Mortgage Refinance Savings in 2026: Study Shows Millions Could Lower Payments

Many homeowners who purchased properties during the high-rate environment of the past few years may finally have an opportunity to reduce their monthly housing costs.

According to a new LendingTree study, nearly one-third of borrowers who took out a 30-year fixed mortgage between 2023 and 2025 could save money by refinancing at mortgage rates available in early April 2026.

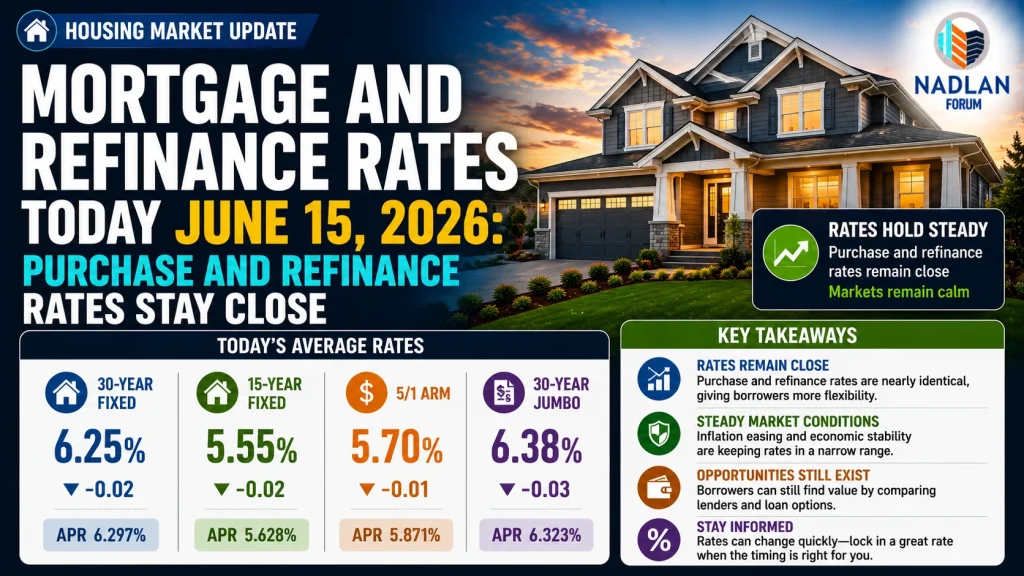

Researchers compared mortgage rates from government housing data against the average 30-year fixed mortgage rate of 6.37% recorded in early April. The analysis focused on homeowners whose existing mortgage rate was at least half a percentage point higher than current market rates.

The results showed that 32.5% of recent borrowers could benefit from refinancing, with estimated average savings of roughly $2,320 per year.

Mortgage Rates Have Improved Since Their Peak

Mortgage rates climbed sharply during 2023 and reached their highest levels in decades.

According to Freddie Mac, the average 30-year fixed mortgage rate peaked near 7.79% in October 2023, the highest level since 2000.

Although rates remain elevated compared to the historic lows seen during 2020 and 2021, they have moved lower since that peak. By early April 2026, the average rate had declined to 6.37%.

That drop created potential refinance opportunities for many homeowners who locked in mortgages when rates were significantly higher.

Average Savings Could Exceed $2,300 Per Year

LendingTree found that borrowers refinancing from higher mortgage rates to around 6.37% could reduce their housing expenses in a meaningful way.

Refinance Potential by Origination Year

| Year | % Eligible to Benefit | Avg. Monthly Savings | Avg. Annual Savings |

|---|---|---|---|

| 2025 | 25.1% | $152 | $1,822 |

| 2024 | 34.7% | $191 | $2,291 |

| 2023 | 37.7% | $223 | $2,680 |

| 2023–2025 Combined | 32.5% | $193 | $2,320 |

Borrowers who purchased homes earlier in the rate cycle generally stand to benefit the most.

Homeowners who secured mortgages in 2023 were more likely to refinance successfully because rates were significantly higher at that time.

Falling Rates Could Expand Refinance Opportunities

The study also examined what would happen if mortgage rates dropped even further.

When researchers modeled a refinancing environment with rates near 6.00%, the percentage of homeowners who could benefit jumped sharply from 32.5% to 56.6%.

That means more than half of recent homebuyers could potentially reduce their monthly payments if rates continue easing later this year.

The findings show how sensitive refinance demand remains to even modest movements in mortgage rates.

Refinancing Is Not Free

Although refinancing can generate savings, experts note that it still comes with upfront costs.

Typical refinance expenses often range from 2% to 6% of the loan amount, depending on the lender and loan structure.

For example:

- A $400,000 mortgage refinance could cost between $8,000 and $24,000

- Fees may include appraisals, closing costs, title services, and lender charges

- Borrowers need enough monthly savings to recover those costs over time

This is why analysts used a half-point rate reduction as the benchmark for meaningful refinance savings.

Smaller rate improvements may not justify the refinancing expense for every borrower.

Economic Uncertainty Continues Impacting Mortgage Rates

Mortgage rates have remained volatile throughout 2026 due to inflation concerns, Treasury yield movements, and global economic uncertainty.

For a brief period in February 2026, the average 30-year mortgage rate dipped below 6% for the first time since 2022.

However, rates quickly moved higher again after geopolitical tensions in the Middle East intensified and inflation pressures returned to financial markets.

The study noted that mortgage rates climbed again following the start of the Iran conflict, which pushed Treasury yields and borrowing costs higher.

Midwest and Northeast States Show Strongest Refinance Potential

The percentage of homeowners who could benefit from refinancing varies significantly by state.

States in the Midwest and Northeast dominated the list of areas where borrowers may see the biggest refinance opportunities.

States With the Highest Share of Borrowers Who Could Benefit

| Rank | State | % of Borrowers Who Could Benefit |

|---|---|---|

| 1 | New Hampshire | 42.5% |

| 2 | Illinois | 42.4% |

| 2 | Indiana | 42.4% |

| 4 | Michigan | 41.8% |

| 5 | Ohio | 41.4% |

| 6 | Maine | 39.9% |

| 7 | Missouri | 39.5% |

| 8 | Wisconsin | 37.9% |

| 9 | Minnesota | 37.4% |

| 10 | New Jersey | 37.2% |

These states generally saw larger portions of borrowers secure mortgages during periods of elevated rates.

Some States Show Lower Refinance Demand

Other states showed much smaller percentages of homeowners who would benefit from refinancing at current rates.

States With the Lowest Share of Borrowers Who Could Benefit

| Rank | State | % of Borrowers Who Could Benefit |

|---|---|---|

| 1 | Alaska | 20.0% |

| 2 | North Dakota | 21.7% |

| 3 | South Dakota | 22.8% |

| 4 | Idaho | 24.0% |

| 5 | Hawaii | 26.0% |

| 6 | Utah | 26.1% |

| 6 | Iowa | 26.1% |

| 8 | Wyoming | 26.7% |

| 9 | Texas | 27.2% |

| 10 | Alabama | 27.3% |

In many of these states, borrowers either secured lower rates initially or experienced different local lending conditions.

California Borrowers Could Save the Most

While some states had fewer eligible borrowers, homeowners in expensive housing markets could potentially save much more money each month.

California ranked highest for potential monthly refinance savings.

Highest Potential Monthly Savings by State

| State | Avg. Monthly Savings |

|---|---|

| California | $363 |

| Hawaii | $355 |

| District of Columbia | $273 |

| Washington | $259 |

| Massachusetts | $246 |

Higher home prices and larger mortgage balances often lead to greater refinance savings opportunities when rates decline.

Refinancing Could Improve Household Budgets

For many homeowners, even moderate monthly savings can make a meaningful financial difference.

Reducing mortgage payments could help families:

- Build emergency savings

- Pay down debt

- Increase retirement contributions

- Improve monthly cash flow

- Manage rising living expenses

In today’s higher-cost economic environment, lower housing expenses remain an important financial goal for many households.

Homeowners Still Need to Compare Costs Carefully

Financial experts continue recommending that homeowners carefully calculate the full cost of refinancing before moving forward.

Important factors include:

- Closing costs

- Loan term length

- Break-even period

- Future housing plans

- Current mortgage balance

Borrowers planning to move within a few years may not remain in the property long enough to recover refinance expenses.

Refinance Activity Could Grow Later in 2026

If mortgage rates stabilize or move lower during the second half of 2026, refinance activity could increase significantly.

Many homeowners who delayed refinancing while rates remained elevated may begin reentering the market if borrowing costs improve further.

Although rates remain well above pandemic-era lows, even small declines are now creating opportunities for millions of borrowers who purchased homes during the peak of the recent rate cycle.

For many households, monitoring mortgage rates closely over the coming months could lead to meaningful long-term savings. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses