Credit Quality Worries Spread Across Banking Sector as Lenders Tighten Standards

Concerns over credit quality are spreading across the U.S. banking sector, as high-profile defaults and warning signs in subprime lending raise fresh questions about the health of both large and regional financial institutions. The latest alarm came from JPMorgan Chase CEO Jamie Dimon, who expressed unease following recent bankruptcies by First Brands and Tricolor Holdings, a key player in the subprime auto loan market.

“My antenna goes up when things like that happen,” Dimon told analysts during an earnings call. “And I probably shouldn’t say this, but when you see one cockroach, there are probably more. Everyone should be forewarned on this.”

Dimon’s blunt remarks reflect a growing sentiment across the industry: that isolated signs of stress may be masking deeper credit vulnerabilities. The warning came amid a series of unsettling reports from regional banks that further fueled investor anxiety.

Regional Banks Report Losses and Fraud Concerns

Two mid-sized lenders, Zions Bancorp and Western Alliance Bancorp, both flagged credit issues in their latest quarterly updates. Zions disclosed a $50 million charge-off tied to “misrepresentations and defaults” in its loan portfolio, while Western Alliance said it was pursuing legal action against a borrower accused of fraudulent activity.

While neither bank suggested systemic risk, the timing of the reports has amplified market unease, especially given that these institutions serve as important credit providers for small businesses and real estate investors. The developments come as some banks begin tightening their underwriting standards an early sign that the long period of loose lending conditions may be ending.

Moody’s: Market Still Stable, But Warning Signs Emerging

Despite the headlines, credit rating agency Moody’s maintains that the broader financial system remains stable. Marc Pinto, Moody’s Head of Global Private Credit, told CNBC that while there are “pockets of weakness,” the overall health of U.S. banks and private credit markets remains sound.

“When we dig deeper here and look to see if there’s a turn in the credit cycle, which is effectively what the market seems to be focusing on, we can find no evidence,” Pinto said. “If we look at the asset quality numbers from the last several quarters, we’re seeing very little deterioration at all. That could change, but the fundamentals remain solid for now.”

Pinto acknowledged, however, that lending standards have loosened in some sectors, and that elevated consumer debt, rising insurance costs, and slowing job growth could challenge household finances in the coming months.

Ripple Effects on Housing and Mortgage Markets

The anxiety surrounding credit quality isn’t limited to the auto sector. Experts warn that tightening credit conditions could ripple through the housing market as well affecting both mortgage approvals and the broader pace of home sales.

“When credit quality starts to tighten, the effects ripple far beyond underwriting desks,” said Shilen Arrow, CEO and founder of Feesback. “It slows the pace of homebuying, shifts negotiating power, and forces both buyers and sellers to rethink what value and affordability really mean.”

Arrow noted that in markets such as New York and Los Angeles, where demand is constant even during downturns, tighter credit doesn’t eliminate activity it just reshapes it. “Deals still happen,” he said, “but the pool of qualified buyers shrinks, and competition becomes about liquidity and reliability rather than just price.”

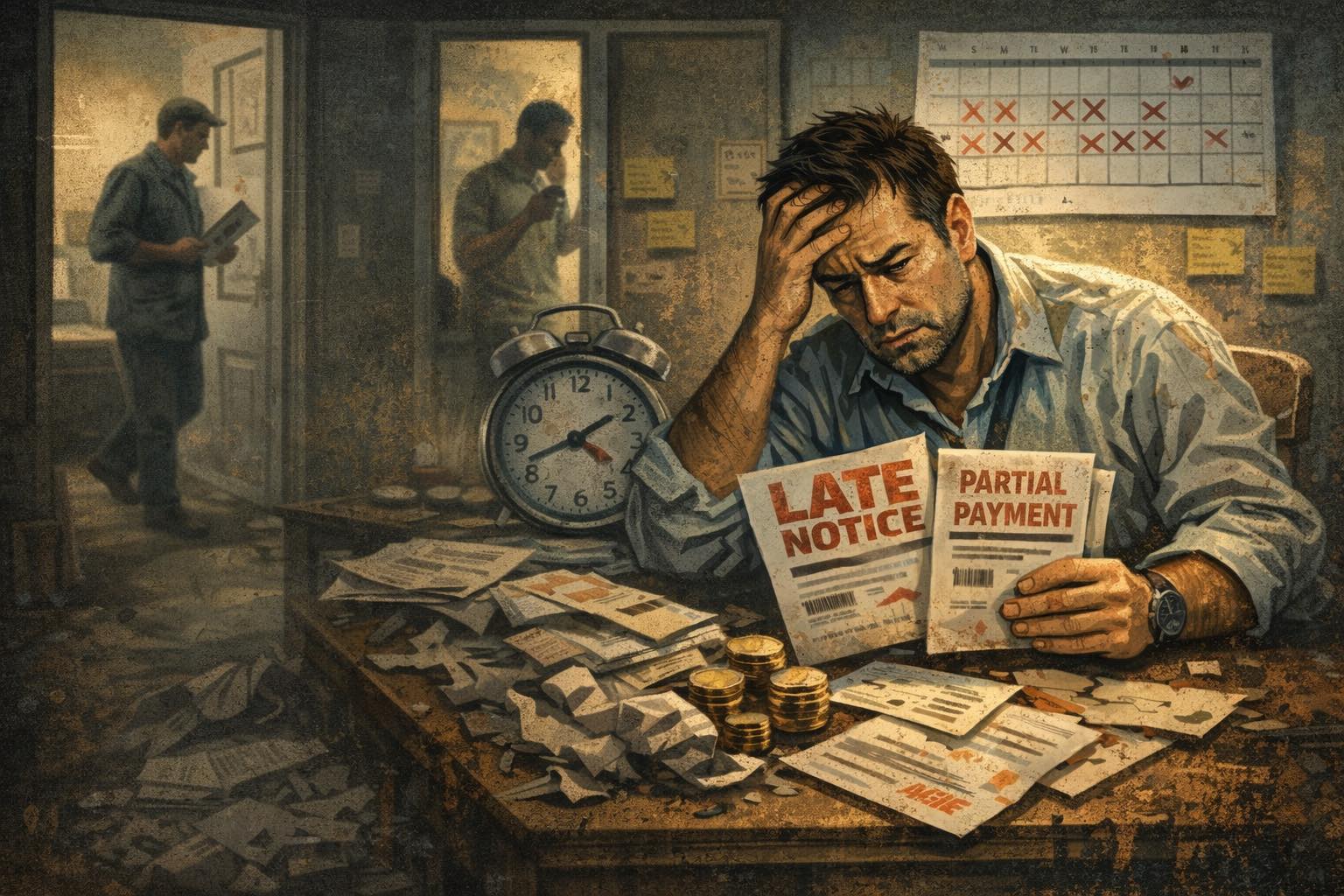

Mortgage Delinquencies Begin to Climb

Early warning signs are emerging in the housing sector as well. Amy Pierce, President of Bank Strategic Solutions, reported a gradual rise in mortgage delinquencies, driven by a combination of job losses, climbing insurance premiums, and higher escrow costs.

“Many buyers stretched themselves thin at the peak of the market in 2021 and 2022, expecting they could refinance at lower rates later,” Pierce explained. “But now, with refinancing opportunities limited and expenses like insurance surging, a lot of homeowners are struggling to keep up with payments. Many have little to no savings to handle unexpected costs.”

This trend, though not yet alarming, underscores how sensitive consumers have become to even modest financial shocks.

Risk Management Takes Center Stage

As economic uncertainty grows, experts say financial institutions must adopt a more holistic approach to risk management recognizing that financial, operational, and regulatory risks are increasingly intertwined.

“Today’s risk environment is changing faster than ever, and every type of risk is connected,” said Rafael DeLeon, Senior Vice President for Industry Engagement at Ncontracts and a Director at Main Street Bank in Fairfax, Virginia. “A credit issue, cyber incident, or regulatory shift can affect the whole organization overnight. The strongest institutions treat risk as a living, integrated discipline not a checklist.”

DeLeon emphasized that while the industry’s fundamentals remain solid, complacency could prove costly. “We’re not seeing a crisis,” he said, “but we’re certainly seeing stress points that deserve attention before they multiply.”

A Market Recalibration, Not a Collapse

Industry leaders agree that the current wave of concern shouldn’t be mistaken for a crisis, but rather a recalibration after years of easy money and historically low rates.

“Credit tightening isn’t just a constraint it’s a reset,” Arrow added. “It rewards efficiency, trust, and long-term relationships qualities that tend to endure well beyond any single credit cycle.”

Indeed, while defaults in sectors like subprime auto lending are drawing attention, analysts suggest they may serve as an early warning system rather than a systemic threat. The key question now is whether banks can adjust fast enough to manage emerging risks without choking off credit to households and small businesses.

Outlook: Cautious Optimism with Eyes on the Horizon

For now, the U.S. financial system remains on steady footing, supported by strong capital reserves, low unemployment, and generally healthy balance sheets. However, lenders are watching closely for any signs that rising delinquencies in consumer credit or real estate could spread.

“Every credit cycle ends eventually,” Dimon said earlier this year. “The question is not if, but when and how well-prepared we’ll be when it happens.”

With the economy slowing and rates remaining elevated, the coming quarters will test whether the banking sector’s current caution represents prudent foresight or the first tremors of a broader credit contraction. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses