FOMC Poised for Another Rate Cut as Data Gaps and Market Pressures Build

The Federal Open Market Committee (FOMC) appears all but certain to deliver another 25-basis-point rate cut at its meeting this Wednesday, continuing its recent pivot toward easing monetary policy amid economic uncertainty and limited government data. According to the CME FedWatch Tool, markets have priced in a more than 95% probability of a rate reduction, which would mirror the Fed’s move in September and bring the federal funds rate down to a range of 3.75%–4.0%.

“The October meeting is shaping up to be another step toward a more neutral stance,” said Sam Williamson, senior economist at First American. “The lack of key economic data from the federal government shutdown leaves policymakers operating with less visibility into the true state of the economy, particularly the labor market. That makes this meeting one of the more complicated in recent memory.”

Policy Challenges Amid a Data Blackout

With the government shutdown continuing to delay critical reports such as payrolls, retail sales, and consumer spending Fed officials are flying partially blind. As a result, they’ve been forced to rely on private-sector data, alternative spending trackers, and market-based inflation expectations. While those tools offer some insight, they lack the granularity of official government surveys.

This information gap has amplified internal debate within the FOMC. Some members are reportedly cautious about cutting too aggressively without confirmation that inflation is truly trending lower, while others favor proactive easing to protect against potential downside risks.

“Without clear data, policy disagreement becomes inevitable,” Williamson added. “Some officials would rather wait for stronger confirmation of a slowdown, while others see preemptive action as a safer move given global weakness and domestic uncertainty.”

The October meeting carries added weight because there will be no FOMC meeting in November, giving Wednesday’s decision an outsized influence on markets. Traders are already anticipating another cut at the December meeting, assuming inflation remains subdued and growth shows further signs of cooling.

Uneven Consumer Spending Clouds Outlook

Some economists remain uneasy about the Fed’s recent dovish turn. Mark Zandi, Chief Economist at Moody’s Analytics, noted last month that consumer spending is increasingly concentrated among wealthier households.

“The U.S. economy is being largely powered by the well-to-do,” Zandi wrote on X. “The top 20% of households have been spending strongly, while the bottom 80% have seen their spending barely keep up with inflation.”

This divergence raises questions about the sustainability of overall economic growth. While higher-income consumers continue to drive retail and travel activity, weaker spending among middle- and lower-income Americans could slow momentum heading into 2026.

Mortgage Market Reaction

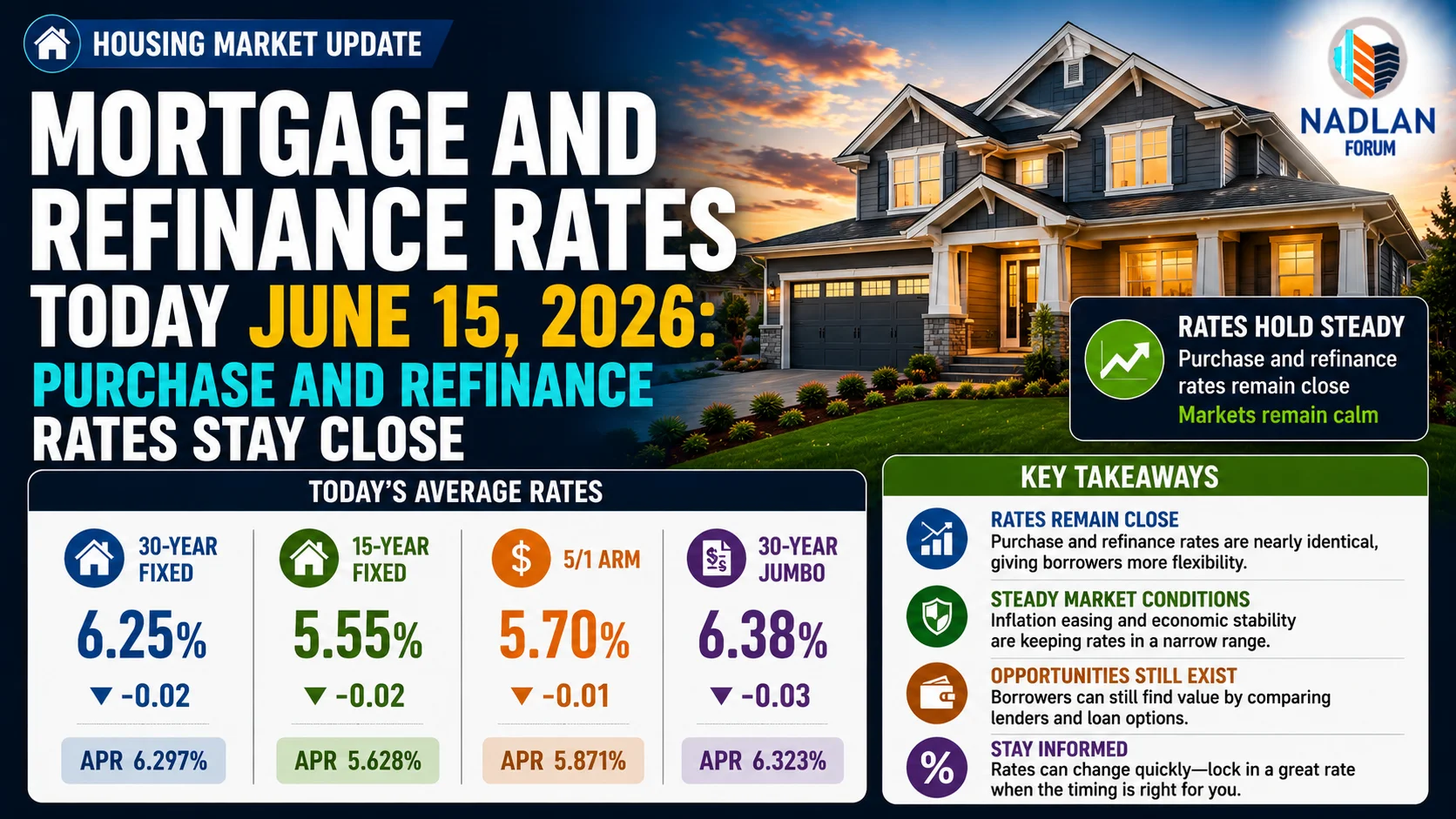

The Fed’s shift toward rate cuts has already rippled through housing finance markets. The average 30-year fixed mortgage rate dropped to 6.04% APR in the week ending October 23, down four basis points from the previous week, according to data from Zillow and Florida Realtors.

Even with rates easing, affordability remains a challenge. Home prices are still near record highs, and housing inventory remains well below pre-pandemic levels. Still, falling rates are beginning to create opportunities for both buyers and existing homeowners.

Anyone who purchased a home in mid-2024, when average mortgage rates were around 7.32%, could now refinance at about 6%, lowering their monthly payments by nearly $290 on a $300,000 loan. Over the life of the mortgage, that translates to savings of roughly $66,700, even after factoring in closing costs.

“Refinancing activity is likely to pick up if rates continue trending lower,” noted Williamson. “That could provide some relief to homeowners who bought during last year’s rate peak and are now feeling squeezed.”

Balance Sheet Policy May Amplify Market Effects

In addition to interest rate cuts, the Fed’s balance sheet strategy could soon add another layer of support to financial markets. Chair Jerome Powell recently signaled the central bank may pause its balance sheet runoff, a process known as quantitative tightening, and resume reinvesting maturing Treasury securities instead of allowing them to roll off.

Such a move would inject fresh liquidity into bond markets, helping to stabilize Treasury yields and potentially push long-term borrowing costs lower. Since mortgage rates are closely tied to the 10-year Treasury yield, even a modest decline could further improve housing affordability.

“If the Fed halts the runoff and resumes reinvestments, it would reintroduce steady demand for Treasuries,” said Williamson. “That could nudge longer-term yields lower and reinforce the effects of policy rate cuts—providing a double dose of easing.”

A Balancing Act for the Fed

The central bank now faces a difficult balancing act: supporting the economy amid softening growth and data uncertainty while avoiding the perception of overreacting. Inflation has cooled significantly since 2022, but policymakers remain wary of cutting rates too quickly and reigniting price pressures.

Still, with global growth slowing, labor market signals turning mixed, and inflation measures holding near 3%, markets expect the Fed to err on the side of caution by continuing to loosen policy modestly.

“This is a risk management cycle, not a stimulus cycle,” Williamson concluded. “The Fed is trying to guide the economy to a soft landing without the usual data playbook. Every decision now carries more weight—and more risk—than in a typical environment.” For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses