Flip Home Loans: Financing Your Real Estate Investment

Real estate investors who specialize in buying, renovating, and reselling properties need fast, flexible financing solutions that traditional mortgage lenders often cannot provide. Flip home loans have emerged as a specialized financial product designed specifically for investors who want to capitalize on distressed properties, execute strategic renovations, and generate profit through quick sales. These short-term financing instruments offer unique advantages and challenges that every investor should understand before entering the competitive world of property flipping. Whether you're a seasoned investor or exploring your first renovation project, understanding the mechanics of flip home loans can mean the difference between a profitable venture and a financial setback.

Understanding Flip Home Loans and Their Purpose

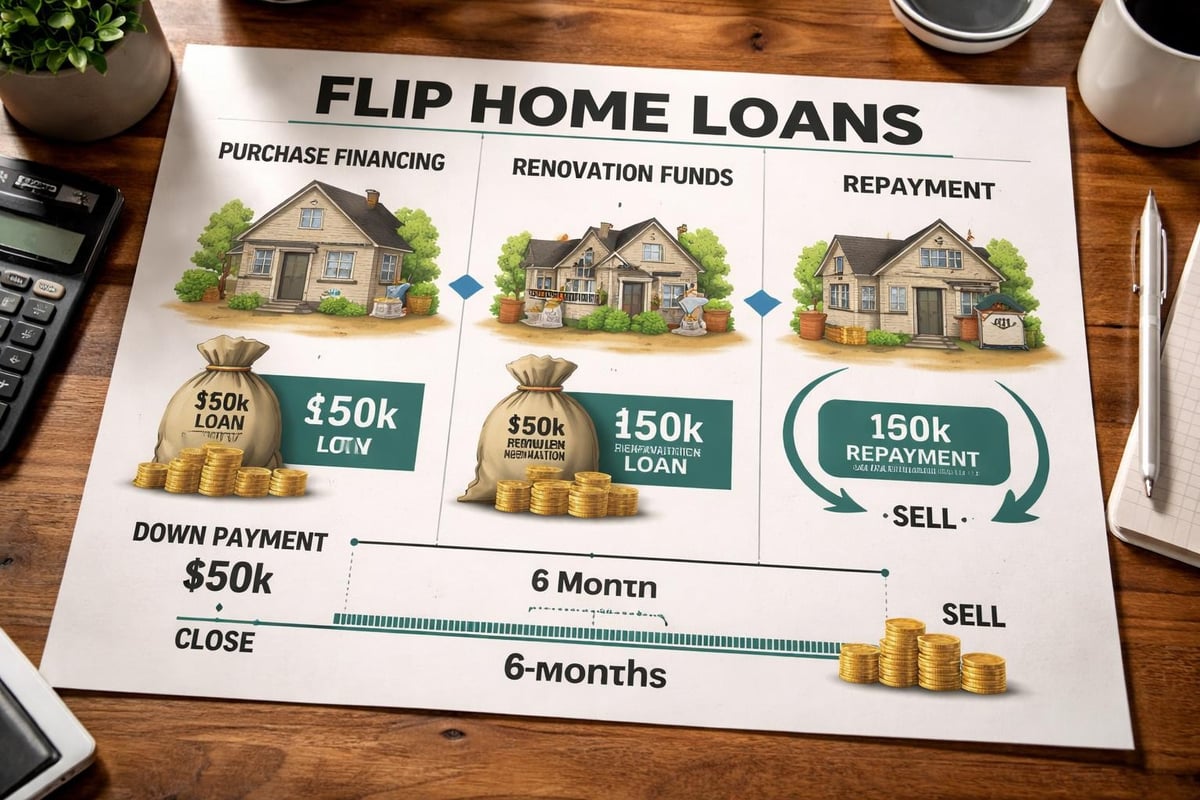

Flip home loans are short-term financing products specifically structured to help real estate investors purchase and renovate properties for resale. Unlike conventional mortgages that span 15 to 30 years, these loans typically run between six and eighteen months, aligning with the timeframe most investors need to complete a flip project.

The fundamental purpose of flip home loans is to provide rapid access to capital. Traditional lenders often require extensive documentation, long approval processes, and strict property condition requirements that make them impractical for distressed properties. In contrast, flip home loans focus primarily on the property's potential value after repairs rather than its current condition.

Key Components of Flip Home Loans

These specialized financing products consist of several critical elements that differentiate them from traditional mortgages:

- Purchase price financing: Covers the initial acquisition cost of the property

- Renovation budget: Provides funds for repairs, improvements, and upgrades

- Short repayment terms: Typically 6-18 months to encourage quick project completion

- Higher interest rates: Reflects the increased risk and shorter timeline

- Asset-based approval: Focuses on property value rather than borrower credit score

Understanding the concept of property flipping as an investment strategy helps contextualize why these loans are structured differently than conventional financing.

How Flip Home Loans Differ from Traditional Mortgages

The distinctions between flip home loans and conventional mortgages are substantial and impact every aspect of the financing process. Traditional mortgages prioritize the borrower's creditworthiness, employment history, and debt-to-income ratio. Flip home loans, by contrast, evaluate the property's potential and the investor's experience level.

| Feature | Flip Home Loans | Traditional Mortgages |

|---|---|---|

| Loan Term | 6-18 months | 15-30 years |

| Approval Time | 7-14 days | 30-45 days |

| Interest Rates | 8-15% | 3-7% |

| Primary Focus | Property potential | Borrower creditworthiness |

| Property Condition | Any condition accepted | Must meet habitability standards |

| Down Payment | 10-30% | 3-20% |

The approval process for flip home loans moves considerably faster because lenders assess risk differently. They calculate two critical metrics: Loan-to-Value (LTV) and After Repair Value (ARV). The LTV represents the loan amount relative to the current purchase price, while ARV estimates the property's worth after renovations are complete.

Interest Rates and Payment Structures

Flip home loans carry significantly higher interest rates than conventional mortgages, typically ranging from 8% to 15% annually. This premium reflects the shorter term, higher risk profile, and specialized nature of the financing. Many lenders structure these loans as interest-only payments, allowing investors to minimize monthly expenses while the property undergoes renovation.

Some lenders charge points upfront, which are percentage-based fees calculated on the total loan amount. A typical flip home loan might include 2-4 points, meaning an investor borrowing $200,000 would pay $4,000 to $8,000 in origination fees. These costs must be factored into the overall project budget to ensure profitability.

Types of Flip Home Loans Available to Investors

Investors can access flip home loans through several different channels, each with distinct advantages and qualification requirements. Understanding these options helps investors select the financing that best aligns with their project needs and financial situation.

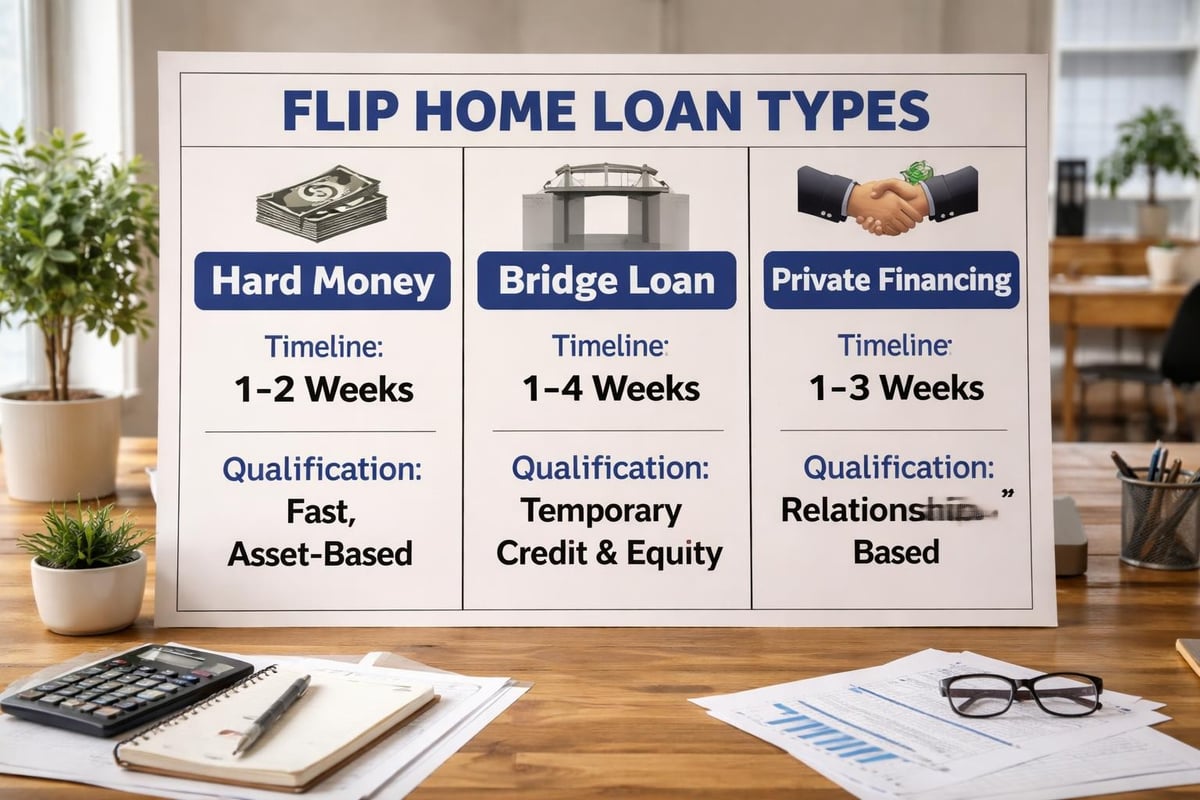

Hard Money Loans

Hard money loans represent the most common type of flip home loans. These are provided by private lenders or companies specializing in real estate investment financing. Hard money lenders for house flipping focus primarily on the property's value and potential rather than the borrower's credit history.

Advantages of hard money loans:

- Fastest approval process (often within days)

- Flexible terms negotiable with individual lenders

- Accept properties in any condition

- Less stringent credit requirements

- Can fund both purchase and renovation costs

Disadvantages to consider:

- Highest interest rates among flip financing options

- Significant upfront points and fees

- Shorter repayment windows create pressure

- May require substantial down payments

The fundamentals of hard money fix and flip loans include understanding how lenders evaluate both the current property value and the projected ARV to determine loan amounts and terms.

Bridge Loans

Bridge loans serve as temporary financing solutions that "bridge" the gap between purchasing a property and securing permanent financing or completing a sale. While similar to hard money loans, bridge loans typically come from more traditional financial institutions and may offer slightly better terms.

These loans work particularly well for investors who need to act quickly on a property opportunity but haven't yet sold their current investment. The short-term nature of bridge loans aligns perfectly with the flip timeline, though they may require stronger borrower qualifications than hard money alternatives.

Qualification Requirements for Flip Home Loans

While flip home loans are generally more accessible than traditional mortgages, lenders still maintain specific qualification standards to protect their investment. Understanding these requirements helps investors prepare successful applications and avoid delays.

Experience and Track Record

Many lenders prefer working with investors who have completed at least one or two successful flip projects. First-time flippers may face additional scrutiny, higher down payment requirements, or the need to partner with experienced investors. Some lenders require detailed renovation plans and contractor bids to verify the project's feasibility.

Documentation typically required:

- Property purchase agreement

- Detailed scope of work for renovations

- Contractor estimates and bids

- After Repair Value appraisal or comparative market analysis

- Personal financial statements

- Proof of liquid reserves

- Previous flip project experience (if applicable)

Down Payment and Reserve Requirements

Most flip home loans require down payments ranging from 10% to 30% of the purchase price. The exact percentage depends on the lender's risk assessment, the property's condition, and the borrower's experience level. Additionally, lenders often require investors to maintain cash reserves equal to several months of loan payments.

The structure and benefits of fix and flip loans emphasize the importance of adequate capitalization beyond just the down payment. Unexpected renovation costs, permit delays, or market shifts can extend the project timeline, making reserve funds essential for success.

Calculating Costs and Determining Profitability

Successful real estate investors master the art of accurate cost projection before committing to flip home loans. Every expense must be accounted for to ensure the project remains profitable after all costs are paid.

Comprehensive Cost Analysis

A complete flip project budget includes numerous line items beyond the obvious purchase price and renovation costs:

| Cost Category | Typical Percentage | Description |

|---|---|---|

| Purchase Price | 60-70% | Initial property acquisition cost |

| Renovation Costs | 15-25% | Materials, labor, permits |

| Financing Costs | 5-8% | Interest, points, fees |

| Holding Costs | 3-5% | Utilities, insurance, property taxes |

| Selling Costs | 6-8% | Agent commissions, closing costs |

| Contingency Reserve | 5-10% | Unexpected expenses |

Interest expenses accumulate throughout the project duration. A $200,000 flip home loan at 12% annual interest held for nine months would cost approximately $18,000 in interest charges. Many investors underestimate this expense, eroding their profit margins.

The 70% Rule for Flip Investments

Experienced investors often apply the 70% rule when evaluating potential flip opportunities. This guideline suggests that the total investment (purchase price plus renovation costs) should not exceed 70% of the after repair value. This margin provides buffer for financing costs, holding expenses, selling fees, and profit.

For example, if a property's ARV is estimated at $300,000:

- Maximum total investment: $210,000 (70% of ARV)

- Less renovation costs: $50,000

- Maximum purchase price: $160,000

The features of fix and flip loans including loan-to-cost ratios help investors understand how much financing they can secure based on their project numbers.

Strategic Advantages of Using Flip Home Loans

Despite higher costs compared to traditional financing, flip home loans offer strategic advantages that make them invaluable tools for serious real estate investors. The ability to move quickly on opportunities often outweighs the premium paid for specialized financing.

Speed and Competitive Advantage

In competitive real estate markets, the ability to make cash-equivalent offers gives investors significant leverage. Sellers of distressed properties often prioritize speed and certainty over maximum price. An investor with pre-approved flip home loans can close in 7-10 days, competing effectively against all-cash buyers.

This speed advantage allows investors to:

- Negotiate better purchase prices

- Secure properties before competitors

- Capitalize on time-sensitive opportunities

- Build relationships with wholesalers and agents

Leverage and Portfolio Expansion

Flip home loans enable investors to leverage their capital across multiple projects simultaneously rather than tying all funds into a single property. An investor with $100,000 in available capital might purchase one property outright or use flip home loans to finance three or four projects concurrently.

This leverage multiplies both potential returns and risk. Successful execution of multiple flip projects can generate substantially higher annual returns than sequential single-project approaches, though it requires sophisticated project management and risk assessment skills.

Portfolio expansion through flip home loans showing how one investor's capital can fund multiple simultaneous projects versus single property investment

Common Pitfalls and Risk Management

While flip home loans provide powerful financing tools, they also introduce risks that can devastate unprepared investors. Understanding common mistakes helps investors develop strategies to protect their investments and maintain profitability.

Timeline Pressure and Extension Challenges

The short-term nature of flip home loans creates intense pressure to complete projects quickly. Renovation delays caused by contractor issues, permit problems, weather, or unforeseen structural problems can push projects beyond the original loan term. Loan extensions typically come with additional fees and may require renegotiation.

Risk mitigation strategies:

- Build realistic timelines with buffer periods

- Maintain strong contractor relationships and backup options

- Start permit processes before closing

- Conduct thorough property inspections

- Secure firm contractor bids before committing

Market Volatility and Exit Strategy

Real estate markets can shift during renovation periods, potentially affecting the property's ARV and sale timeline. Investors relying on flip home loans must maintain awareness of market conditions and have contingency exit strategies if the market softens.

Alternative exit options include:

- Renting the property temporarily while waiting for better market conditions

- Refinancing into conventional investment property financing

- Seller financing to qualified buyers

- Price adjustments to facilitate faster sales

It's crucial to be aware of predatory mortgage lending practices that can trap investors in unfavorable loan terms or misleading agreements.

Working with Flip Home Loan Lenders

Selecting the right lender significantly impacts the success of flip projects. Not all lenders offer the same terms, service levels, or expertise in real estate investment financing. Building relationships with reliable lenders creates long-term advantages for active investors.

Evaluating Lender Options

Investors should compare multiple lenders across several critical dimensions before committing to flip home loans:

- Interest rates and fees: Compare all-in costs, not just advertised rates

- Loan-to-value ratios: Higher LTV means less cash required upfront

- Renovation funding structure: Draw schedules and inspection requirements

- Approval and closing speed: Time-to-funding impacts deal competitiveness

- Extension policies: Understand costs and processes for timeline extensions

- Reputation and reviews: Research lender track records with other investors

The key features of fix and flip loans including loan terms and interest-only payment options vary significantly between lenders, making thorough comparison essential.

Building Lender Relationships

Successful investors cultivate ongoing relationships with multiple lenders rather than approaching financing as a transactional activity. Lenders who understand an investor's track record, business model, and reliability often provide preferential terms, faster approvals, and greater flexibility during challenging situations.

Regular communication, transparency about project progress, and consistent loan repayment build credibility that translates into better financing opportunities. Some investors work exclusively with one or two preferred lenders who become familiar with their investment criteria and execution capabilities.

Maximizing Returns with Strategic Flip Home Loan Use

Advanced investors employ sophisticated strategies to optimize their use of flip home loans and maximize returns on investment capital. These techniques require experience and careful risk management but can significantly enhance profitability.

Project Stacking and Capital Efficiency

Experienced investors often maintain multiple projects at different stages of completion, creating a pipeline that generates continuous cash flow. This approach requires careful capital management and strong relationships with flip home loan lenders who can provide financing for overlapping projects.

Pipeline management components:

- Acquisition phase: Identifying and securing new properties

- Renovation phase: Active construction and improvement work

- Marketing phase: Preparing for sale and showing properties

- Closing phase: Finalizing sales and repaying flip home loans

This staggered approach allows investors to reinvest proceeds from completed projects into new acquisitions while maintaining active renovations, creating momentum and efficiency in their investment business.

Negotiating Better Terms Through Performance

Investors who consistently complete successful projects and repay flip home loans on time earn favorable treatment from lenders. This performance history can translate into reduced interest rates, lower points, higher loan-to-value ratios, and faster approval processes.

Some lenders offer tiered pricing structures where investors receive progressively better terms as they complete more projects. The savings on interest and fees across multiple projects can amount to tens of thousands of dollars annually for active investors.

Alternative Financing Strategies to Consider

While flip home loans serve as the primary financing tool for most property flippers, savvy investors explore complementary strategies that can reduce costs or provide additional flexibility. Understanding the full spectrum of financing options enables more strategic capital deployment.

Private Money and Partnership Structures

Private money from individual investors offers an alternative to institutional flip home loans. These arrangements typically involve higher returns for the capital provider but may offer more flexible terms and structures than traditional lenders. Some investors establish ongoing relationships with private money sources who fund multiple projects.

Partnership structures allow investors to combine their expertise with partners who provide capital. These arrangements might split profits 50/50 or use other formulas based on each party's contribution. Partnerships reduce individual capital requirements while distributing risk across multiple parties.

Lines of Credit and Hybrid Approaches

Some experienced investors secure business lines of credit backed by their real estate portfolio or other assets. These revolving credit facilities can supplement flip home loans by covering down payments, closing costs, or unexpected expenses without requiring separate loan applications for each use.

Hybrid approaches might combine a smaller flip home loan with personal capital or lines of credit to optimize the cost of capital while maintaining adequate financing for the complete project.

Flip home loans provide essential financing tools that enable real estate investors to capitalize on renovation opportunities that traditional mortgages cannot support. Understanding the structure, costs, and strategic applications of these specialized loans separates successful investors from those who struggle with undercapitalized projects.

Whether you're planning your first flip or scaling an established investment business, connecting with experienced investors and industry professionals accelerates your learning and helps you avoid costly mistakes. Nadlan Forum offers resources, community engagement, and expert insights specifically designed for real estate investors navigating the complexities of property investment financing. Join the conversation to learn from successful investors, share your experiences, and access the knowledge you need to build a profitable real estate investment business.

Responses