Existing Home Sales Inch Higher but Stay Near Historic Lows

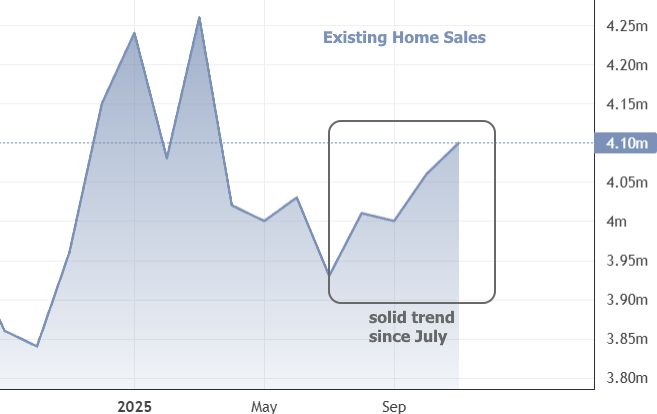

Existing-home sales registered another small improvement in October, rising 1.2% to an annual rate of 4.10 million, according to new data from the National Association of Realtors (NAR). The pace is now 1.7% higher than the same time last year, helped by easing mortgage rates and resilient demand despite the temporary government shutdown. But even with these modest gains, sales remain near some of the weakest levels seen in more than a decade.

NAR Chief Economist Lawrence Yun noted that lower borrowing costs gave buyers a bit more room to act. He also pointed out that regional conditions varied widely. The Northeast continued to struggle with tight inventory, while high prices in the West held many buyers back. In contrast, the Midwest and South were supported by better affordability and a growing number of homes for sale.

Yun added that slowing rent growth should help bring inflation down, opening the door for additional Federal Reserve rate cuts moves that could support more buyer activity through 2026.

Regional Breakdown: October 2025 Home Sales and Prices

| Region | Annual Sales Rate | MoM Change | Median Price | YoY Change |

|---|---|---|---|---|

| Northeast | 490,000 | 0.0% | $503,700 | +6.5% |

| Midwest | 990,000 | +5.3% | $319,500 | +4.6% |

| South | 1.86 million | +0.5% | $362,300 | +0.3% |

| West | 760,000 | -1.3% | $628,500 | +0.1% |

The regional data highlights ongoing affordability divides. Prices remain highest in the West, where even slight gains can push buyers to the sidelines. Meanwhile, the Midwest continues to stand out as one of the few regions where both supply and affordability are aligning to support stronger sales.

National Market Snapshot

- Total Housing Inventory: 1.52 million homes

(↓ 0.7% from September; ↑ 10.9% YoY) - Unsold Inventory Supply: 4.4 months

(↓ from 4.5 last month; ↑ from 4.1 a year ago) - Median Existing-Home Price: $415,200

(↑ 2.1% YoY; 28th straight annual increase) - Single-Family Median Price: $420,600

(↑ 2.2% YoY) - Condo/Co-op Median Price: $363,700

(↑ 0.9% YoY) - Typical Time on Market: 34 days

(↑ from 33 last month; ↑ from 29 a year ago) - First-Time Buyer Share: 32%

(↑ from 30% last month; ↑ from 27% YoY) - Cash Buyer Share: 29%

(↓ from 30% last month; ↑ from 27% YoY) - Investor Share: 16%

(↑ from 15% last month; ↓ from 17% YoY) - Distressed Sales: 2%

(unchanged) - Average 30-Year Mortgage Rate: 6.25%

(↓ from 6.35% in September)

A Market Finding Its Floor

The slight increase in October adds to the pattern seen since late summer: home sales are no longer steadily falling and instead appear to be settling into a firmer, though still low, range.

Lower mortgage rates, more fresh listings, and small affordability improvements have helped lift demand from the unusually weak levels of 2023. The question now is whether the market can move beyond stabilization and begin a true recovery.

Rates have dipped further in early November, which could support additional sales in the months ahead. But with prices still historically high and many homeowners locked into low-rate mortgages, the market may continue to take only small steps forward rather than seeing a quick rebound. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses