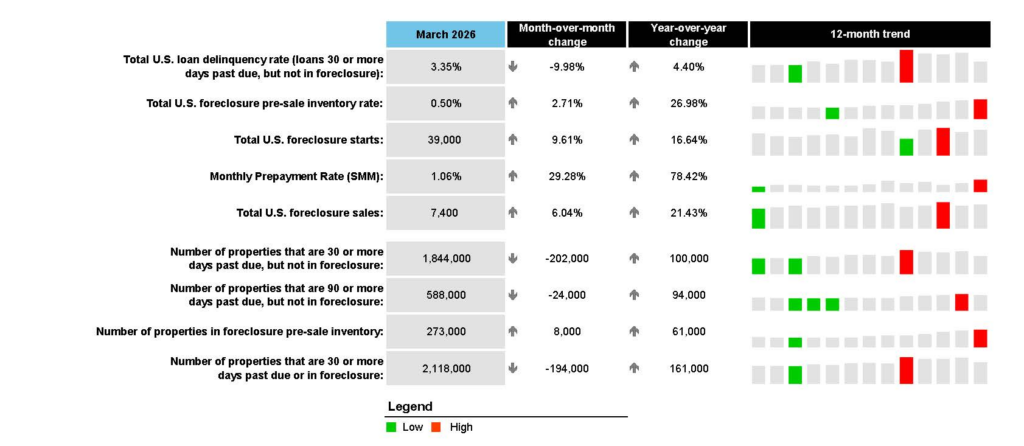

The national delinquency rate dropped to 3.35%, a decline of 37 basis points from February. This improvement was mainly driven by fewer loans entering delinquency and better recovery activity among borrowers.

Even with this progress, the rate is still slightly higher than it was one year ago, showing that overall conditions have not fully returned to earlier levels.

Fewer New Late Payments and Better Loan Recovery

One of the key positive trends is the reduction in new delinquency cases.

- New delinquencies fell by 23% compared to the previous month

- The number of loans moving into more serious stages (60 and 90 days past due) also declined

- Loan “cures,” where borrowers catch up on missed payments, increased significantly

In March alone, about 547,000 loans returned to current status, marking a 27% increase from February. This suggests that many borrowers are managing to recover from short-term financial challenges.

Prepayment Activity Reaches Multi-Year High

Another notable trend is the rise in prepayment activity, which includes refinancing or paying off loans early.

Prepayment speeds increased sharply:

- Up 78% compared to March 2025

- Reached 1.06%, the highest level in nearly four years

This increase is likely linked to slightly lower mortgage rates, which are encouraging some homeowners to refinance or pay down their loans faster.

Non-Current Loans Decline but Remain Elevated

The total number of non-current loans those that are either delinquent or in foreclosure declined during March.

- Total non-current loans dropped by about 194,000

- The total now stands at 2.12 million

However, this figure is still more than 8% higher than the same time last year, indicating that overall loan stress has not fully eased.

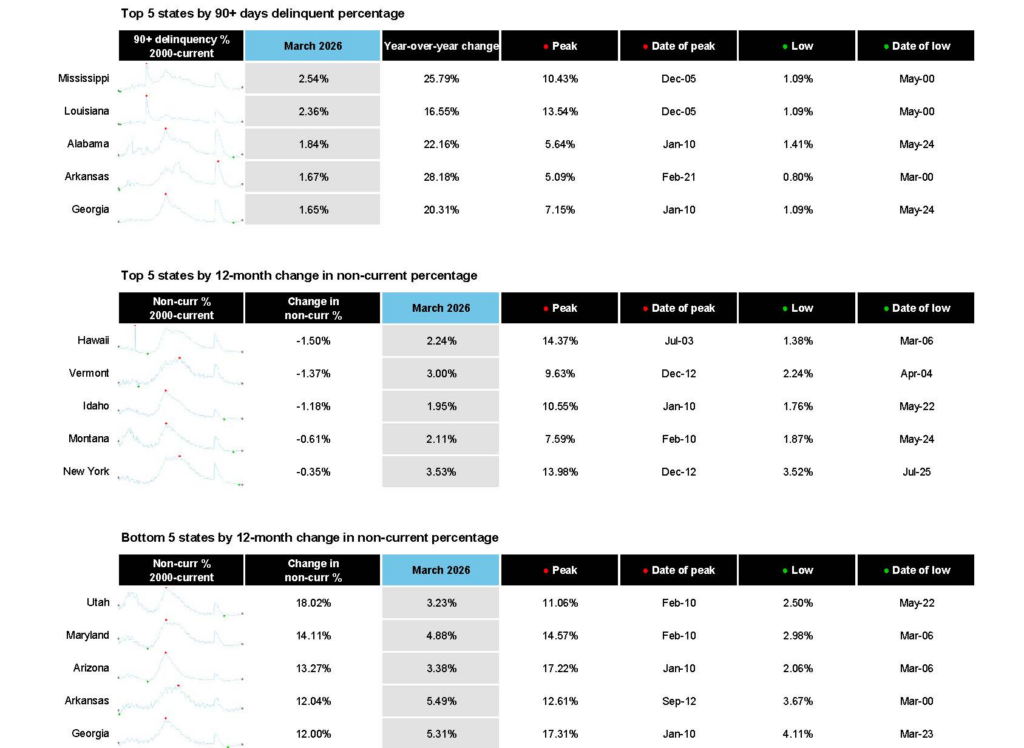

Serious Delinquencies Continue to Rise

While early-stage delinquencies improved, more serious cases are still increasing.

There are currently about 154,000 more borrowers who are:

- 90 days or more past due, or

- Already in the foreclosure process

This trend is important because serious delinquencies are more likely to lead to foreclosure if not resolved.

Foreclosure Activity and Inventory Increase

Foreclosure activity continued to move higher in March.

- Foreclosure starts increased by 17% compared to last year

- Property sales related to foreclosure rose by 21%

Most notably, the total number of homes in active foreclosure reached 273,000. This is the highest level recorded since early 2020, marking a six-year high.

This rise reflects the buildup of cases that began during earlier periods of financial stress and are now moving through the system.

What This Means for the Housing Market

The latest data shows a mixed picture:

Positive signs:

- Fewer new delinquencies

- Higher cure rates

- Increased prepayment activity

Areas of concern:

- Rising serious delinquencies

- Growing foreclosure inventory

- Higher non-current loan levels compared to last year

Overall, most homeowners are still managing their mortgage payments, but a smaller group of borrowers is facing ongoing financial challenges.

Broader Economic Context

Several factors are influencing mortgage performance:

- Higher interest rates compared to previous years

- Increased living costs

- Economic uncertainty in some sectors

These conditions can make it harder for some borrowers to stay current on their loans, especially those already under financial pressure.

Key Takeaways

- Mortgage delinquencies declined in March due to seasonal improvement

- Loan recovery activity increased significantly

- Prepayment activity reached its highest level in nearly four years

- Serious delinquencies and foreclosure inventory continue to rise

- Overall loan performance is stable but shows signs of stress in certain areas

Final Outlook

The U.S. mortgage market is showing signs of short-term improvement, especially in early-stage delinquencies. However, the increase in serious delinquencies and foreclosure inventory suggests that risks are still present.

As the year continues, trends in employment, interest rates, and inflation will play a major role in shaping mortgage performance. For now, the market remains stable overall, but with areas that require close attention. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses