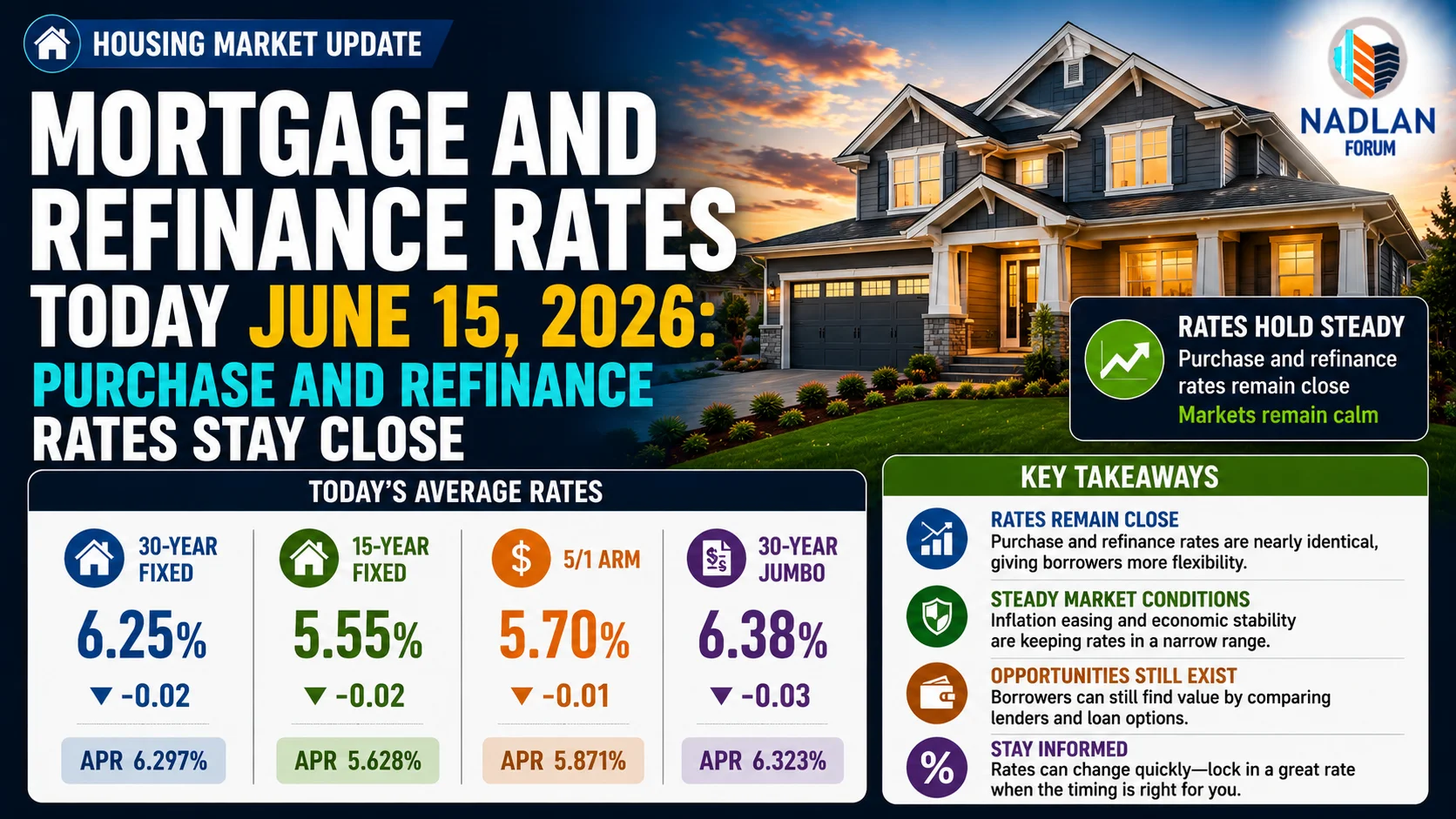

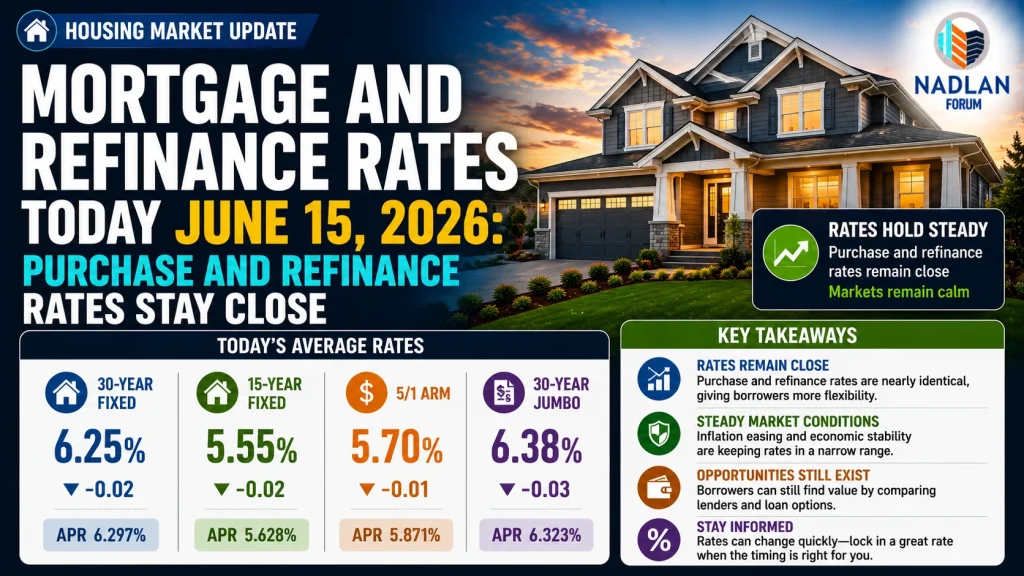

Mortgage and Refinance Rates Today: Rates Jump to Highest in 6 Months

Mortgage rates saw a sharp rise on March 28, 2026, reaching their highest point in nearly six months. The 30-year fixed mortgage rate jumped to 6.47%, up by 10 basis points from the previous day. This marks the highest level since late September. Meanwhile, the 15-year fixed rate also increased by five basis points, reaching 5.90%.

These changes are part of a broader trend that has seen mortgage rates fluctuate in recent months due to economic shifts and global events. While rates remain slightly lower than last year’s peaks, the recent surge has left many buyers and homeowners looking to secure loans with higher-than-expected costs.

Current Mortgage Rates Snapshot

Here’s a look at the latest national average mortgage rates:

- 30-year fixed: 6.47%

- 20-year fixed: 6.50%

- 15-year fixed: 5.90%

- 5/1 ARM: 6.71%

- 7/1 ARM: 6.56%

- 30-year VA: 5.99%

- 15-year VA: 5.55%

- 5/1 VA: 5.53%

These are rounded national averages; however, rates can vary by state, lender, and loan type.

Refinance Rates Also Climbing

Refinance rates are also on the rise, with the 30-year fixed rate at 6.60%, up from previous levels. Here’s a breakdown of the latest refinance rates:

- 30-year fixed refinance: 6.60%

- 20-year fixed refinance: 6.57%

- 15-year fixed refinance: 5.97%

- 5/1 ARM refinance: 6.87%

- 7/1 ARM refinance: 6.52%

- 30-year VA refinance: 5.92%

- 15-year VA refinance: 5.71%

- 5/1 VA refinance: 5.29%

Refinancing remains more expensive than buying a new home in many cases, though these rates can vary depending on the specific circumstances and loan term chosen.

What Does This Mean for Homebuyers?

For potential homebuyers, this increase in mortgage rates means higher monthly payments, especially for long-term loans like the 30-year fixed option. This could make homeownership less affordable, particularly in high-cost areas. However, it’s still important to note that rates are not as high as the peaks seen earlier in 2025.

The increase in rates, combined with higher home prices, could further slow housing demand. If rates continue to climb, it may push some buyers to reconsider their timelines or home purchasing plans.

Refinancing at Higher Rates: Is It Worth It?

For those considering refinancing, the recent rise in rates could affect your decision. If your current mortgage rate is lower than the new rates, it might not be worth refinancing at this time unless there are other factors—like consolidating debt or shortening the loan term that make refinancing beneficial.

If you currently have a higher rate or adjustable-rate mortgage, refinancing into a fixed-rate mortgage may still make sense to lock in stability, even at the higher rates. However, be mindful of the added cost.

Should You Buy or Refinance Now?

If you’re in the market for a new home or looking to refinance, the current environment presents both challenges and opportunities. While mortgage rates are climbing, they are still lower than the rates seen in previous years. If you’re prepared to move forward, locking in a mortgage rate now might still be a good option, especially if you are planning to stay in your home long-term.

However, buyers should be aware of the financial impact of higher rates on their monthly payments and overall loan affordability. Consider carefully how higher rates will affect your budget and future homeownership goals.

Adjustable-Rate Mortgages (ARMs) vs. Fixed Rates

For those exploring mortgage options, it’s important to weigh the pros and cons of adjustable-rate mortgages (ARMs) versus fixed-rate mortgages:

- Fixed-rate mortgages: These loans offer stability with a consistent interest rate for the entire term of the loan, making them ideal for those who want predictable payments. However, fixed rates are currently higher than the intro rates for ARMs.

- ARMs: These loans offer lower starting rates for a set period (e.g., 5/1 ARM), but the rates can increase after the introductory period. If you plan to sell or refinance before the rate adjusts, an ARM could save you money initially. However, there’s always the risk that rates may increase during the loan term.

What to Expect Going Forward

Mortgage rates are expected to continue fluctuating, influenced by various factors, including inflation, economic growth, and global events. In the coming months, market conditions could lead to further increases or potential stabilization in rates.

For buyers and homeowners, staying informed about the market and considering the long-term implications of your loan choices will be crucial. While rates may still be lower than past highs, any upward movement in rates could have a substantial impact on affordability.

In summary, the recent rise in mortgage rates signals a potential shift in the housing market, with higher borrowing costs affecting both homebuyers and those looking to refinance. As always, it’s essential to shop around and compare offers to find the best rate available for your financial situation. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses