Cooling Home Prices Stall Economic Growth, Cotality Report Reveals

The latest 2025 Q2 Homeowner Equity Report (HER) from Cotality reveals that U.S. homeowner equity, while still substantial, is showing signs of stagnation due to cooling home prices. According to the report, the average homeowner equity stands at approximately $307,000, marking the third-highest level in recorded history. This figure represents a significant increase of $124,000 compared to the first quarter of 2020, just as the pandemic began to reshape the housing market.

However, despite these solid equity gains over the past few years, the report also highlights a year-over-year (YoY) drop of $141.5 billion in borrower equity, a decrease of 0.8%. Homeowners with mortgages now hold a total of $17.5 trillion in net equity, but the softening market and modest price declines are beginning to stall further growth.

Key Takeaways from the Report:

Modest Losses in Homeowner Equity

Although recent declines in equity are relatively small, the trend is indicative of the broader challenges facing homeowners, especially as the housing market cools. In 2023, the average borrower gained $25,000 in equity, but in 2024, that gain was reduced to just $4,500. Over the past year, the average homeowner lost about $9,200 in equity, which could signal more financial strain ahead for many homeowners, particularly those considering selling or refinancing.

Rising Negative Equity

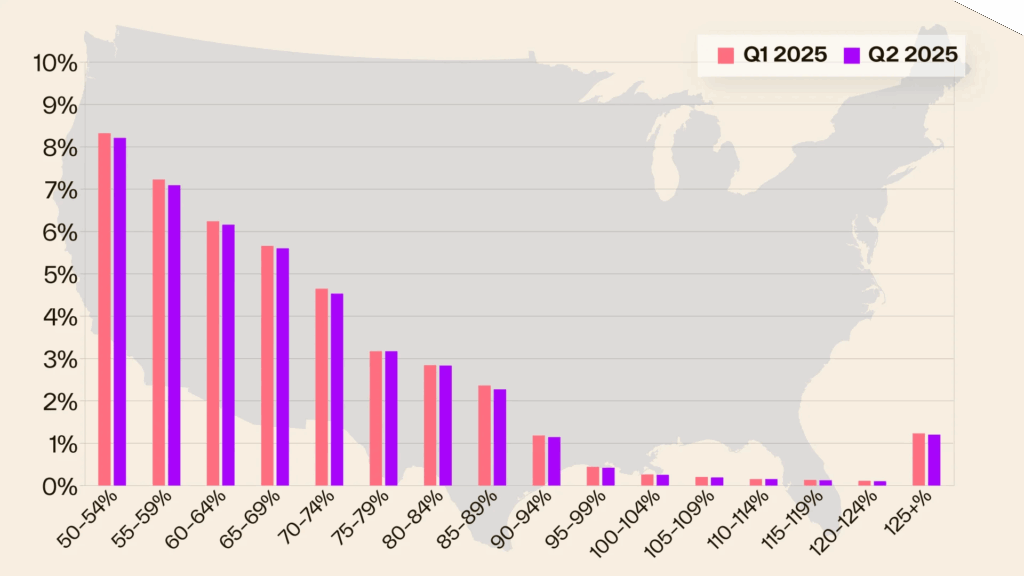

One of the more concerning trends in the report is the increase in negative equity, where homeowners owe more on their mortgages than their homes are worth. The percentage of mortgaged homes with negative equity rose from 1.7% to 2% year-over-year. This equates to 175,000 more properties entering negative equity compared to the previous year, an 18% increase. However, when measured quarterly, the number of properties with negative equity actually fell by 3.3%, largely due to the typical seasonal improvement seen during the spring homebuying season.

Geographic and Market Variations

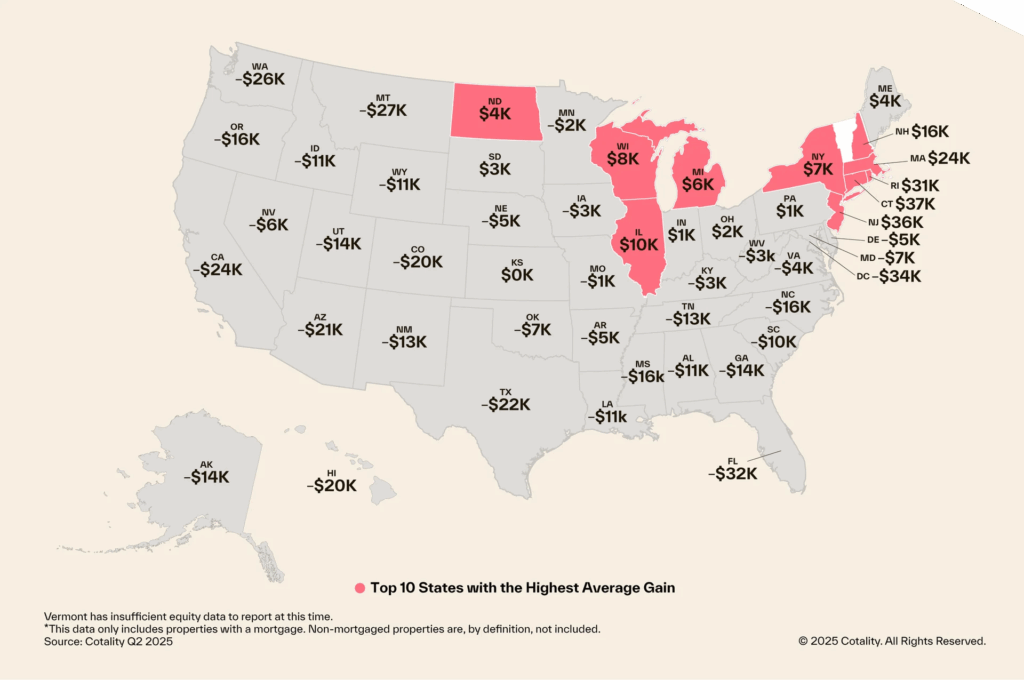

While national trends show signs of slowing, specific markets are experiencing more dramatic shifts in homeowner equity. In some regions, especially in the Northeast, homeowners have seen steady equity growth. States like Connecticut, New Jersey, and Rhode Island saw the largest equity gains YoY, with average increases of $37,400, $36,200, and $31,200, respectively. However, in other areas like the District of Columbia, Florida, and Montana, homeowners have seen significant equity losses, with declines of $34,400, $32,100, and $26,900.

The Impact of Cooling Home Prices

Dr. Selma Hepp, Cotality’s Chief Economist, noted that home price appreciation has been the slowest since the 2008 financial crisis. As appreciation moderates, homeowner equity growth is expected to slow as well, with seasonal fluctuations in home prices playing a more pronounced role in the changes to equity values. For homeowners, this means that while equity remains relatively strong in many areas, accessing that equity for purposes like refinancing or home improvement may become more challenging as home values stagnate or decline.

The Strain of Negative Equity

Several metropolitan areas have been more affected by negative equity than others. Areas like McAllen, Texas, Shreveport, Louisiana, and Cape Coral, Florida have experienced significant increases in the percentage of properties with negative equity. This is partly due to factors such as declining home prices and the impact of natural disasters, which have destroyed substantial amounts of equity in affected areas. Los Angeles, San Francisco, and Las Vegas have been less impacted, with fewer homes entering negative equity despite the national increase.

What This Means for Homeowners

Homeowners should be aware of the potential for further equity losses in the coming months as the cooling housing market and modest price declines continue to affect their property values. While equity gains have slowed, they still remain at historically high levels, and many homeowners continue to benefit from the rising equity they accumulated during the pandemic years. However, the trend of rising negative equity in certain markets, combined with stagnant home prices, may make it harder for some homeowners to leverage their properties for financial flexibility.

For homeowners in areas experiencing price declines or stagnant growth, this report suggests that they may face challenges in refinancing or accessing their home equity through loans. Homeowners should consider their options carefully and potentially focus on paying down any outstanding debt to maintain their financial stability in an uncertain housing market.

Looking Ahead

While the forecast for homeowner equity in the near future is more conservative, the Cotality Home Price Index predicts a modest 3% increase in home prices by June 2026. However, until then, homeowners may need to adjust their expectations and carefully consider their financial decisions in light of the cooling housing market.

The overall outlook indicates that while the housing market isn’t headed for a drastic collapse, homeowners should remain vigilant and make informed decisions about leveraging their home equity for future financial moves. The coming months could be a critical time for homeowners to reassess their positions and plan accordingly. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses