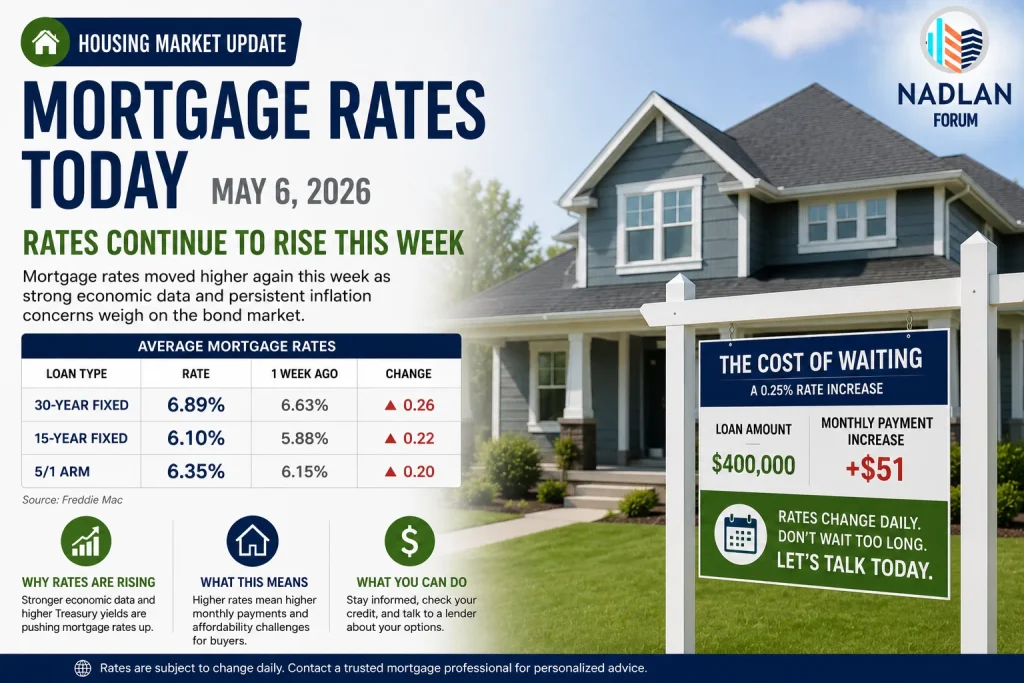

Mortgage Rates Today May 6, 2026: Rates Continue to Rise This Week

Overview of Current Mortgage Trends

Mortgage rates in the U.S. are moving upward again this week, continuing a pattern seen over recent days. Whether you compare rates to the start of the year or just the past few days, fixed-rate home loans are trending higher.

Data from Zillow shows that several key mortgage rates increased within a single day, reflecting ongoing pressure in the housing finance market. This rise may affect both homebuyers and homeowners planning to refinance.

Today’s Mortgage Rates

Here are the latest average mortgage rates:

- 30-year fixed: 6.31%

- 20-year fixed: 6.22%

- 15-year fixed: 5.71%

- 5/1 ARM: 6.31%

- 7/1 ARM: 6.15%

- 30-year VA: 5.91%

- 15-year VA: 5.55%

- 5/1 VA: 5.79%

These figures represent national averages and may vary based on location, lender, and borrower profile.

The 30-year fixed rate increased by nine basis points in just one day, while shorter-term loans like the 15-year and 20-year options also saw noticeable gains. Since the beginning of the year, these shorter-term loans have risen by nearly 0.30 percentage points.

Today’s Refinance Rates

Refinance rates are also moving higher. Here are the current averages:

- 30-year fixed refinance: 6.29%

- 20-year fixed refinance: 6.37%

- 15-year fixed refinance: 5.70%

- 5/1 ARM refinance: 6.14%

- 7/1 ARM refinance: 5.99%

- 30-year VA refinance: 5.72%

- 15-year VA refinance: 5.18%

- 5/1 VA refinance: 6.14%

In many cases, refinance rates can be slightly higher than purchase rates, though this depends on market conditions and borrower details.

Why Mortgage Rates Are Rising

Mortgage rates are influenced by several factors, including inflation, economic growth, and decisions by central banks. When inflation remains elevated, lenders often increase rates to manage risk.

Recent market conditions suggest that investors expect borrowing costs to stay higher for longer. This has pushed up yields in the bond market, which directly impacts mortgage pricing.

Even small increases in rates can significantly affect monthly payments, especially for long-term loans.

30-Year vs 15-Year Mortgage: Key Differences

30-Year Fixed Mortgage

A 30-year fixed mortgage remains the most popular option for buyers. Its main advantage is lower monthly payments, since the loan is spread over a longer period.

It also offers stable payments because the interest rate does not change over time. This makes budgeting easier for homeowners.

However, the downside is higher total interest costs. Over 30 years, borrowers pay significantly more interest compared to shorter loan terms.

15-Year Fixed Mortgage

A 15-year mortgage offers lower interest rates and allows borrowers to pay off their home faster. This can save a large amount in total interest over the life of the loan.

The trade-off is higher monthly payments, as the loan must be repaid in half the time. This option is often better suited for buyers with stable income and strong financial planning.

Understanding Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages work differently from fixed loans. They offer a fixed rate for an initial period, such as five or seven years, and then adjust annually.

For example, a 5/1 ARM keeps the same rate for five years before changing each year after that.

The main benefit is a lower starting rate, which can reduce early monthly payments. However, there is risk involved. After the fixed period ends, rates may increase, leading to higher payments.

This option may work well for buyers who plan to move or refinance before the adjustment period begins.

What Rising Rates Mean for Buyers and Homeowners

As mortgage rates increase, affordability becomes more challenging. Higher rates lead to higher monthly payments, which can reduce the amount buyers are able to borrow.

For homeowners considering refinancing, rising rates may limit opportunities to secure better terms. However, those who can improve their credit score or reduce debt may still find competitive options.

Tips to Get a Lower Mortgage Rate

- Improve your credit score before applying

- Reduce your debt-to-income ratio

- Compare offers from multiple lenders

- Consider a shorter loan term if affordable

- Make a larger down payment

These steps can help borrowers secure better rates even in a rising market.

Final Thoughts

Mortgage rates today in May 2026 are showing an upward trend, and this may continue depending on economic conditions. Buyers and homeowners should stay informed and carefully compare options before making decisions.

Even small changes in interest rates can have a long-term impact, so planning ahead and understanding loan types is more important than ever. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses