First Investment Property: Your Complete Guide for 2026

Purchasing your first investment property represents a significant milestone in building long-term wealth through real estate. Unlike buying a primary residence, investment properties require a different mindset focused on cash flow, appreciation potential, and strategic financial planning. The real estate market in 2026 continues to offer opportunities for new investors who approach their purchase with thorough research, realistic expectations, and a clear understanding of the commitment involved. This comprehensive guide will walk you through the essential steps and considerations to make your first property investment successful.

Understanding Investment Property Fundamentals

Investment properties generate income through rental payments or appreciation over time. The key difference between a personal residence and an investment property lies in the financial objectives and tax implications.

Primary types of investment properties include:

- Single-family homes

- Multi-family units (duplexes, triplexes, fourplexes)

- Condominiums and townhouses

- Commercial properties

- Vacation rentals

Your first investment property should align with your financial capacity, management capabilities, and market knowledge. Single-family homes often serve as the most accessible entry point for new investors because they require less capital and management complexity compared to larger multi-unit buildings.

Evaluating Your Financial Readiness

Before searching for properties, assess your financial position honestly. Investment properties typically require larger down payments than primary residences, with most lenders expecting 20% to 25% of the purchase price upfront.

| Financial Requirement | Primary Residence | Investment Property |

|---|---|---|

| Minimum Down Payment | 3% to 5% | 15% to 25% |

| Credit Score (Typical) | 620+ | 640+ |

| Debt-to-Income Ratio | Up to 43% | Up to 36% |

| Interest Rate | Lower | 0.5% to 0.75% higher |

Planning for a larger down payment is crucial for securing favorable financing terms on your investment property. Additionally, maintain reserves covering at least six months of mortgage payments, property taxes, insurance, and maintenance costs.

Selecting the Right Market and Location

Location determines the success or failure of your first investment property more than any other single factor. A property in a growing market with strong employment, population growth, and infrastructure development will outperform a cheaper property in a declining area.

Key Market Indicators to Research

Start by analyzing metropolitan areas with diverse economies and consistent job growth. Research local market trends including median home prices, rental rates, vacancy percentages, and projected development plans.

Essential location factors include:

- Employment opportunities and major employers

- School district quality and ratings

- Crime statistics and neighborhood safety

- Public transportation and accessibility

- Planned infrastructure improvements

- Proximity to amenities (shopping, healthcare, entertainment)

The Chase Bank investment property guide emphasizes that successful investors spend considerable time understanding local market dynamics before making purchase decisions. Consider starting in markets you already know or where you can easily visit and manage the property.

Neighborhood-Level Analysis

Once you identify promising markets, drill down to specific neighborhoods. Visit at different times of day and days of the week. Talk to local property managers, real estate agents, and current landlords to understand rental demand and tenant quality.

Properties near universities, hospitals, or major employment centers often maintain consistent rental demand. However, these areas may also command premium purchase prices, affecting your return on investment calculations.

Calculating Investment Returns

Understanding the numbers separates successful real estate investors from those who struggle. Your first investment property should generate positive cash flow or have clear appreciation potential that justifies temporary negative cash flow.

Essential Financial Metrics

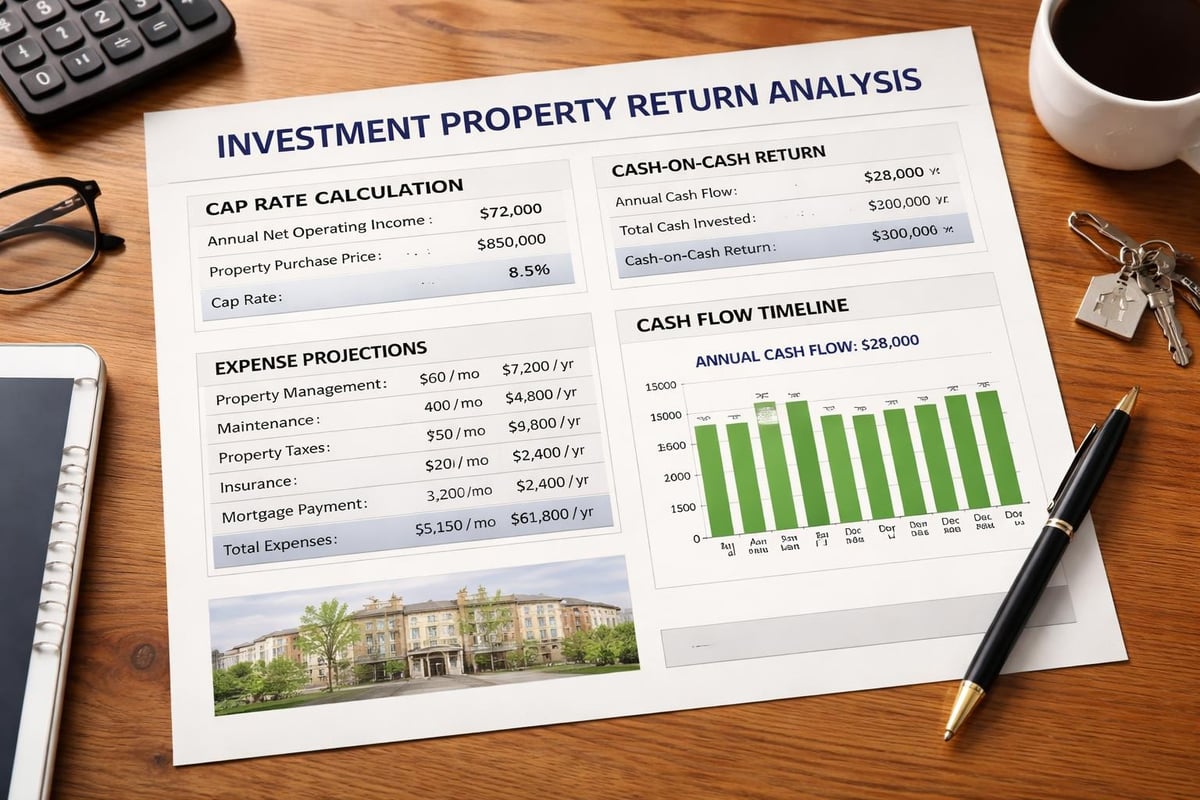

Cap Rate (Capitalization Rate) measures the property’s net operating income against its purchase price. Calculate it by dividing annual net operating income by the property’s current market value. A cap rate between 5% and 10% is typical for residential investment properties, though this varies significantly by market.

Cash-on-Cash Return examines the annual pre-tax cash flow relative to the total cash invested. This metric helps you understand the actual return on your down payment and closing costs.

Gross Rent Multiplier provides a quick screening tool by dividing the property price by gross annual rental income. Lower numbers generally indicate better investment opportunities, though this varies by market.

| Metric | Formula | Good Range |

|---|---|---|

| Cap Rate | NOI ÷ Property Value | 5% to 10% |

| Cash-on-Cash Return | Annual Cash Flow ÷ Total Cash Invested | 8% to 12% |

| Gross Rent Multiplier | Property Price ÷ Gross Annual Rent | 4 to 7 |

When evaluating potential returns, factor in property taxes, insurance, maintenance reserves, property management fees, and vacancy periods. Conservative estimates protect you from unexpected financial stress.

Financing Your First Investment Property

Securing financing for an investment property differs from obtaining a mortgage for a primary residence. Lenders view investment properties as higher risk, resulting in stricter qualification requirements and higher interest rates.

Conventional Financing Options

Most investors use conventional mortgages through traditional banks or mortgage lenders. These loans typically require 20% to 25% down and carry interest rates approximately half a percentage point higher than primary residence mortgages.

Alternative financing methods include:

- Portfolio loans from smaller banks that keep loans in-house rather than selling them

- Hard money loans for short-term financing (typically used for fix-and-flip projects)

- Private money from individual investors or family members

- Home equity from your primary residence

- Partnerships where you combine resources with other investors

Fixed-rate mortgages provide stability and predictable payments, making them ideal for your first investment property. While adjustable-rate mortgages offer lower initial rates, they introduce uncertainty that can complicate cash flow planning.

Improving Your Financing Position

Prepare documentation including tax returns, W-2 forms, bank statements, and proof of existing assets. Lenders scrutinize investment property applications more carefully than primary residence loans.

Consider paying down existing debt to improve your debt-to-income ratio. Each percentage point improvement in your credit score can translate to better interest rates and terms, saving thousands over the loan’s life.

Property Inspection and Due Diligence

Never skip the inspection process on your first investment property. Professional inspections reveal costly issues that aren’t visible during casual viewings.

Critical Inspection Areas

Hire qualified inspectors to evaluate the foundation, roof, electrical systems, plumbing, HVAC, and structural elements. Budget at least $400 to $600 for comprehensive inspections, though this varies by property size and location.

Request documentation for recent repairs, renovations, and ongoing maintenance issues. Review the property’s history including past insurance claims, code violations, and zoning compliance.

Due diligence checklist:

- Professional property inspection

- Title search and title insurance

- Zoning verification

- Review of current leases (if occupied)

- Comparable sales analysis

- Rental market analysis

- Environmental assessments (if needed)

- Survey confirmation of property boundaries

The first-time investor tips from Money Crashers emphasize patience during the due diligence phase. Taking time to thoroughly investigate prevents expensive surprises after closing.

Property Management Considerations

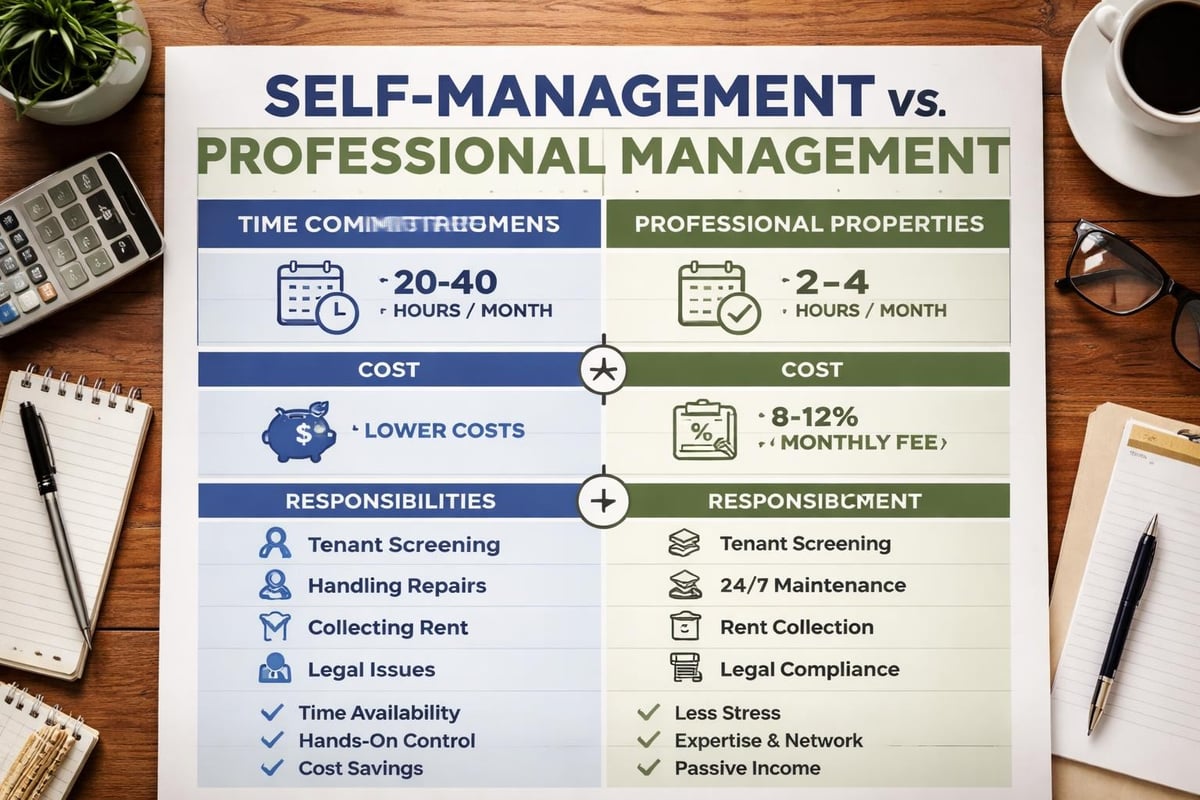

Decide early whether you’ll self-manage your first investment property or hire professional management. This decision significantly impacts your time commitment and cash flow.

Self-Management vs. Professional Management

Self-management saves the typical 8% to 10% management fee but requires time for tenant screening, rent collection, maintenance coordination, and legal compliance. First-time investors often underestimate the time commitment involved in property management.

| Management Type | Pros | Cons |

|---|---|---|

| Self-Management | No management fees, direct control, faster decisions | Time-intensive, learning curve, emotional involvement |

| Professional Management | Expertise, time savings, tenant screening, legal compliance | 8% to 10% fees, less direct control |

Professional property managers handle advertising vacancies, screening tenants, collecting rent, coordinating repairs, and ensuring compliance with landlord-tenant laws. Their expertise often justifies the cost, especially for out-of-state properties or investors with limited time.

Tax Implications and Benefits

Investment properties offer significant tax advantages that improve overall returns. Understanding these benefits helps you maximize the financial potential of your first investment property.

Key Tax Deductions

Mortgage interest represents your largest deductible expense, especially in the early loan years when interest comprises most of your payment. Property taxes, insurance premiums, and operating expenses including repairs, maintenance, property management fees, and utilities all reduce taxable income.

Depreciation allows you to deduct a portion of the property’s value annually, even though the property may actually appreciate. Residential investment properties depreciate over 27.5 years under current tax law.

Work with a tax professional familiar with real estate investments to ensure you capture all eligible deductions. The Mashvisor guide to buying investment property highlights how understanding real estate taxes impacts your overall investment strategy.

1031 Exchanges

While perhaps not immediately relevant to your first investment property, understanding 1031 exchanges helps with long-term planning. These exchanges allow you to defer capital gains taxes when selling one investment property and purchasing another, enabling wealth building through strategic property upgrades over time.

Risk Mitigation Strategies

Every investment carries risks, and real estate is no exception. Successful investors identify potential problems and implement strategies to minimize their impact.

Common Investment Property Risks

Vacancy periods reduce cash flow and still require you to cover mortgage payments and expenses. Maintain adequate reserves and select properties in markets with strong rental demand to minimize vacancy duration.

Unexpected repairs can devastate your budget if you’re unprepared. Set aside at least 1% of the property value annually for maintenance and repairs, though older properties may require more.

Problem tenants cause financial and emotional stress. Implement thorough screening processes checking credit history, employment verification, rental history, and criminal background. Never skip screening to fill a vacancy quickly.

Market downturns affect property values and rental rates. Conservative financing with adequate equity cushion protects you during market corrections. Avoid over-leveraging your first investment property, even when lenders approve larger loan amounts.

Building Your Investment Team

Real estate investing succeeds through teamwork. Surround yourself with qualified professionals who understand investment properties and can guide you through challenges.

Essential Team Members

Real estate agents familiar with investment properties understand the metrics investors care about and can identify opportunities others miss. Choose agents who work with investors regularly rather than those focused primarily on primary residences.

Lenders experienced with investment property financing provide smoother transactions and may offer better terms than generalist mortgage brokers. Establish relationships before you need financing.

Accountants specializing in real estate understand the tax implications and can structure your investment for maximum tax efficiency. Their guidance often saves more than their fees cost.

Attorneys review contracts, handle closings, and ensure compliance with landlord-tenant laws. Real estate law varies significantly by state, making local expertise valuable.

Property inspectors, contractors, and handymen keep your property maintained and help evaluate potential purchases. Build these relationships early so you have trusted resources when needed.

The community and resources available through Nadlan Forum connect investors with experienced professionals and fellow investors who share knowledge and strategies for successful property investment.

Making Your First Offer

Once you identify a suitable property and complete preliminary analysis, structure an offer that protects your interests while remaining competitive in the market.

Offer Components

Include appropriate contingencies in your offer including financing approval, satisfactory inspection results, and clear title verification. These contingencies protect your earnest money deposit if issues arise during due diligence.

Research comparable sales to determine fair market value. The DoorLoop tips for first-time investors emphasize patience in evaluating opportunities rather than rushing into deals based on emotion or fear of missing out.

Consider the seller’s situation when structuring your offer. Flexible closing dates or accommodating specific seller needs can make your offer more attractive without increasing your purchase price.

Negotiation factors beyond price:

- Closing timeline flexibility

- Seller covering closing costs or repairs

- Including appliances or furnishings

- Assumption of existing leases and deposits

- Home warranty coverage

Remember that every dollar you save on purchase price increases your return on investment. However, don’t let negotiations derail a good deal over minor differences.

Long-Term Investment Planning

Your first investment property serves as the foundation for potential portfolio growth. Think beyond the immediate purchase to how this property fits into your broader financial goals.

Portfolio Growth Strategies

Some investors focus on acquiring multiple properties quickly, while others prefer to stabilize one property before adding another. Neither approach is inherently superior; choose the strategy aligned with your resources, risk tolerance, and objectives.

Cash flow from your first investment property can fund down payments on subsequent properties. Alternatively, appreciation equity allows you to refinance and extract capital for additional investments while maintaining the original property’s income stream.

Track all income and expenses meticulously from day one. This habit provides clear financial pictures for tax purposes, refinancing applications, and future purchase decisions. Property management software simplifies tracking and generates reports demonstrating your investment’s performance.

Common Mistakes to Avoid

Learning from others’ mistakes costs less than making them yourself. New investors frequently encounter predictable pitfalls that damage returns or create unnecessary stress.

Typical New Investor Errors

Underestimating expenses leads to negative cash flow surprises. Budget conservatively, including management fees even if you plan to self-manage initially. Circumstances change, and having room in your numbers for professional management provides flexibility.

Emotional attachment to properties clouds judgment. Your first investment property is a business asset, not your home. Make decisions based on numbers and logic rather than personal preferences about aesthetics or features.

Overleveraging maximizes risk and limits flexibility when unexpected situations arise. Maintaining equity cushion and cash reserves protects your investment during market downturns or extended vacancies.

Skipping professional inspections to save a few hundred dollars potentially costs thousands in unexpected repairs. Always inspect thoroughly before purchasing.

Ignoring local market research and buying based solely on price or online analysis without understanding local dynamics leads to poor investment decisions. Visit markets personally and talk to local professionals before committing capital.

Building wealth through real estate begins with purchasing your first investment property using sound strategies, thorough research, and conservative financial planning. Success requires patience, realistic expectations, and willingness to learn continuously as you navigate the challenges and opportunities of property investment. Whether you’re seeking cash flow, appreciation, or portfolio diversification, Nadlan Forum provides the resources, community support, and expert guidance to help you make informed decisions and achieve your real estate investment goals in 2026 and beyond.

Responses