How Your Credit Score Can Save (or Cost) You Thousands on a Mortgage in 2025

In today’s housing market, mortgage rates are still hovering well above the record lows we saw during the pandemic. Just a few short years ago, locking in a 30-year fixed loan at 2% to 3% was entirely possible. Those days, however, are gone at least for now.

Since 2022, rates have been closer to 7%, a level we hadn’t seen since 2007. But here’s the good news: you have more control than you might think over the rate a lender offers you especially if you’re willing to work on your credit score.

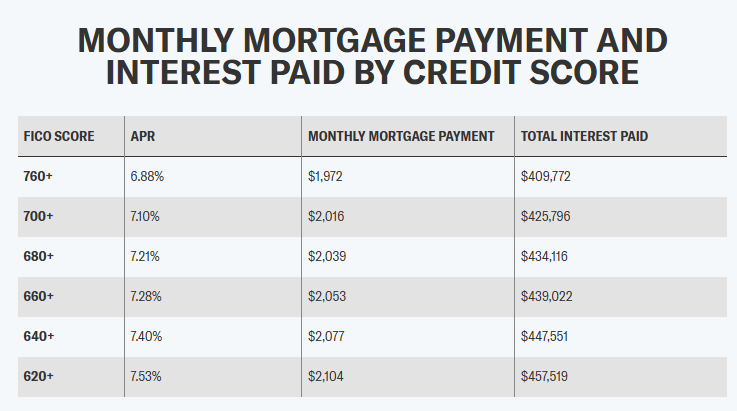

In fact, improving your score could trim as much as two-thirds of a percentage point from your mortgage rate. Over the life of a $300,000 loan, that’s nearly $48,000 in interest saved, plus about $130 less per month in payments.

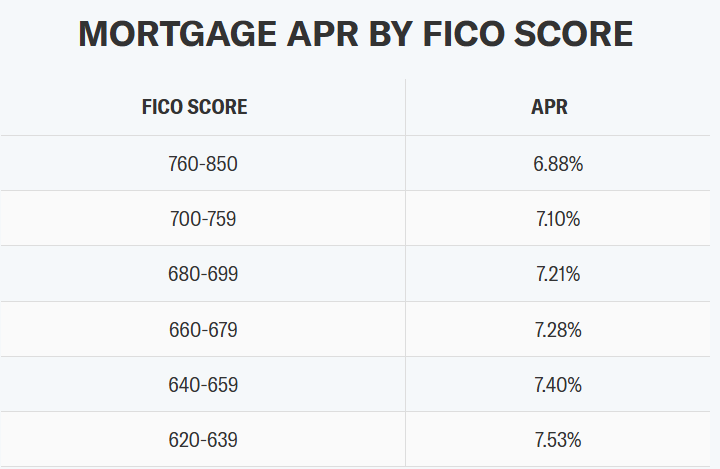

Mortgage Rates by Credit Score — August 2025

Data from Curinos for myFICO.com shows just how much your credit score can affect your interest rate:

- Excellent credit (FICO 760–850): Around 6.88% for a 30-year fixed

- Good credit (700–759): Slightly higher rates, but still competitive

- Fair credit (660–699): You’ll notice a jump in cost here

- Poor credit (620–659): Rates rise sharply, adding thousands over time

- Subprime (below 620): Mortgage approval becomes harder, and rates climb even more

Why Lenders Charge Less for Higher Scores

Your credit score is essentially your financial report card it signals to lenders how likely you are to repay on time. But it’s not the only factor they consider:

- Debt-to-Income Ratio (DTI): The percentage of your income going toward debt payments. Lower is better.

- Loan-to-Value Ratio (LTV): The size of your mortgage compared to the home’s value. A larger down payment means a lower LTV and often a better rate.

- Loan Term: Shorter terms, like 15 years, typically come with lower rates than 30-year terms.

- Loan Type: VA loans (for military-connected borrowers) often have the lowest rates, followed by USDA and FHA loans.

How Much Can You Save?

Let’s put it into perspective:

If you have an 800 FICO score, you could snag a 6.88% 30-year fixed mortgage rate. Drop that score into the mid-600s, and you might be paying 7.5% or more potentially adding tens of thousands to your total cost.

Even small improvements can pay off. For example, raising your score from 720 to 760 might lower your rate enough to save you $25 to $50 per month, which adds up over decades.

Will Rates Ever Go Back to 3%?

Probably not anytime soon. The near-3% rates of 2020 and 2021 were fueled by emergency Federal Reserve cuts to combat the pandemic’s economic impact. It would take another crisis of that scale to recreate those conditions.

For now, experts say a “good” rate is anything in the low 7% range or below though national averages, like Freddie Mac’s recent 6.72%, are slightly better than that.

Bottom line: Your credit score is one of the few levers you can pull to lower your mortgage cost right now. If you’re house hunting in 2025, investing time in boosting your score before you apply could mean the difference between overpaying and saving tens of thousands. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses