How Much Could Falling Mortgage Rates Save Homebuyers Over the Life of a Loan?

Amid high home prices and limited inventory, homebuyers have faced an uphill battle over the past few years. But there’s finally some relief on the horizon: mortgage rates are falling, and that’s translating into meaningful savings for borrowers across the country.

A new LendingTree analysis reveals that the average APR on 30-year fixed-rate mortgages dropped by 0.51 percentage points between July 2024 and July 2025 from 7.19% to 6.68%. While that half-point drop may sound modest, the long-term impact is substantial: the average borrower could save around $40,000 over the life of a 30-year loan.

“Even small decreases in mortgage rates can make a big difference,” said Matt Schulz, LendingTree’s Chief Consumer Finance Analyst. “When you’re dealing with large loan amounts, every fraction of a percentage point adds up to thousands in potential savings.”

Key Findings from the LendingTree Report

- Average APR decline: Down 0.51 percentage points nationwide (7.19% → 6.68%).

- Monthly savings: Borrowers are paying $111.71 less per month on average, or about $1,340.56 less per year.

- Lifetime savings: Over 30 years, that adds up to $40,216.81 in total savings.

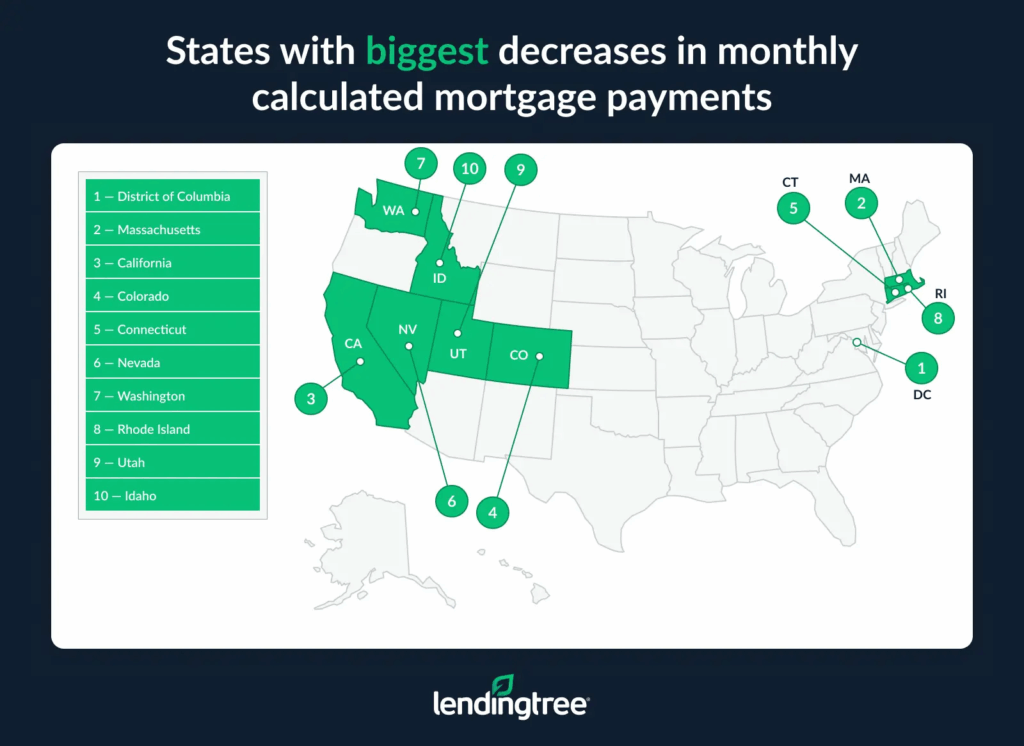

- Biggest savings: Borrowers in Washington, D.C., Massachusetts, and California saw the greatest monthly drops, cutting payments by roughly $210–$214 per month, or more than $75,000 in lifetime savings.

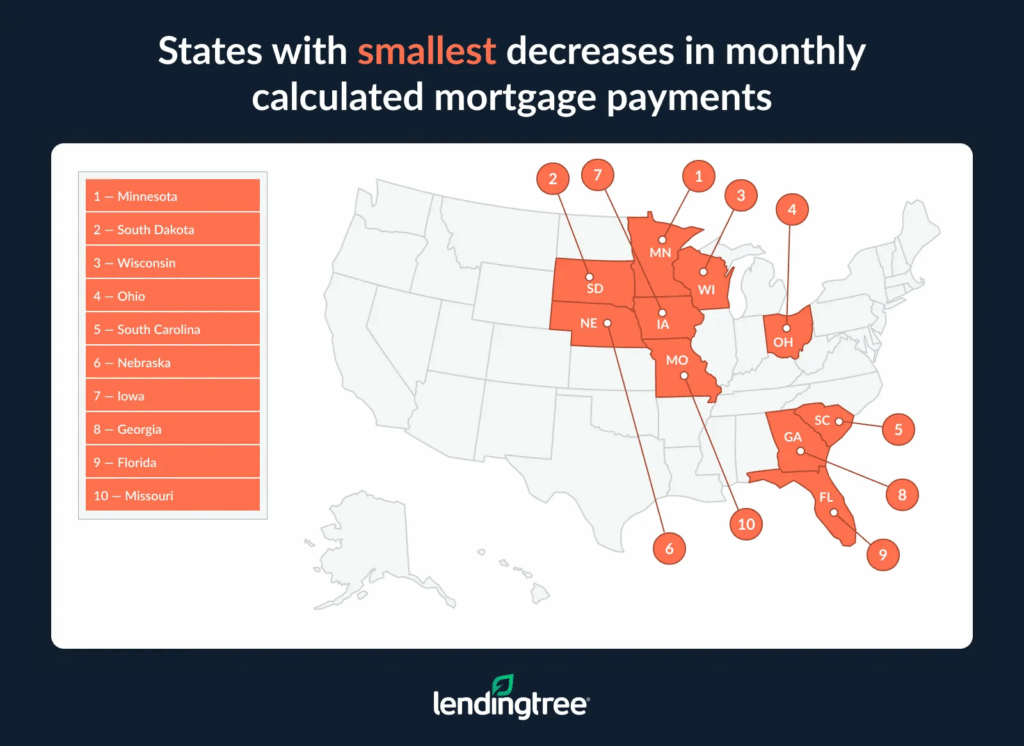

- Smallest savings: Homeowners in Minnesota, South Dakota, and Wisconsin saw more modest declines of just $24–$31 per month, equating to about $9,700–$11,000 in 30-year savings.

- North Dakota exception: It was the only state where rates rose, ticking up from 6.81% to 6.84%, adding about $1,858 in costs over the life of a loan.

What’s Driving the Decline in Mortgage Rates?

The downward movement in rates over the past year reflects a shift in monetary policy and cooling inflation pressures. The Federal Reserve’s rate cuts in late 2024 helped stabilize borrowing costs, and while the Fed doesn’t directly set mortgage rates, its decisions influence overall credit conditions and investor sentiment in bond markets.

After a volatile period in 2023 and early 2024 when inflation fears pushed mortgage rates near 8% the more dovish tone from the Fed and signs of economic moderation have restored confidence that borrowing costs will continue to ease gradually through 2026.

“Rate cuts don’t automatically lower mortgage rates overnight,” Schulz explained, “but they signal to investors that the cost of borrowing should come down over time, which tends to bring yields and by extension mortgage rates lower.”

Regional Breakdown: Where Borrowers Save the Most

Borrowers in high-cost housing markets are seeing the largest dollar savings simply because they have larger loan balances.

District of Columbia:

- Mortgage rates fell by 0.69 percentage points, leading to $213.85 less per month on average.

- That equates to $2,566 annually or $76,984 in lifetime savings.

Massachusetts:

- Rates decreased 0.72 points, lowering payments by $210.42 per month—or $75,752 saved over 30 years.

California:

- Average rates fell 0.64 points, dropping payments by $209.26 per month, saving homeowners $75,333 over the life of a loan.

“These are some of the most expensive housing markets in the country,” Schulz noted. “Because home prices and loan amounts are higher, even a half-point reduction in rates can lead to tens of thousands in savings.”

By contrast, smaller Midwestern states where homes tend to be more affordable experienced lower dollar savings but similar percentage benefits.

Minnesota, South Dakota, and Wisconsin saw APR declines of just 0.12 to 0.17 points, yet those small improvements still translated into nearly $10,000 in long-term savings for many borrowers.

Why Rate Changes Matter More Than You Think

Falling rates don’t just help homebuyers they also improve affordability across the entire housing market. Lower mortgage payments can make the difference between qualifying for a loan or being priced out altogether.

For example, a borrower with a $400,000 loan at 7.2% pays about $2,715 per month. Lowering that rate to 6.7% cuts the payment to around $2,580, saving $135 each month enough to free up thousands per year for other expenses or savings goals.

“Every time rates drop, housing affordability improves,” said Schulz. “It can help first-time buyers get into the market and make it easier for existing homeowners to refinance and improve their financial position.”

How Borrowers Can Maximize Their Savings

While no one can control national interest rate movements, borrowers can take several proactive steps to secure the lowest possible APR:

- Shop Around: Compare offers from multiple lenders. Even a small difference in rates can lead to massive long-term savings.

- Improve Credit Health: A higher credit score can unlock better rates. Pay down debt, make on-time payments, and avoid new credit inquiries before applying.

- Increase Your Down Payment: Putting more money down reduces the lender’s risk and can help you qualify for a lower rate.

- Consider Different Loan Terms: Shorter-term loans (like 15-year mortgages) and adjustable-rate mortgages (ARMs) often have lower initial rates. Evaluate what fits your financial goals.

- Ask About Discounts: Some lenders offer reduced rates for autopay enrollment, existing relationships, or paying points upfront.

“Borrowers often underestimate their own influence,” Schulz emphasized. “You can’t control the Fed, but you can control how you prepare and how many quotes you get. A few smart moves can easily save you tens of thousands over time.”

The Bottom Line

While home prices remain stubbornly high, declining mortgage rates are finally providing some relief to both buyers and current homeowners. Whether through refinancing or new purchases, today’s lower rates are giving borrowers a rare opportunity to cut costs and rebuild affordability in a market that’s been stretched thin. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses