U.S. Housing Supply Expected to Grow in 2026 as Market Slowly Recovers

First American’s 2025 forecast predicted a year of slow but steady progress and the housing market largely followed that path. Mortgage rates eased, inventory improved, and affordability inched up throughout the year. Buyers also filed more purchase applications than in 2024. Still, experts warn that the market remains far from “normal,” as high prices and the ongoing rate lock-in effect continue to limit the number of homes for sale.

The report explains that housing recoveries take time, and 2025 was just the beginning. Much of what shaped this year limited supply in some regions, improving affordability, and steady buyer demand will likely carry into 2026.

According to the forecast, six key forces will guide the 2026 housing market:

growing supply, stress points, regional gaps, affordability, life-driven demand, and new-home strength.

First American summed it up clearly: “The housing market will not be fully normal in 2026, but it should take another step forward as life events pull more buyers and sellers into the market.”

Affordability Expected to Improve Slowly With Help From Prices and Income

The direction of mortgage rates next year depends heavily on inflation, job trends, and Federal Reserve policy. The Fed began cutting rates in 2025, but analysts note that future cuts may be limited by government spending, tariff-related price pressure, and stubborn inflation.

Most projections place mortgage rates in the low-6% range for 2026. A dip below that level is possible, but experts say rates alone will not restart the market.

A bigger boost may come from growing inventory and stable home price growth. Home prices appreciated at the slowest pace since 2012 in 2025, and incomes outpaced price gains in many areas. If this pattern continues, affordability should improve again in 2026 especially where sellers are cutting prices to attract buyers.

Another major factor is the amount of pent-up demand. Between 2022 and 2025, the market saw roughly 4 million fewer sales each year than the pre-pandemic average. That means millions of households delayed buying or selling.

Demographics add to the pressure. Nearly 52 million Americans are in their 30s, and many still rent. Millennials are expected to add more than 10 million new homeowner households over the next 25 years, with Gen Z close behind. Life events marriage, divorce, new jobs, caregiving, and retirement will continue to move buyers and sellers even if mortgage rates stay near current levels.

Regional Gaps: Some Areas Stay Tight, While Others See More Supply

Inventory has not improved evenly across the country. The Midwest and Northeast remain the most limited in both new-home and resale supply. These areas are likely to keep seeing fast sales and fewer seller concessions through 2026.

In contrast, many Southern and Western metros now have more homes for sale. In September, 22 of the top 75 markets had higher active inventory than the 2018–2019 average and all were in the South or West. Half were in Texas or Florida, where new construction and slower demand kept supply rising.

Cities like Austin, TX, and Tampa, FL, saw big price jumps during the boom, followed by slower population growth and higher borrowing costs. That made homes feel overpriced compared with local wages. Large new-home supply in these markets added even more choices for buyers.

Experts expect a “two-speed market” in 2026:

- South & West: Softer conditions, more supply, slower price growth

- Northeast & Midwest: Tight inventory and steady prices

Lower mortgage rates or stronger job growth could help soften markets stabilize later in the year. But rising insurance expenses especially in coastal states may widen the gap between markets with high and low carrying costs.

Is Housing Distress Building?

Foreclosure activity has risen from the record lows seen during the pandemic, but analysts do not expect a major spike in distress. Trouble spots mostly appear where buyers have thin financial cushions, higher insurance bills, or slower job growth.

The two biggest triggers for widespread foreclosures major job loss and negative equity are not present on a large scale. Most homeowners still have strong equity and stable employment. While some recent buyers in overheated markets may see price declines, the overall risk remains contained going into 2026.

Listing Activity Expected to Keep Rising Into 2026

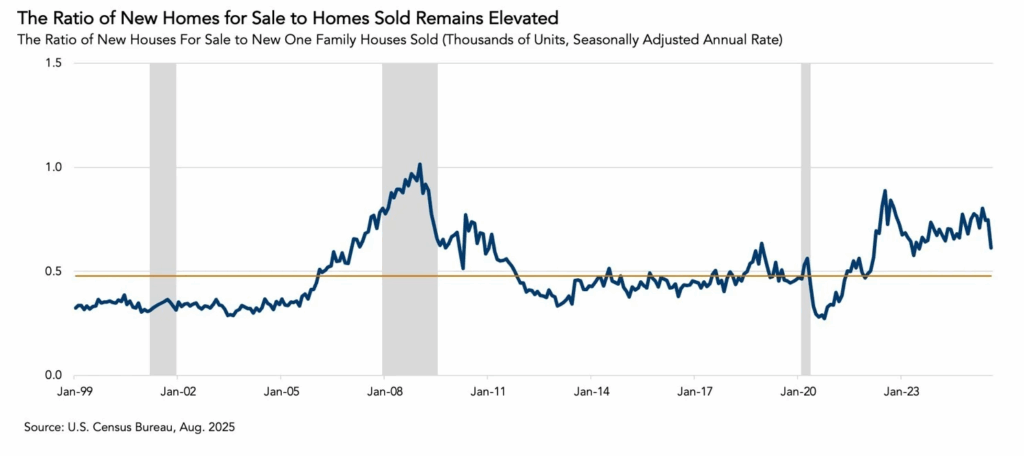

More owners in 2025 accepted that mortgage rates may stay “higher for longer,” which helped boost supply. First American tracks an “inventory turnover” measure how many existing homes are listed for sale relative to the number of households. Historically, the average sits around 2.5%.

Early in 2025, turnover was about 1.4%, and improved to nearly 1.5% by the end of the year. That’s still far below normal, but moving upward. Growth was strongest in the Sun Belt, where new construction and slower buyer demand kept listings rising.

Even though some sellers tested the market and later pulled their listings, the total number of active listings remained higher than the prior year. This gradual rise is expected to continue into 2026 as more owners move for life-driven reasons and as new homes get completed.

Builder Outlook: Cautious but Active

With inventory rising and demand softer in some regions, single-family construction has slowed slightly. New-home buyers are facing affordability challenges, and resale options have become more available again.

Builders have been relying heavily on incentives such as mortgage rate buydowns, closing cost help, and price cuts—to move homes. These incentives attract buyers but reduce builder margins, making developers more careful with new starts.

Still, new homes will likely hold an advantage in 2026. Many existing homeowners remain locked into 3%–4% mortgage rates and are reluctant to sell. Builders, on the other hand, can adjust prices quickly and offer incentives, giving buyers more flexibility.

Looking Ahead: What to Expect in 2026

The forecast for 2026 points to:

- More housing supply, but still below normal

- Gradual improvement in affordability

- Steady demand driven by life events and demographics

- Regional differences that shape buyer and seller expectations

- A continued edge for the new-home market

While the housing market won’t fully “reset” in 2026, it is expected to make progress. As inventory grows, incomes rise, and mortgage rates stabilize, more buyers and sellers should feel ready to return to the market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses