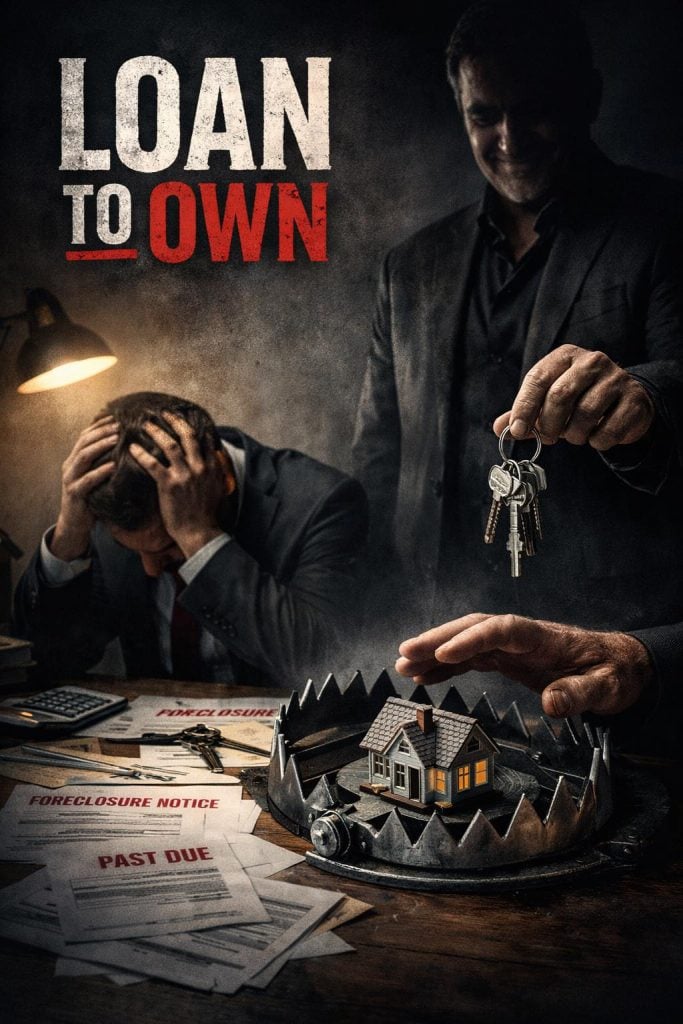

Loan To Own

How Smart Players Don’t Buy Properties—They Just Wait for You to Make a Bad Decision

Most investors think they’re buying real estate. In reality, many times they are simply playing a role in someone else’s game. Loan to Own is a strategy where they give you financing, knowing full well it will be difficult for you to meet the terms. Not by accident, not by mistake, but intentionally.

The terms look “reasonable,” the deal closes, everyone is happy, and you feel like you’ve secured financing that you wouldn’t have gotten from the bank. Then the clock starts ticking: the interest rate pressures you, the cash flow isn’t enough, there are delays, there are overruns, and suddenly you realize you’re chasing the deal instead of managing it.

At this stage, the other party is no longer in a hurry; on the contrary, they are waiting. Because for them, the real asset is not the interest you’re paying, but the ownership they will take when you default. And this happens more often than people realize.

Funds, private lenders, and big players know exactly where to put their money to control the outcome. They don’t need you to succeed, they just need you to survive long enough so that they are in a position to legally, cleanly, and sometimes even “with your consent,” take the property from you.

To be precise, not every tough loan is a trap, and not every lender wants to take over your property. But if you’ve built a deal that doesn’t have a real cushion, doesn’t have a clear exit plan, and you don’t have control over alternative sources of financing, then you’re not an investor—you’re a target.

The question every investor should ask themselves before signing is simple: If things don’t go according to plan, who remains in control? Because in Loan to Own deals, the one holding the debt controls your future.

Responses