FHFA Q3 Report Highlights Foreclosure Prevention Progress and Shifting Refinance Trends

The Federal Housing Finance Agency’s latest quarterly analysis offers a detailed look at how the housing finance system performed in the third quarter of 2025, with a focus on foreclosure prevention, loan performance, and refinance activity. Overall, the data points to steady borrower support, modest stress in delinquency metrics, and refinance volumes reacting quickly to interest rate changes.

Foreclosure Prevention Efforts Remain Strong

According to the Q3 report, the Enterprises Fannie Mae and Freddie Mac completed 50,096 foreclosure prevention actions during the third quarter alone. Since the start of conservatorships in September 2008, total prevention efforts now exceed 7.26 million.

Of those actions, more than 6.55 million have helped homeowners stay in their homes. This includes roughly 2.81 million permanent loan modifications, highlighting the continued use of long-term solutions for borrowers facing hardship.

Forbearance and Loan Adjustments

Forbearance activity edged higher in Q3. New forbearance plans increased from 22,119 in Q2 to 23,674 in Q3. By the end of September, about 33,360 loans remained in forbearance. While that represents just 0.11% of all serviced loans, it accounts for 6.2% of loans that were past due, showing forbearance is still a key tool for struggling borrowers.

During the quarter, forbearance-based solutions made up 65% of all loan modifications, while 35% were term extensions only. In addition, 238 short sales and deeds-in-lieu were completed, bringing the long-term total since 2008 to more than 706,000.

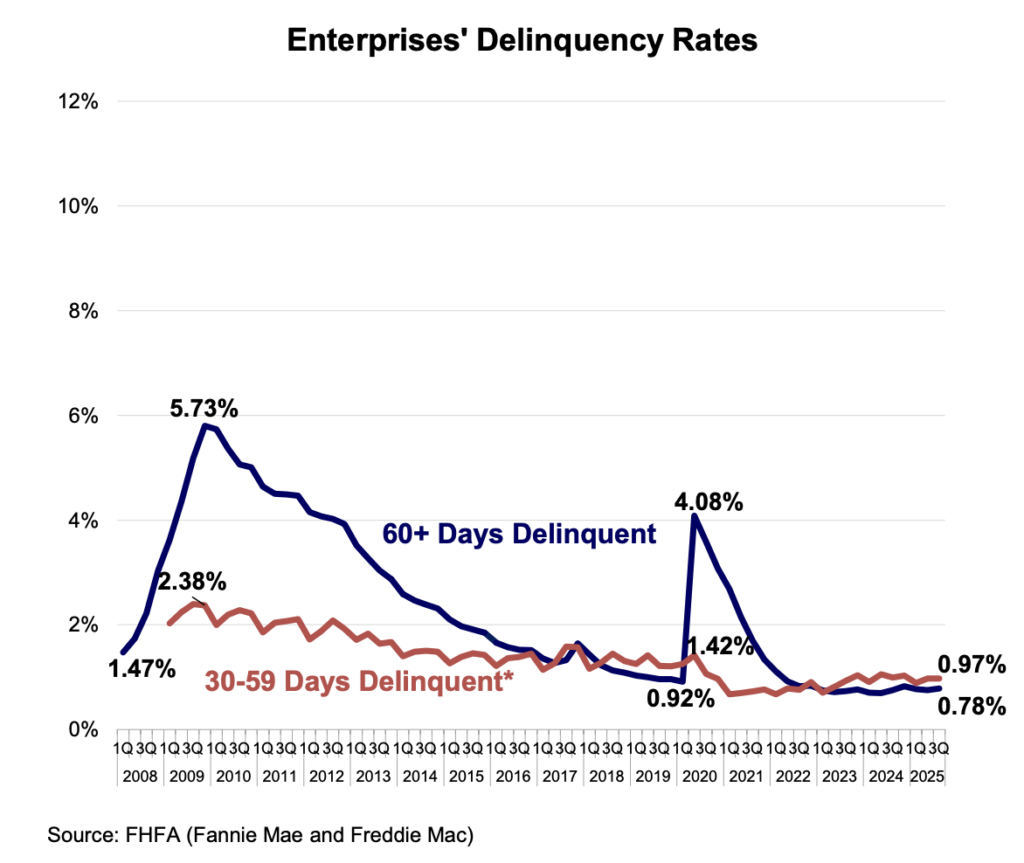

Delinquency Rates Tick Up, But Stay Below Industry Levels

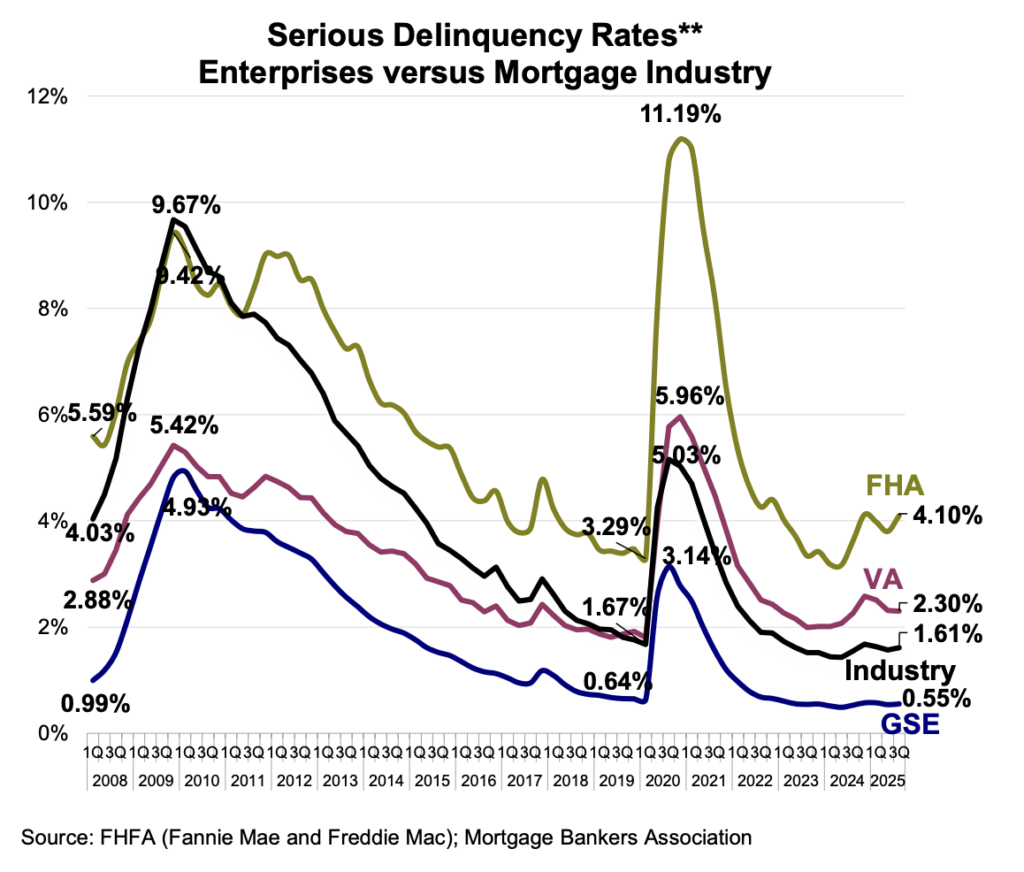

Loan performance weakened slightly in Q3, though Enterprise loans continued to outperform the broader market. The 60+ day delinquency rate rose from 0.76% to 0.78%, while the serious delinquency rate (90+ days) increased to 0.55%.

Even with this uptick, Enterprise delinquency rates remain far lower than the industry average. By comparison, serious delinquencies stood at 1.61% for all loans, **2.30% for Veterans Affairs loans, and **4.10% for Federal Housing Administration loans.

Foreclosure activity showed signs of rising stress. Third-party and foreclosure sales increased 4.7% to 3,344, while foreclosure starts jumped to 24,802 during the quarter.

Refinance Activity Responds to Rate Changes

Refinance trends reflected the volatility in mortgage rates throughout the summer. September saw a rebound in refinance volume, but overall third-quarter activity remained lower than Q2. Higher mortgage rates in June and July weighed on demand before easing conditions later in the quarter.

The average 30-year fixed mortgage rate fell from 6.59% in August to 6.35% in September, helping spark renewed interest. At the same time, cash-out refinances became less common. After making up as much as 82% of refinance activity over the prior three years, cash-out transactions declined from 63% in August to 55% in September, signaling a shift toward rate-and-term refinances.

What the Q3 Data Signals

The Q3 findings show a housing finance system that is still stable but adjusting to higher rates and slower economic momentum. Foreclosure prevention tools remain widely used, delinquency levels are rising only modestly, and refinance demand continues to move closely with interest rates.

As 2026 approaches, the data suggests policymakers and lenders will remain focused on borrower assistance, risk management, and monitoring how affordability and rate trends shape homeowner behavior in the months ahead. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses