What Wealthy Parents Should Know Before Passing Real Estate to Their Children

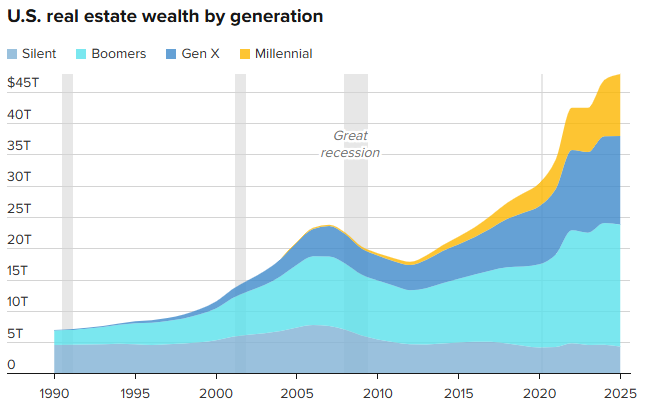

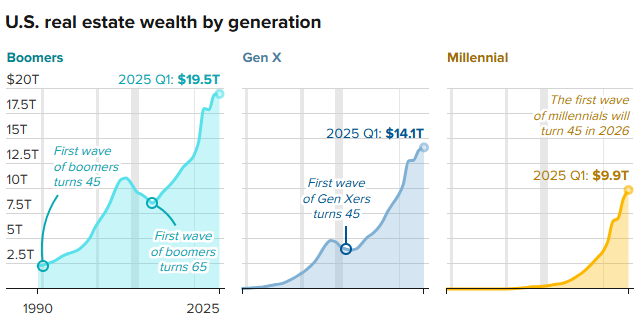

The upcoming intergenerational wealth transfer is not just about bank accounts and stocks it’s also about property. Baby boomers and the silent generation collectively hold nearly $25 trillion in real estate, ranging from city apartments to luxury vacation homes. But as families prepare to pass these assets down, the process can be fraught with emotional tension, financial pitfalls, and logistical headaches.

Inheriting a family home or vacation property can sometimes create disputes over usage, decor, and upkeep, even in otherwise close-knit families. Lawyers and estate planners for affluent clients say there are proactive ways to reduce conflict while also managing taxes and protecting assets.

“Families may have strong attachments to vacation homes, but inevitably, disagreements arise,” says Jere Doyle, senior estate planning strategist at BNY Wealth. “Some children want to keep the property, others don’t. Planning ahead is key to avoiding unnecessary fights.”

Here’s a detailed guide to successfully passing down real estate to the next generation.

1. Use Wills and Trusts to Minimize Taxes

Transferring real estate before death can trigger significant capital gains taxes. If parents gift a property during their lifetime, children inherit the original purchase price as their tax basis. This can create a large tax bill if they decide to sell.

“Elisa Rizzo from J.P. Morgan Private Bank often sees families reluctant to part with second homes, even as they downsize their primary residence,” Doyle notes. “These vacation homes become central gathering places and hold immense sentimental value.”

By leaving property in a will or a trust, heirs benefit from a stepped-up basis: they only pay taxes on appreciation after the inheritance date. Families can also explore strategies like qualified personal residence trusts to reduce the taxable value of gifts while retaining control.

2. Consider LLCs and Trusts to Protect Assets

Rather than placing property directly in children’s names, high-net-worth families often hold it within a limited liability company (LLC), with the LLC itself controlled by a trust. This structure shields the property from potential lawsuits, creditor claims, or bankruptcy issues among heirs.

“If a vacation home is rented and someone is injured, the children aren’t personally liable,” says Doyle. “Other assets, like stocks or bonds, are protected too.”

Fractional ownership of LLC shares can also reduce transfer taxes because partial interests in real estate are less liquid and can be discounted for tax purposes.

3. Establish Clear Rules for Use

Operating agreements and trusts can specify how a property is used, helping prevent disputes over weekends, renovations, or rentals. Parents can also restrict transfers to children’s spouses, ensuring the property remains in the bloodline.

“Without clear guidelines, siblings may clash over scheduling or property improvements,” says Laura Mandel, chief fiduciary officer at Northern Trust. “We often include buyout provisions so one sibling can purchase another’s interest if needed.”

Families have successfully used these agreements for everything from ski chalets in Vermont to ranches in Montana, avoiding ongoing tension by clearly defining expectations upfront.

4. Fund Ongoing Maintenance and Insurance

Money is often the biggest source of disagreement. Even heirs who want to keep a property can struggle with expenses like insurance, utilities, and upkeep.

“Without funding, resentment grows fast,” says Dan Griffith, director of wealth strategy at Huntington Private Bank. “One child ends up paying bills for everyone else or demanding reimbursement, and disputes are almost guaranteed.”

Parents can allocate liquid assets or life insurance to a trust, covering ongoing costs. The operating agreement should also outline contingency plans for shortfalls, ensuring everyone’s contributions are fair.

5. Plan for Children Who Want to Sell

Even if all heirs initially agree to keep a property, life circumstances can change. A job relocation, new marriage, or unforeseen family event can lead to one or more siblings wanting to cash out.

“It’s essential to include buyout provisions,” says Doyle. “A sibling should be able to buy others’ shares, possibly using promissory notes or trust funds, without forcing a sale.”

Griffith adds, “Sometimes the grandchildren or younger family members have no attachment to a property. In those cases, selling it might actually allow those who care most to enjoy it fully.”

Passing down real estate doesn’t have to lead to conflict. Thoughtful planning, the right legal structures, and clear communication can help families preserve cherished memories while minimizing taxes, costs, and disputes. Whether it’s a city penthouse, a vineyard estate, or a mountain lodge, the key is creating a strategy that balances sentimental value with financial practicality. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses