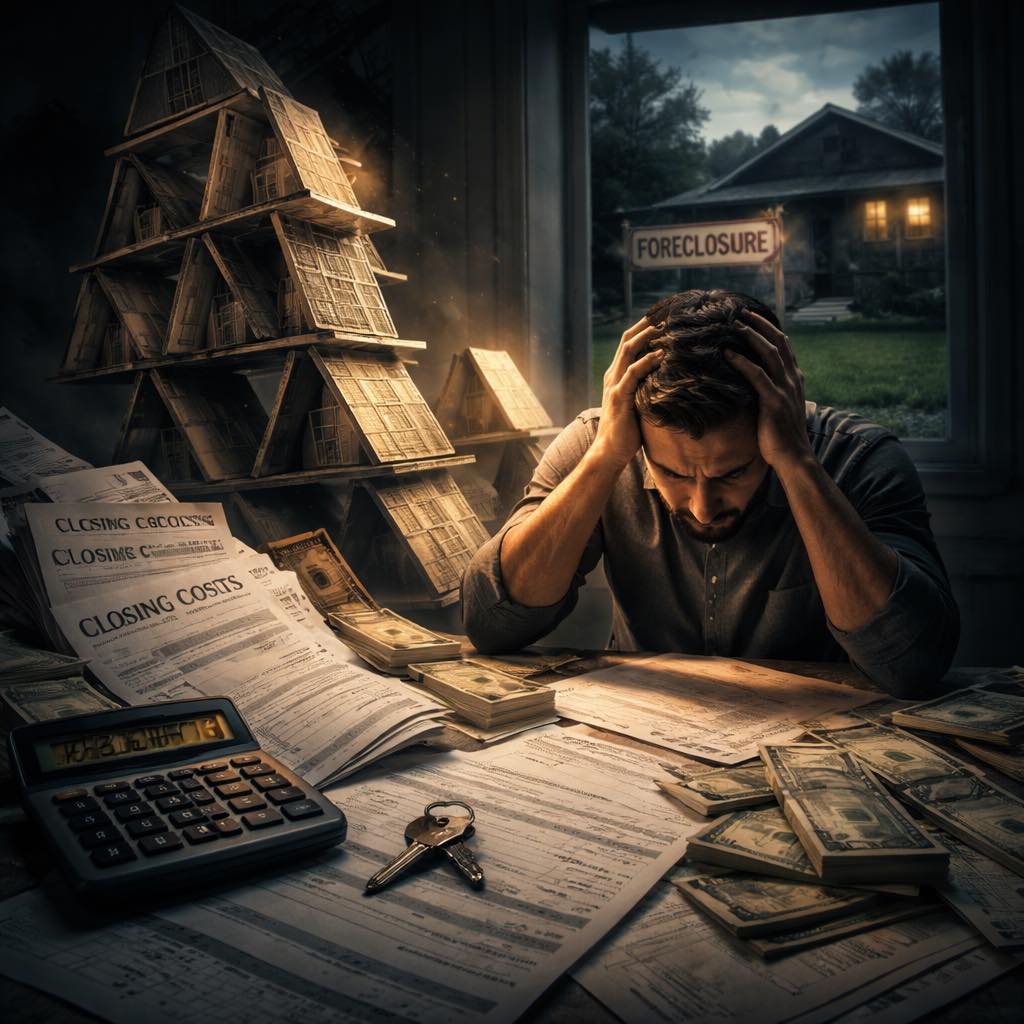

Cash-Out Refinance Illusion

The illusion that quietly wipes out investors’ profits

You think you pulled cash out of your property and made a smart move.

In reality, that’s often the moment you started losing.

Most investors look at a cash-out refinance as a way to extract equity, keep the asset, and move on to the next deal. Sounds perfect—but this is exactly where the illusion begins.

Because what no one tells you is this:

You’re not pulling out profit—you’re increasing risk.

And there’s another layer most people don’t even calculate:

The money you “take out” isn’t actually what you have available.

From that amount, you still need to subtract:

- Loan origination costs

- Points

- Bank fees

- Appraisal

- Title and closing costs

- Sometimes prepayment penalties on the existing loan

So in reality, the net cash you receive is significantly lower—but your new debt is fully increased.

What’s really happening behind the scenes?

- Your loan balance increases

- Your monthly payment jumps

- Your interest rate is often higher

- Your DSCR (Debt Service Coverage Ratio) gets weaker

- The property shifts from stable to fragile

And then it only takes:

- One tenant leaving

- One major repair

- A spike in insurance

- An increase in property taxes

…and suddenly you’re not a smart investor anymore—you’re feeding the property out of your own pocket.

The critical point most investors miss:

Before the refinance—you had a margin of safety.

After the refinance—you’re operating on the edge.

And it doesn’t stop there.

Often, investors take that extracted cash and roll it into another leveraged deal.

Now you’ve created a domino effect:

- One property weakens → the next depends on it

- One cash flow gets hit → the whole system shakes

- One small market shift → everything starts to unravel

This isn’t theory.

This is exactly how real estate portfolios collapse.

Not from one bad deal—

but from leverage that looked smart on paper and failed in reality.

So how do you know you’re inside the illusion?

- Your DSCR is borderline after the refinance

- You don’t have real reserves

- You depend on full occupancy

- You’re relying on rent increases to make the numbers work

That’s not a strong position.

That’s a risky one.

And the most dangerous part?

It looks great on Excel.

It feels like progress.

And that’s exactly what traps people.

Advanced investors don’t ask:

“How much cash can I pull out?”

They ask:

“How much stress can this property absorb and still remain stable?”

Because in real estate, it’s not the strong deals that build you—

it’s the deals that survive bad times.

If you’re not deeply analyzing the true impact of a refinance—including all costs and cash flow effects—you’re not leveraging.

You’re gambling.

Responses