Inflation Inches Up as Jobless Claims Surprise, Adding Complexity for Fed’s Decision

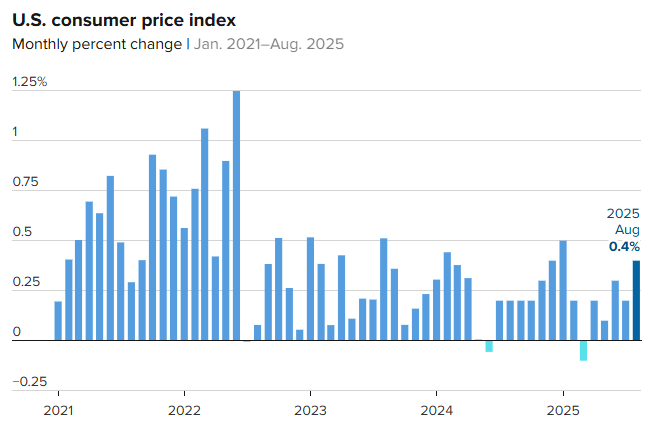

In a fresh update from the U.S. economy, consumer prices showed a notable uptick in August, adding to the mixed signals the Federal Reserve will need to consider ahead of their key policy meeting next week. The Consumer Price Index (CPI) rose by 0.4% in August, the largest monthly gain since January.

This increase drove the annual inflation rate to 2.9%, marking a 0.2 percentage point rise from July’s figure. Economists had anticipated a 0.3% monthly increase, with an annual inflation rate of 2.9%, making the actual results a touch warmer than expected but still manageable.

For a deeper look into underlying trends, the core CPI, which excludes volatile food and energy prices, climbed by 0.3% in August, bringing the 12-month figure to 3.1%. This closely watched core reading aligns with forecasts and remains a key focus for the Fed, given that it provides a clearer picture of long-term inflationary trends.

Unemployment Claims Surge, Adding Pressure on Fed’s Rate Decisions

Adding another layer of complexity, the Labor Department reported a surprising increase in weekly unemployment claims. For the week ending September 6, initial jobless claims rose to a seasonally adjusted 263,000, up from the 235,000 analysts had predicted. This figure represents the highest level of unemployment claims since October 2021, signaling potential weakening in the labor market. The rise in claims, coupled with the earlier-than-expected inflation report, will play a significant role in shaping the Fed’s policy decisions.

In response to this data, traders reacted swiftly, pushing the probability of a Federal Reserve rate cut at their September 17 meeting to near certainty. There is now also a high likelihood of further rate cuts in October and December, as market participants adjust their expectations for the Fed’s monetary policy. The data presents a nuanced situation for the Fed, with inflation numbers still below historical highs, yet signs of a cooling labor market raising fresh concerns.

Rising Shelter and Energy Costs Drive CPI Up

The main drivers of the August CPI increase were shelter costs, which are weighted heavily in the index, accounting for about one-third of its total. Shelter costs rose by 0.4% in August, marking the most significant contribution to the overall CPI increase. Alongside this, food prices saw a 0.5% rise, and energy prices increased by 0.7%. Gasoline prices, which had been volatile recently, spiked by 1.9%, a rise that could be partially attributed to the effects of new tariffs on imported goods.

Despite these increases, analysts remain cautious in interpreting the overall inflation data. The effects of President Donald Trump’s tariffs on certain goods, especially in sectors like vehicles, have led to moderate price hikes. New car prices rose by 0.3%, while used cars and trucks saw a sharper increase of 1%. This suggests that while tariffs are pushing some prices higher, their impact is relatively contained within certain sectors.

Focus on Services Costs and Long-Term Inflationary Pressures

While the Fed monitors goods prices, the central bank is particularly attuned to services costs as a more telling indicator of long-term inflation pressures. Services, excluding energy, rose by 0.3% in August, bringing the year-over-year increase to 3.6%. This is a key figure, as services prices tend to be more persistent than goods prices. Additionally, shelter costs, a major component of services, also rose by 3.6% year-over-year, a decrease from earlier in 2023 when shelter inflation peaked above 8%.

Despite these increases, Fed officials have expressed optimism that the worst of inflationary pressures may be behind us. However, the combination of rising prices in shelter and energy costs alongside concerns over the labor market will likely remain a significant part of their discussions.

Jobless Claims Suggest a Cooling Labor Market

The surge in jobless claims has added urgency to the Fed’s upcoming rate decision. Although the overall unemployment rate has remained low, the rise in claims could signal a shift in the labor market. The increase in initial claims to the highest level in nearly four years suggests that some employers may be starting to pull back on hiring. Although layoffs have been relatively subdued throughout the year, the sharp rise in jobless claims raises questions about the health of the labor market moving forward.

Moreover, continuing claims, which lag one week behind, remained unchanged at 1.94 million and have been hovering at levels not seen since late 2021. This suggests that more people are staying on unemployment benefits for longer periods, pointing to slower reemployment rates and potential weaknesses in the job market.

Market Sentiment and Fed Expectations

The markets are now fully pricing in a rate cut at the September meeting, and there is an increasing likelihood of further cuts in the following months. The latest economic data has reignited conversations about a potential series of rate reductions, especially as inflation remains within target levels, but labor market weakness adds complexity to the Fed’s outlook.

The Fed’s cautious approach to tightening monetary policy earlier this year is now being tested by rising inflation in certain sectors and increasing unemployment claims. Fed Chairman Jerome Powell’s decision to signal a series of rate cuts could be influenced by both these economic signals, aiming to foster more economic stability and address weakening job market conditions.

Looking Ahead: The Fed’s Dilemma

As the Federal Reserve approaches its September meeting, policymakers face a challenging economic puzzle. Inflation, although stable, is showing some signs of tick-up in key areas like housing and energy, while labor market data is pointing to potential cracks in the economy. The Fed must balance the dual mandate of controlling inflation and fostering a healthy labor market, which is increasingly difficult with the rise in unemployment claims.

With inflationary pressures continuing to be felt in certain sectors and jobless claims signaling a cooling job market, the path forward for the Fed is increasingly uncertain. However, markets are preparing for a more dovish Fed stance, with rate cuts likely in the near term to address these economic challenges.

Conclusion

The latest economic data showing a rise in inflation and a jump in jobless claims presents a complex backdrop for the Federal Reserve. While inflation remains manageable overall, certain sectors, such as shelter and energy, are seeing persistent price increases. Meanwhile, the rise in unemployment claims signals potential weaknesses in the labor market. The Fed’s upcoming decision to cut rates seems almost certain, but how the central bank navigates these mixed signals will determine its future course of action. The path forward for the housing market and the broader economy depends heavily on the Fed’s ability to balance these competing economic forces in the coming months. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses