How to Score a Better Mortgage Rate as 30-Year Fixed Hits a One-Year Low

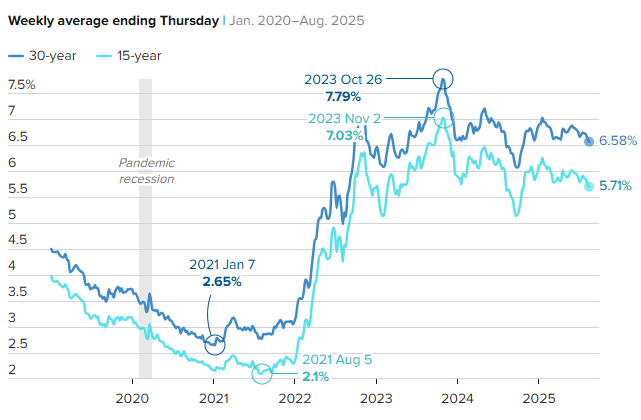

Mortgage rates are finally starting to ease, offering a rare reprieve for homebuyers who have been sidelined by persistently high borrowing costs. On Friday, the average rate for a 30-year fixed mortgage recorded its largest single-day drop in over a year. While still higher than the historically low rates seen during the pandemic, this decline brings some relief and opportunities for those planning to buy a home.

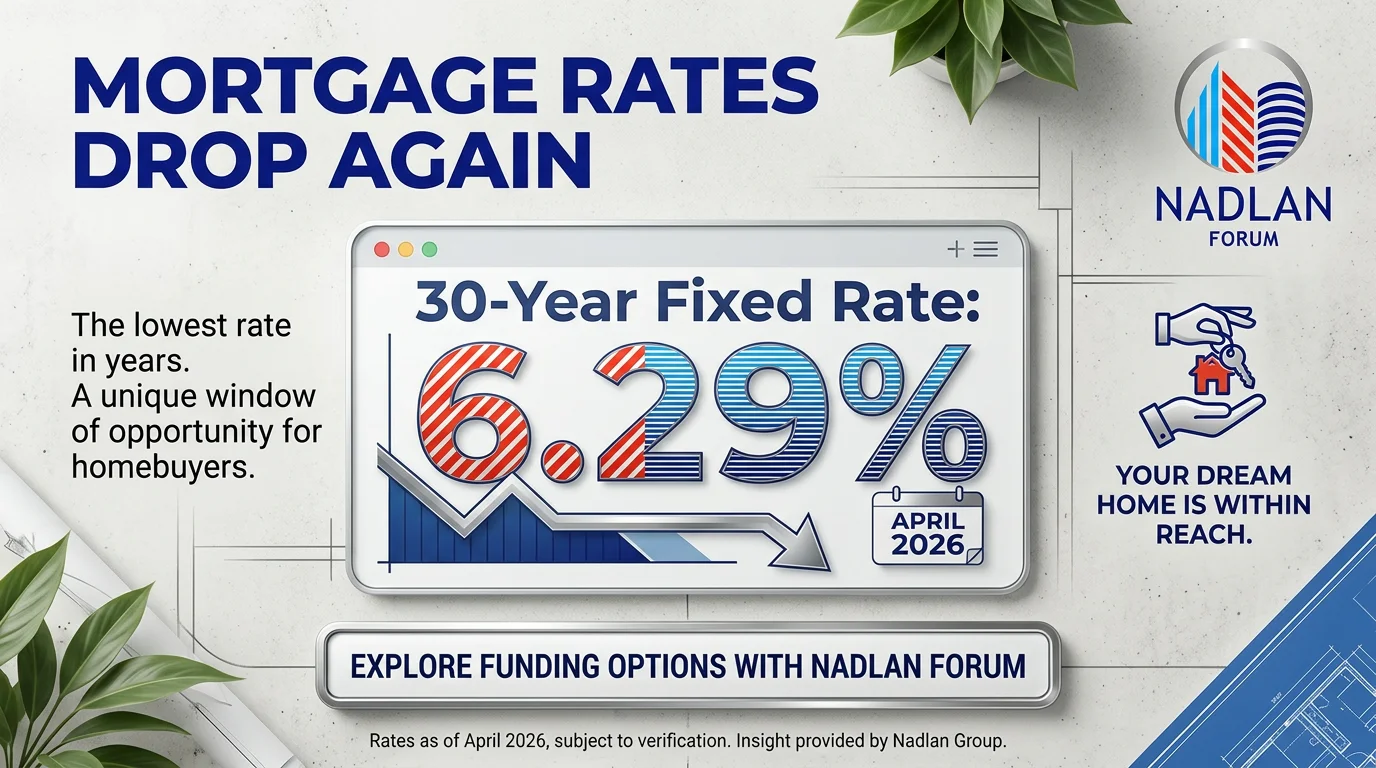

According to Mortgage News Daily, the average 30-year fixed mortgage rate now sits around 6.29%. Although this is still a significant leap from the sub-3% rates many enjoyed during 2020 and 2021, it marks the lowest level for this mortgage type since October last year. For buyers who have been waiting on the sidelines, this shift provides an incentive to act but there are strategies to secure even better terms.

Where Mortgage Rates Stand

The Federal Reserve’s upcoming policy meeting on September 17 has market watchers hopeful for an interest rate cut, which could put further downward pressure on mortgage rates. Historically, changes in the Fed’s target rate can influence mortgage lending, even for fixed-rate loans.

Lawrence Yun, chief economist at the National Association of Realtors, cautions that while some relief may come, rates near 6% should be viewed as the “new normal” for the near term. “Expecting a return to 4% or 5% rates is unrealistic at this stage,” Yun notes.

Three Key Moves to Secure a Lower Mortgage Rate

Even as overall rates fluctuate, prospective buyers have tools at their disposal to improve the mortgage terms they can secure. Here’s how to optimize your position:

1. Improve Your Credit Score

Your credit score remains the most important factor in determining your mortgage rate. The higher your score, the better the rate you’re likely to receive. Scott Lindner, national sales director for real estate and secured lending at TD Bank, emphasizes that even modest improvements in credit can translate into significant savings over the life of a loan.

FICO scores, the most widely used credit rating model, range from 300 to 850. Scores above 670 are considered “good,” over 740 are “very good,” and anything above 800 is deemed “exceptional.” For instance, someone with a score between 780 and 850 could qualify for a 30-year fixed mortgage rate of 6.19%, while someone scoring between 700 and 739 might pay 6.39%. On a $350,000 loan, that difference could add more than $13,000 in interest over the life of the mortgage.

To boost your credit score:

- Pay bills on time, even if only the minimum.

- Keep credit utilization below 30%, meaning you should not max out credit cards.

- Request higher credit limits, but avoid using the new credit to accumulate debt.

- Check for errors on your credit report. Even one inaccurate late payment can lower your score by 50 points or more.

- Maintain long-term credit accounts, as the length of your credit history signals stability to lenders.

2. Increase Your Down Payment

Putting more money down upfront can also help secure a lower rate. Lenders favor borrowers who have more equity at the outset because it reduces their risk.

Yun points out that a 20% down payment typically results in a lower mortgage rate. However, this is not feasible for everyone. In 2024, the average down payment among all homebuyers was 18%, and just 9% for first-time buyers.

If achievable, a larger down payment can yield substantial savings. Not only does it lower your interest payments over the life of the loan, but it can also help you avoid paying private mortgage insurance (PMI), which can cost thousands annually. Schulz notes, “The financial impact of putting 20% down is massive both upfront and long term.”

3. Consider Alternatives to the 30-Year Fixed

While 30-year fixed mortgages are popular, they are not the only option. Adjustable-rate mortgages (ARMs) can offer lower initial rates than fixed-rate loans. For example, a 7/6 ARM currently has a rate of 5.59%, about half a percentage point lower than a typical 30-year fixed rate.

ARMs can be particularly attractive if you plan to move or refinance within a few years. Lindner says, “A seven-year ARM allows buyers to benefit from a lower rate now, with the flexibility to refinance if rates drop further.”

Yun notes that about 90% of buyers still opt for 30-year fixed loans, but ARMs are gaining traction among younger buyers, especially those in their late 20s and 30s who anticipate moving or upgrading in the near future. The key risk, however, is that if rates rise, your ARM could eventually adjust to a higher rate than a fixed loan, increasing your monthly payments.

Additional Strategies for Savvy Buyers

Beyond these primary steps, there are smaller, often overlooked actions that can improve mortgage terms:

- Shop around and compare lenders. Even a small difference in rates can translate to thousands of dollars over the life of a loan.

- Lock in your rate at the right time. Rate locks can protect you from short-term spikes but should be timed carefully to avoid missing potential drops.

- Bundle with financial products. Some lenders offer lower rates for clients with existing accounts or investment relationships.

- Refinance when conditions improve. Even if you start with a slightly higher rate, monitoring the market for opportunities to refinance can save money over time.

Bottom Line

Mortgage rates remain higher than pandemic-era lows, but the recent dip signals an opportunity for buyers who are prepared. Improving your credit score, saving for a larger down payment, and considering alternative loan structures like ARMs can all help reduce borrowing costs.

While a 6% mortgage may feel steep compared to the under-3% rates of the past, with careful financial planning and strategic moves, homebuyers can still secure favorable terms. For those ready to act, the current environment combined with potential Fed rate cuts could make this an ideal moment to enter the market.

The key takeaway: the mortgage landscape has shifted, but savvy buyers who plan carefully and leverage every available advantage can still turn today’s rates into long-term savings. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses