America’s Home Insurance Blind Spot Why Disaster Victims Still Falling Hundreds of Thousands Short

Home insurance is meant to be a safety net. It’s the promise homeowners rely on when disaster strikes—the assurance that they can rebuild and move forward. But across the United States, a growing number of families are learning a painful lesson: even after paying premiums for years, their insurance coverage isn’t enough to rebuild their homes.

This isn’t a rare mistake or a one-off oversight. New analysis shows underinsurance is a systemic problem that’s been building for decades, now exposed by climate-driven disasters like wildfires, floods, and hurricanes.

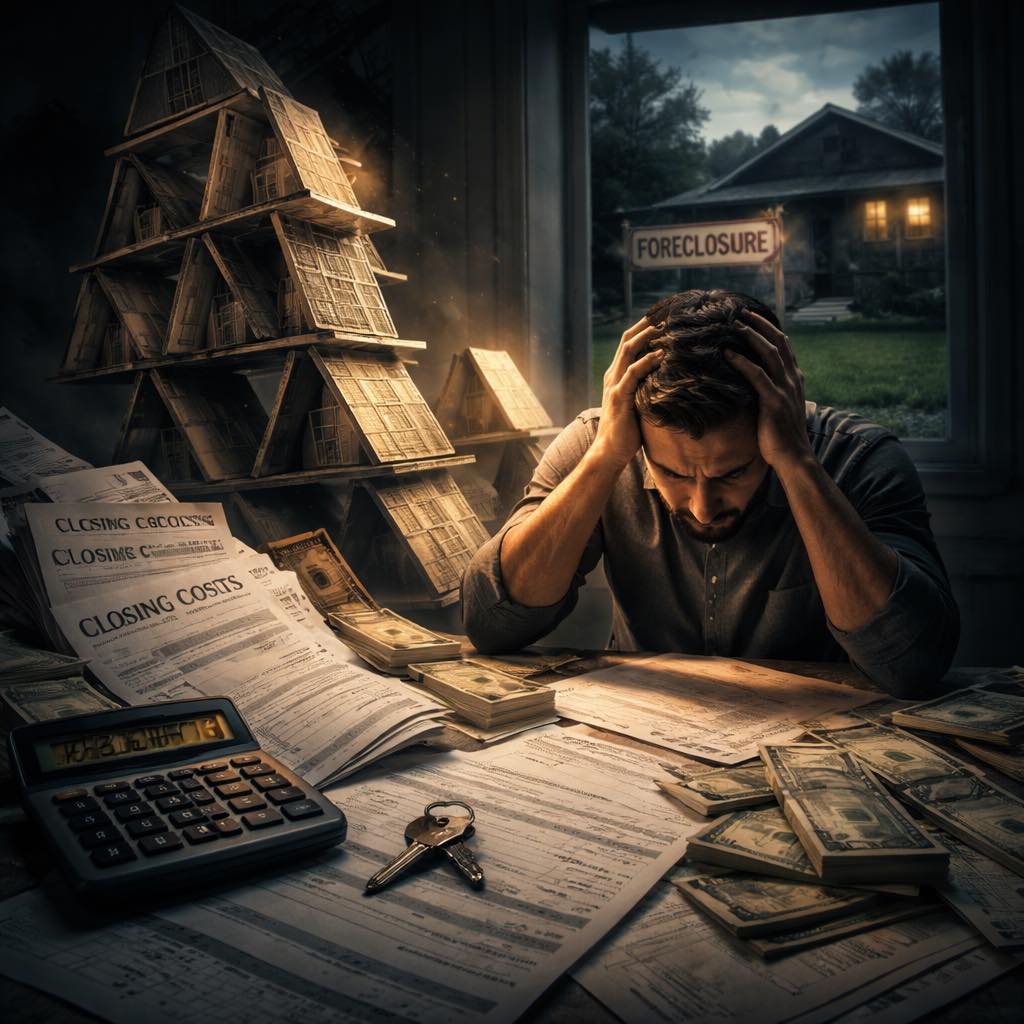

In places like Los Angeles, recent wildfires destroyed thousands of homes. Insurance checks arrived, but many homeowners quickly realized those payouts fell hundreds of thousands of dollars short. Rising labor costs, material shortages, stricter building codes, and post-disaster inflation pushed rebuilding expenses far beyond policy limits. Families were forced to drain savings, take on debt, or abandon rebuilding entirely.

Climate change didn’t create underinsurance—it revealed it. Since the 1990s, many insurers shifted away from guaranteed replacement cost coverage to capped policies designed to control risk and keep premiums competitive. Those caps worked when disasters were smaller and rarer. They don’t work in today’s environment of large-scale, repeated destruction.

The problem is compounded after disasters, when rebuilding doesn’t happen in a normal market. Contractors are scarce, supply chains tighten, and costs surge. Even policies that seemed adequate on paper can fall apart in reality.

Consumer advocates have warned about this for years. Surveys of wildfire survivors consistently show that roughly two-thirds were underinsured, often by six figures. Yet efforts to require stronger coverage face resistance, with regulators warning that forcing insurers to offer full replacement guarantees could push companies out of high-risk markets altogether.

For homeowners, the takeaway is uncomfortable but critical: policy limits matter more than premiums. Coverage needs to be reviewed regularly, stress-tested against real rebuilding costs, and adjusted as construction prices rise.

As climate risks grow, underinsurance is becoming a national housing issue—not just a personal one. Insurance that can’t rebuild a home isn’t true protection, and confronting that reality may define the next chapter of the U.S. housing market.

For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group. Contact us today for a tailored consultation, where our expert advice turns potential into profitable reality.

🔍 If you’re looking to get the best possible mortgage in the U.S. for Foreign Nationals and Americans, and want to run an auction between more than 3,000+ lenders, click here👇

Creative Financing – Nadlan Capital Financing for Foreign Nationals & Americans

Continue reading on our site:

#HomeInsurance

#HousingRisk

#ClimateImpact

#DisasterRecovery

#RealEstateStability

Responses