Paying the Price: How High Mortgage Rates Are Reshaping Home Buying

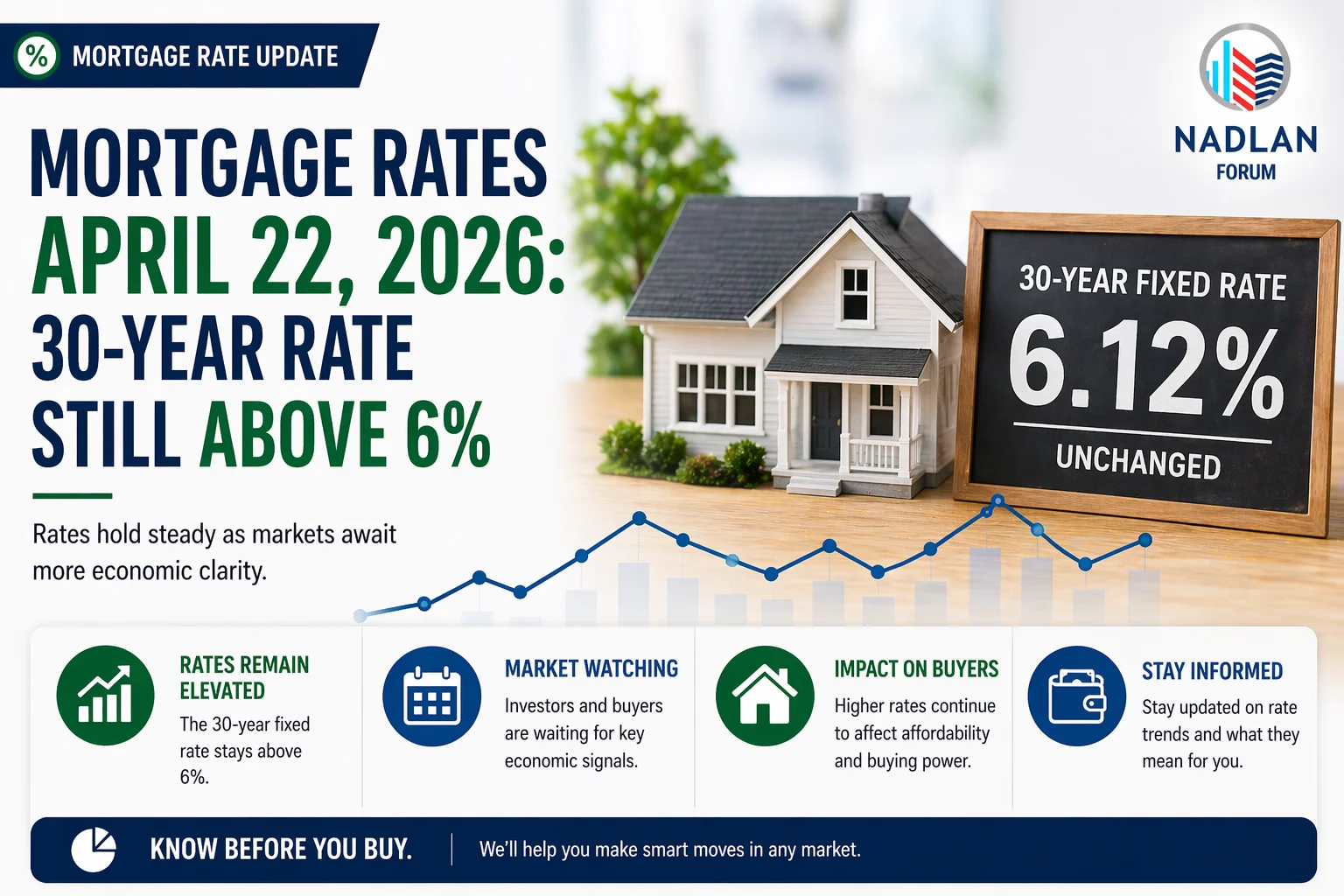

With mortgage rates stubbornly sitting above 6.5%, prospective homebuyers are feeling the pinch more than ever. Affordability challenges in the current housing market are stretching household budgets to their limits, leaving many Americans forced to reconsider when and where they can purchase a home.

New findings from Realtor.com’s August 2025 Buying Power Report shed light on just how constrained buyers have become. According to the analysis, only 28% of homes currently listed are priced within reach of the typical U.S. household. The maximum affordable home price for a median-income buyer has dropped to $298,000 a steep decline from $325,000 in 2019.

Even as wages rise, elevated interest rates have chipped away at real purchasing power, said Danielle Hale, Chief Economist at Realtor.com. This reality is pushing many buyers to adjust expectations, whether that means choosing smaller homes, relocating to more affordable areas, or delaying homeownership altogether.

The Numbers Behind the Strain

While median wages have increased by roughly 15.7% over the past several years, the cost of borrowing has outpaced income growth. A $320,000 fixed-rate mortgage in July 2025 carries a monthly payment nearly $600 higher than it would have at 2019’s average rate translating into an extra $7,200 annually for the typical buyer. In 2019, a $320,000 loan could cover the full median-priced home in many markets. Today, that same loan would require a nearly 28% down payment just to purchase the median listing, which now sits around $439,450.

Regions Feeling the Pinch the Most

Certain metro areas have been hit harder than others. Milwaukee, Wisconsin; Houston, Texas; Baltimore, Maryland; New York City; and Kansas City, Missouri have all seen dramatic drops in what the median earner can afford. Milwaukee experienced the steepest decline, with maximum affordable home prices falling from $314,000 to $281,000 a 10.5% drop equivalent to $33,000.

Even in metros with significant affordability declines, some markets maintain a relative share of homes within reach. New York City remains an exception, where only 13.1% of listings were affordable to a median-income household in July, highlighting the extreme imbalance between income and housing costs in the nation’s largest city.

Where Buying Power Has Improved

On the flip side, a handful of metros have seen modest gains in buying power since 2019. Cleveland, Ohio, leads this group. Strong local wage growth boosted the maximum affordable home price from $249,000 to $260,000 (+4.4%). Notably, half of Cleveland’s housing inventory in July remained within reach of median-earning households.

Other areas that have benefited from rising wages include former pandemic boomtowns such as Phoenix, Arizona; Tampa, Florida; and Austin, Texas. However, even in these regions, rapid home price growth has outstripped income gains, leaving many buyers still struggling to find truly affordable options.

The Consequences of Shrinking Buying Power

Dwindling buying power is reshaping the way Americans approach homeownership. As affordability declines, competition for lower-priced homes has intensified, leaving some buyers resorting to renting or postponing purchases altogether. Younger households, in particular, who often lack existing equity, are disproportionately affected.

Sellers are also feeling the impact. Homes may sit longer on the market, and pricing strategies must adapt to align with what buyers can realistically afford. The interplay between mortgage rates, wages, and housing supply will likely dictate market trends in the months ahead.

What Could Restore Balance

Experts say that restoring lost buying power will require a multi-pronged approach. Slightly lower mortgage rates, continued wage growth, and an increase in affordable housing stock—particularly in high-demand regions would all help alleviate pressure on buyers. Until then, navigating the current market demands flexibility, creativity, and careful financial planning. Buyers may need to broaden their search areas, consider smaller properties, or prioritize long-term affordability over short-term wish lists.

Ultimately, the current market underscores a simple truth: even modest changes in mortgage rates can have an outsized impact on Americans’ ability to purchase homes. For now, affordability remains the defining challenge for buyers across the country. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses