Housing Market Outlook: Lessons from the Past and Signals for the Future

Renowned economist Peter Schiff, best known for predicting the 2008 housing crisis, is once again raising cautionary flags about the U.S. housing market. While today’s environment differs significantly from the subprime era, Schiff warns that elevated home prices combined with rising mortgage rates could lead to challenges for prospective and current homeowners alike.

“Why are home prices still so high? For years, the Federal Reserve kept interest rates near zero, which allowed borrowers to lock in exceptionally low mortgages sometimes as low as 3% or 4%,” Schiff explained in a recent broadcast. “That artificially inflated home values because buyers could afford higher prices given their lower monthly payments.”

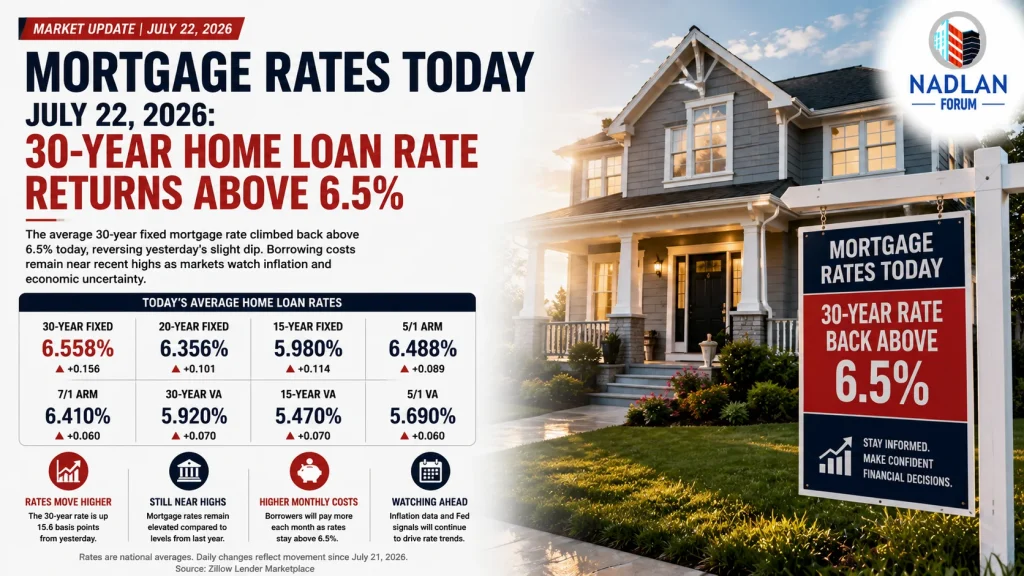

Indeed, mortgage rates have more than doubled since the era of near-zero rates. In recent years, the 30-year fixed mortgage averaged below 3%, whereas today it hovers above 6%. While higher borrowing costs typically act as a cooling mechanism for home prices, the market has not yet fully adjusted. The S&P CoreLogic Case-Shiller U.S. National Home Price Index shows that prices have risen more than 50% over the last five years, reflecting both strong demand and constrained housing supply.

Schiff notes that because homebuyers primarily focus on monthly payments rather than overall home price, the spike in mortgage rates without a corresponding drop in home prices creates an affordability mismatch. “Homes are now far more expensive relative to today’s rates than they were when rates were low. This imbalance could eventually pressure prices downward, but it might be a painful adjustment.”

U.S. Economic Considerations

According to Schiff, the transition toward rate-consistent pricing could create localized housing stress. “Some homeowners may need to sell under pressure, potentially receiving offers below what they owe on their mortgage,” he said. While widespread negative equity is less common than during the 2008 crisis, the combination of high prices and rising borrowing costs could still trigger financial strain for certain segments of the market.

Supply constraints are another factor cushioning the market. Zillow reports a national housing deficit of approximately 4.7 million homes, contributing to continued price elevation. Additionally, homeowners who locked in low mortgage rates are less inclined to sell, reducing market inventory and further limiting affordability for prospective buyers.

Schiff warns of a potential cascading effect if these pressures intensify. “Eventually, even a small group of distressed sellers could have an outsized impact on local pricing, particularly in areas where supply is already limited and prices are stretched.”

Gold as a Safe Haven

Amid concerns about housing affordability and market volatility, gold has once again emerged as a favored refuge for investors. Unlike fiat currencies, gold is not subject to inflationary pressures from monetary policy decisions, and it cannot be printed at will. Over the past 12 months, gold prices have surged more than 40%, and Schiff anticipates continued gains.

“I believe there’s a strong possibility of gold reaching $4,000 per ounce by the end of this year,” Schiff commented. Major banks, including JPMorgan and Goldman Sachs, share a similar outlook, forecasting gold prices potentially hitting that level by 2026. For investors seeking long-term security, gold IRAs offer a way to diversify retirement portfolios while benefiting from potential tax advantages.

The Role of Rentals and Real Estate Income

While the prospect of home price corrections raises concerns for buyers, one enduring trend Schiff highlights is rising rental demand. “Rents increase every year,” he notes, underscoring that rental income remains a reliable hedge against inflation. Real estate continues to offer a source of steady cash flow, which can be particularly appealing as costs for labor, materials, and land rise in tandem with overall inflation.

Legendary investor Warren Buffett has emphasized the value of income-generating real estate, stating in 2022 that he would pay $25 billion for just 1% of the nation’s apartment complexes—a testament to the long-term viability of rental properties as an investment vehicle.

For everyday investors, real estate exposure does not require massive capital or hands-on management. Platforms like Arrived, backed by notable investors including Jeff Bezos, enable individuals to purchase fractional shares in rental properties starting at just $100. This allows investors to participate in rental income without the burdens of property management, maintenance, or tenant concerns.

Schiff explains the process: “You select properties vetted for projected income and long-term value, determine how many shares to purchase, and begin receiving rental income distributions. It’s a straightforward way to benefit from real estate without the traditional headaches.”

Final Takeaways

The current U.S. housing landscape is shaped by multiple forces: historically low interest rates that fueled price growth, rising borrowing costs, limited supply, and sustained rental demand. Schiff’s perspective serves as both a caution and an opportunity. While potential price adjustments may challenge some homeowners, investors can still leverage real estate as a source of income, particularly through rentals or fractional ownership.

As the housing market evolves, prospective buyers, current homeowners, and investors alike must navigate these dynamics carefully, balancing affordability, long-term value, and alternative investment strategies. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses