Which U.S. Metros Will Benefit Most from Declining Mortgage Rates?

As the Federal Reserve recently reduced the target range for the federal funds rate by 0.25 percentage points, bringing it down to 4% to 4.25%, mortgage rates have started to inch closer to the 6% mark. This shift has opened up new opportunities for homebuyers and sellers, particularly in areas where homeownership is more reliant on mortgages. According to a recent report from Realtor.com, metros with younger, more mobile populations are expected to see the biggest boost in housing demand as mortgage rates continue to decline.

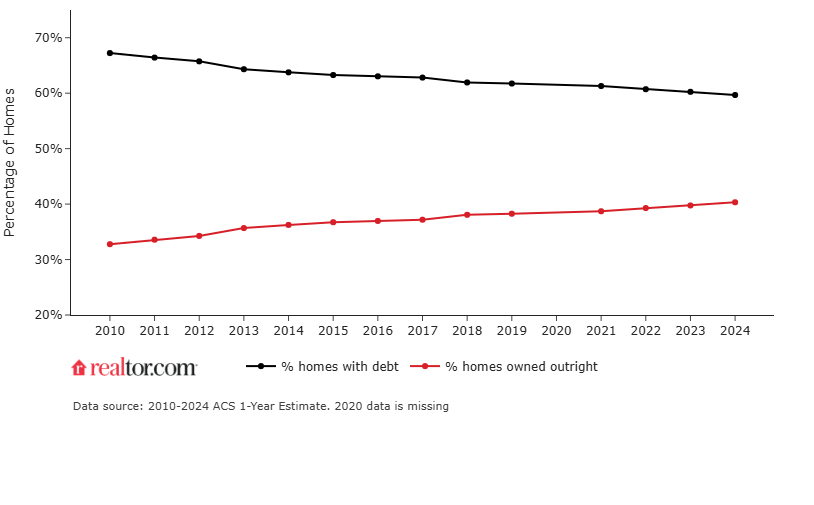

Realtor.com’s findings reveal that nearly 81% of mortgages across the country are currently under 6%, making it easier for many homeowners to sell and buyers to purchase. These metros, characterized by a younger demographic and higher mortgage reliance, are poised to see the most significant shift in market activity.

Metros Poised for a Stronger Response to Declining Rates

Washington, D.C., Denver, Colorado, Virginia Beach, Virginia, and Raleigh, North Carolina stand at the top of the list, with each having a high percentage of mortgaged households. In these areas, lower mortgage rates could prompt a surge in both buyer and seller activity, as many homeowners have mortgages that are still above the current rate threshold.

For example, Washington, D.C. has approximately 73.6% of homes mortgaged, making it highly sensitive to rate changes. In areas like Denver and Raleigh, where homeownership is similarly driven by mortgage reliance, declining rates could fuel demand as more people are encouraged to move or refinance.

“As mortgage rates dip closer to the 6% mark, we expect these metros to experience the most noticeable shift in market behavior,” said Danielle Hale, Chief Economist at Realtor.com. “For markets like Denver and Washington, D.C., where homeowners still carry mortgages, falling rates will likely unlock a wave of buyers and sellers eager to take advantage of the improved financing conditions.”

Less Responsive Markets: The Impact of Outright Homeownership

In contrast, metros such as Miami, Florida, Buffalo, New York, and Pittsburgh, Pennsylvania have a much lower percentage of mortgaged households. These markets, where a larger share of the population owns their homes outright, are likely to be slower to respond to declining mortgage rates. In these areas, the focus is less on mortgage affordability and more on other factors, such as housing supply, home equity, and age demographics.

“In metros like Miami and Buffalo, where older generations hold a larger share of the market, the response to lower rates is more muted,” Hale explained. “Homebuyers in these areas may not feel the immediate urgency to purchase, as many current homeowners are already mortgage-free and have built substantial equity over time.”

Top Metros with the Highest Share of Mortgaged Households

Realtor.com’s analysis shows the following metros with the highest share of mortgaged households, where declining mortgage rates are most likely to create a notable surge in activity:

- Washington, D.C. (73.6%)

- Denver, Colorado (72.9%)

- Virginia Beach, Virginia (70.7%)

- Raleigh, North Carolina (70.7%)

- San Diego, California (70.0%)

- Baltimore, Maryland (69.4%)

- Atlanta, Georgia (69.2%)

- Seattle, Washington (69.1%)

- Portland, Oregon (68.5%)

- Richmond, Virginia (68.3%)

These cities, with a high percentage of mortgaged homes, are well-positioned to benefit from falling mortgage rates, with more potential buyers and sellers engaging in the market.

Top Metros with the Highest Share of Outright Owners

On the flip side, markets where outright homeowners dominate, such as Miami, Buffalo, and Pittsburgh, are expected to see a slower response to lower mortgage rates. These cities tend to have an older demographic of homeowners who own their properties outright. Here’s a look at the metros with the highest share of outright owners:

- Miami, Florida (44.8%)

- Buffalo, New York (44.2%)

- Pittsburgh, Pennsylvania (44.2%)

- Detroit, Michigan (42.3%)

- Tampa, Florida (42.3%)

- Houston, Texas (42.2%)

- Tucson, Arizona (41.9%)

- San Antonio, Texas (41.5%)

- Birmingham, Alabama (41.0%)

- New York, New York (40.1%)

These metros tend to have lower mortgage reliance, particularly among older homeowners. As a result, the overall market response to lower mortgage rates will likely be less pronounced.

Nationwide Trends and Regional Implications

Looking at national trends, 64% of occupied U.S. housing units are owned, and nearly two-thirds of those homeowners have a mortgage. As the population ages, more outright owners have accumulated significant home equity, making them less reliant on new mortgages to buy homes or move. This shift in demographics highlights the growing divide between younger, more mobile homebuyers and older homeowners with paid-off properties.

“The gap between mortgage-reliant buyers and outright homeowners is widening,” Hale noted. “Regions with younger, more mobile populations will see a stronger response to falling mortgage rates, while those with older, more settled populations may experience less of an immediate boost.”

What Does This Mean for Buyers and Sellers?

For buyers and sellers in metros with a high proportion of mortgaged households, the coming months could bring significant changes. As mortgage rates fall, these areas are likely to see an uptick in transactions, with more people looking to buy homes or refinance existing mortgages. However, buyers in areas with a high percentage of outright owners may not see the same immediate market shifts.

If you’re in one of the more mortgage-dependent metros, you may find that lower rates open up more opportunities to purchase a home or secure a better financing deal. In markets with fewer mortgaged households, however, other factors like housing availability and local economic conditions may play a more significant role in the market’s response to rate changes. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses